Antin Infrastructure Partners

2026 Update - Reaching the inflection point

Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

Introduction

Antin trades at 11x EV/FCFF, yet is a high quality company providing stable and predictable cash flows.

It’s an illiquid company, which explains part of the discount in valuation, with a free float of 16% (currently less than €400m potentially available in the market)

Company will start a new fundraising cycle this year which should contribute to an uplift in AUM and earnings

Current stock price provides margin of safety (company should be trading at least 20% higher), and in the meantime, it delivers a solid and sustainable 7% dividend yield.

Investing in Antin today is like investing in an investment grade bond yielding 7% per year, which is in line with past market performance, but without the risk that passive investors face with indexes valuations at all time highs.

Antin passes our Asymmetric test and represents ~5% of the portfolio.

I. Antin in a Nutshell

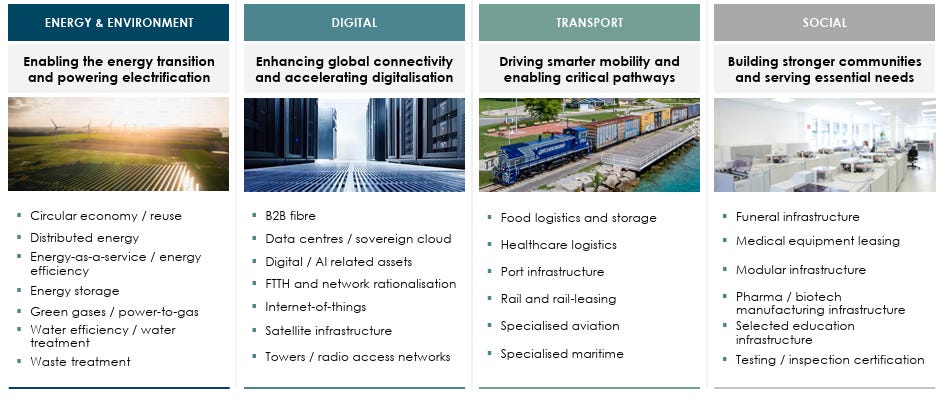

Antin Infrastructure Partners is a private equity company focused on infrastructure companies across Europe and North America.

The company focuses on infrastructure companies withing transport, energy & environmental, digital and social sectores.

Antin manages three different strategies:

Flagship — The core strategy with the first fund launched 20 years ago. It current has ~€18.6bn of fee-earning assets under management (AUM). Last fund reached €10bn size.

Mid-cap — A new strategy launched in 2021 focusing on mid-market infrastructure investments. As the Flagship strategy becomes larger and can’t target mid-market companies, the firm launched this fund to continue investing in this segment.

NextGen — Strategy launched also in 2021 that invests in new businesses and technologies that require capital to scale.

Antin effectively covers the entire segment in the infrastructure space, from newer companies/technologies to very large investments.

Current investments are concentrated in the digital infrastructure space (fiber companies, data centers, etc.), and energy & environment (district energy, renewables, etc.).

Antin applies what they call the “Infrastructure Test”, which are the main characteristics that their investments need to comply:

Provide as essential service to the community

Exhibit significant barriers to market entry

Have stable and predictable cash flows, that are inflation-linked

Display robust downside protection, mostly insulated from the business cycle.

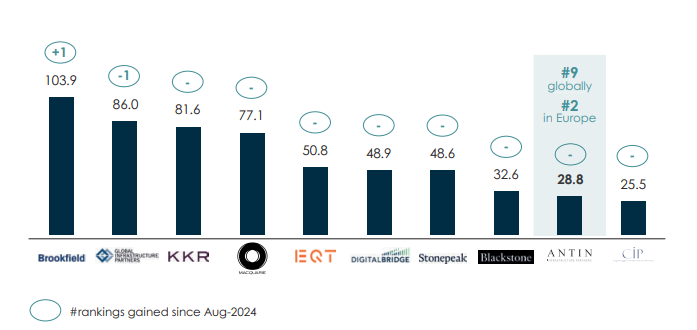

The industry of private equity has concentrated over the last decade, with major companies acquiring asset management companies and consolidating the industry. Antin ranks as the 9th largest asset manager and is currently in a good position with very large funds.

During the next decade there is a risk of Antin being acquired by one of the largest managers as the industry keeps consolidating.

Since inception in 2007, AUM have increased from €0.2bn to €33.8bn AUM:

The Flagship strategy has increased from €1.0bn in 2008 to €10bn in 2022.

New strategies launched to effectively cover a larger share of the infrastructure market

In the private equity, performance is key an Antin has achieved an investment performance of 22% gross IRR and a 2.5x Gross Multiple.

However, it’s not only performance in terms of delivered IRR what matters, but also how long you take to deploy the committed capital and to return it back to investors.

During the last years, this investment activity slew down, as 2022 marked one of the most challenging years in the history of the PE industry. From very high valuations, to a disruption in financial markets with rates increasing exponentially in a few quarters.

The company went public in 2021 at a valuation that was very high. Final IPO price was set at €24 per share, implying a P/E of ~33x and nearly 40x actual earnings. The stock reached an insane valuation of €34.5 per share during 2021 and today the stock trades at ~€10 per share.

I started investing in March 2024, with multiple further acquisitions during 2024 and 2025, implying an average cost of €11.4 per share.

Stock is down 12%, but the investment is only 6% down, as the company offers a 6-7% dividen yield.

Summary of the investment thesis

A forgotten company?

Antin has not performed as I expected when I first invested in 2024. This was mainly a mistake I made, as looking backwards, I should have factored an extended fundraising cycle. This has created uncertainties, and given the illiquidity of the stock, it looks that it’s becoming a forgotten stock.

The firm was slow in deploying capital, which turns to be a positive signal as the investment committees seem to be focused on performance, rather than simply investing capital to earn management fees.

During the last quarters, investment performance has accelerated, with the Flagship fund close to 75% of capital invested, and the Mid-cap strategy almost ready.

Currently, the company is launching multiple sell-side process to exit matures companies of older funds. This will support the new fundraising cycle.

For many quarters, executives avoided to give specific timings on fundraising, due to the uncertainties on investment performance (investments and exits). A reasonable approach to not overpromise and the under-deliver.

The market now is not looking into the details.

New fundraising cycle begins at the end of 2026, which will effectively increase the AUM significantly during the next 3 years

The cycle is supported by exits, which will trigger the first carried interest attributable to the company — an important milestone, although not material at this stage (~€50m in the next couple years)

Earnings will increase in the next years, supporting not only strong cash flow generation but also the current high dividend distributions.

Antin is like buying an investment grade bond offering a 7% coupon. It’s very attractive, yet nobody seem to care

Current DPS stands at €0.7 per share, representing a dividend yield of 7%

This dividend is sustainable as cash generation sufficiently covers this pay-out

During the next years, company will invest ~1% in its own funds (GP Commitment), but current cash and exits will provide cushion to not put at risk the dividend.

Note that share buybacks are not a viable alternative due to the current illiquidity of the stock.

However, it’s more than just a simple bond. There is high margin of safety and potential high upside.

The stock trades at 12x earnings, a low valuation for a high-quality business that provides stable cash flows over extended periods of time.

In the private markets you will never see an asset management company with €30bn of AUM trading at 12x earnings and 7.4x EBITDA.

There will be growth in earnings over the next years through the new fundraising cycle. While value might take time to come, the increasing cash flow generation will support the current 7% dividend yield.