Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

Dear reader,

Today I bring my analysis of IMCD — a leading European company in the specialty chemical distribution.

For this analysis, I will follow again the bullet-point structure to go direct to the point. Please let me know if you enjoy this format or you prefer more text and explanations.

Introduction to IMCD

IMCD is the largest pure specialty chemical distributor in the word, yet it only controls 2% of the market share

Brentag is the largest distributor of chemicals worldwide, but focused on both specialty and commodity chemicals.

In the specialty chemicals space, IMCD is the largest company (€4.8bn revenue), followed by Azelis (€4.2bn).

Despite being the largest company, it only controls ~2% of the market share.

IMCD in a nutshell:

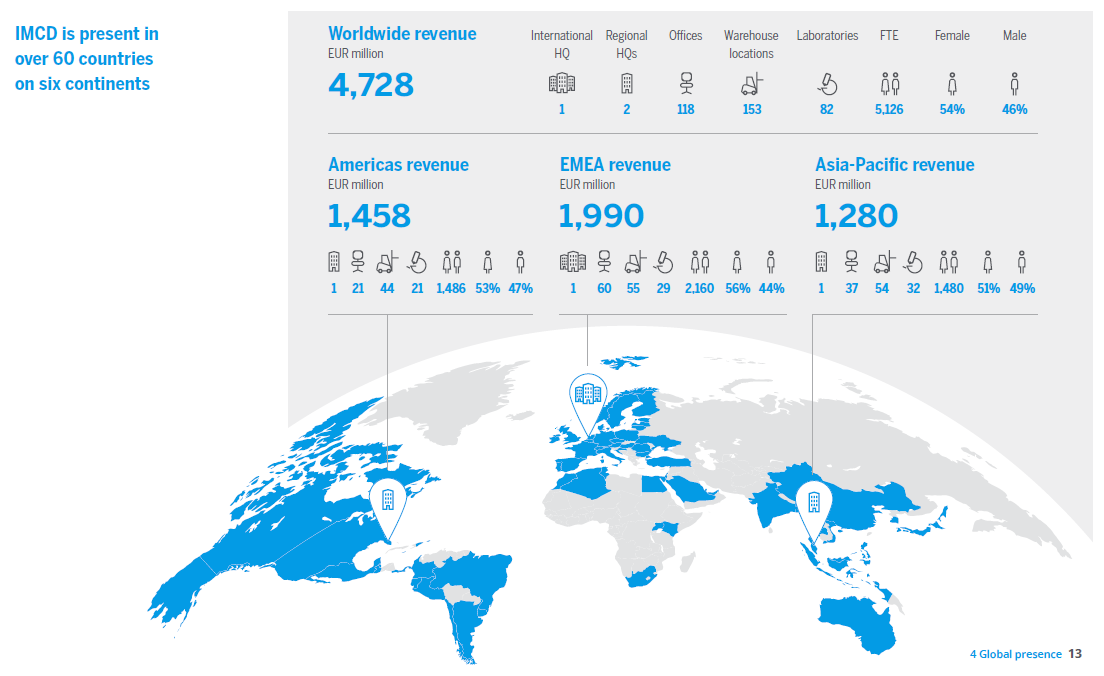

Company is present in more than 60 countries, being Europe the core geography (xx% of total revenue).

The firm employs more than 5,000 people around the world, having 118 offices, 153 warehouses and 82 laboratories.

Company is divided in 8 business groups, which are chemical groups such as beauty, food, construction, etc.

The company has ~68k customers and trades more than 50k products.

The company generates €4.8bn in revenues and a FCF of €280m.

Part I: History of the Company

IMCD was founded in 1995 and went public in 2014, growing from a regional distributor into a global specialty chemicals leader through three PE ownership cycles and over 600 acquisitions

IMCD’s origins trace back to 1995, when Piet van der Slikke carved out a group of companies from the Internatio Müller combine division to create a new specialty chemicals distributor:

In 2001, the company unified its operations on a single IT platform, laying the infrastructure for international growth

By 2004, Internatio-Müller Chemical Distribution had officially become IMCD as a stand-alone business, with revenues of €550 million and ~700 employees

Three rounds of private equity ownership (2001–2014) defined IMCD’s early growth trajectory, built on both organic expansion and acquisitions:

Taros Capital & AlpInvest Partners (~2001–2005). Focus was on pan-European expansion beyond the original Benelux and French base

ABN AMRO Capital (2005–2010). Acquired for ~€300 million. IMCD reached approximately €1 billion in revenue by 2010, driven by acquisitions of smaller specialty chemical distributors across Europe

Bain Capital & KKR (2010–2014). Acquired at ~€650 million valuation. Continued the acquisition-led expansion strategy ahead of the IPO

IMCD listed on Euronext Amsterdam in June 2014, providing capital to accelerate global expansion:

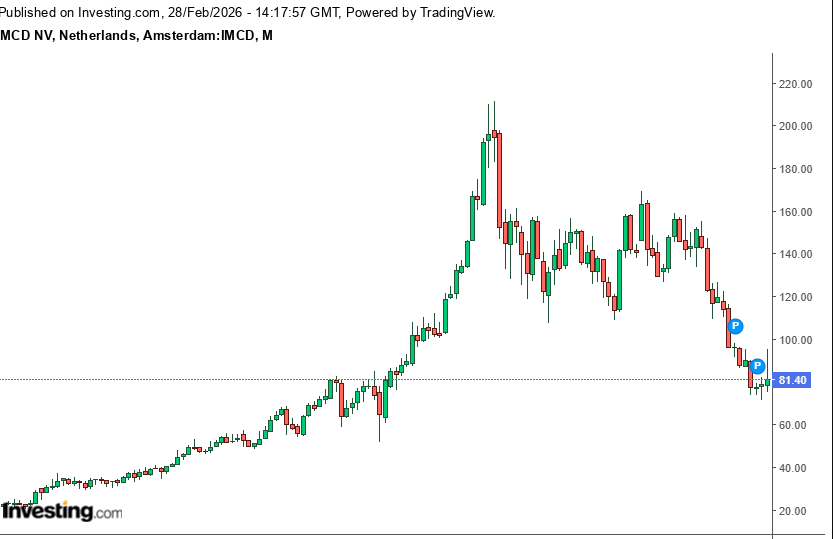

IPO priced at €21 per share (today’s share price stands at ~€80), implying a market cap of ~€1 billion

At IPO, revenue was €1.4 billion and EBITDA margin was ~8%.

Post-IPO growth focused on geographic expansion and building a value-added services platform:

IMCD expanded into North America and strengthened presence across Latin America and Asia.

The company built a global network of technical centers, evolving from pure distribution into a formulation and technical advisory partner

The 2020s brought an acceleration in M&A activity, particularly in Asia Pacific:

In 2021, IMCD accelerated acquisitions across Asia Pacific in personal care, pharmaceuticals, water treatment, and automotive coatings

13 acquisitions completed in 2023 alone; opened first “Beauty Studio” in Paris

12 further acquisitions completed in 2024, bringing the cumulative total to over 600 since 1995

2024 marked IMCD’s 10-year listing anniversary — but also a significant leadership transition:

Share price had grown more than 700% since the 2014 IPO

In January 2024, founder CEO Piet van der Slikke stepped down; replaced by Valerie Diele-Braun

In April 2025, Diele-Braun stepped down for personal reasons; Marcus Jordan (COO, 26-year IMCD veteran) assumed the CEO role

Since the founder’s departure, IMCD has lost nearly 45% of market cap — though this is primarily attributable to financial performance and macro headwinds rather than the leadership change itself

Part II: IMCD Business Overview

1. How IMCD Operates

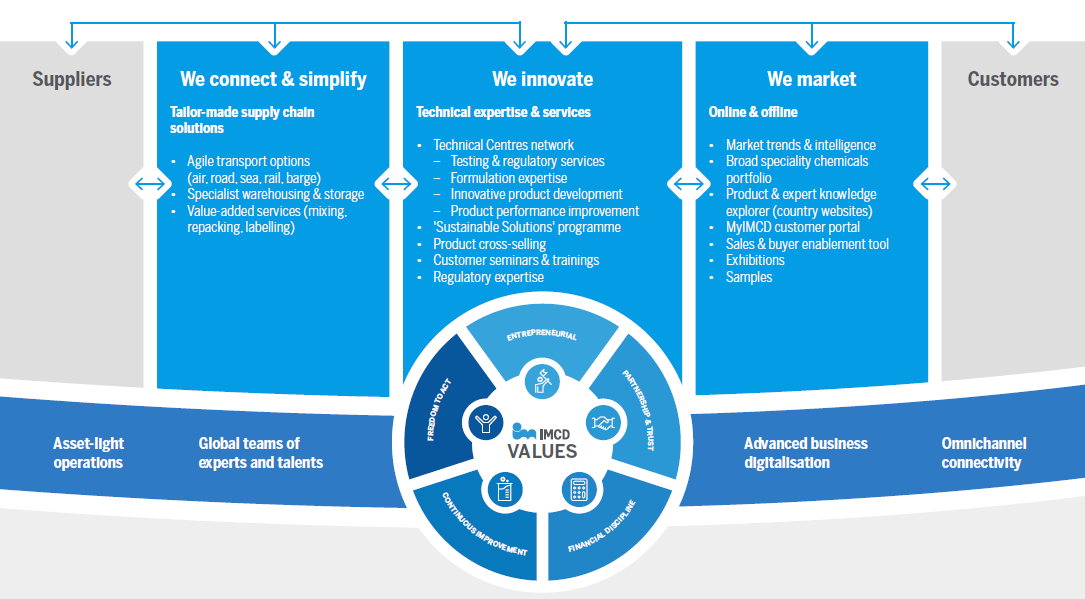

IMCD sits between large global chemical manufacturers and thousands of smaller manufacturing customers, acting as an outsourced sales, marketing and distribution channel that converts suppliers’ fixed distribution costs into variable ones.

What differentiates IMCD from a simple logistics provider is the technical and commercial layer it adds on top of distribution:

Its sales force includes chemists, pharmacists and formulation experts who advise customers on product selection and ingredient compatibility and a deep network of laboratories across the globe.

The model is asset-light, with physical warehousing, logistics and transportation fully outsourced:

IMCD relies on 1,000+ third-party logistics providers for physical distribution

This drives strong cash conversion and capital returns, as the business requires limited fixed asset investment

Growth is driven by two engines:

Organic growth: expanding existing supplier relationships into new geographies and product lines

Acquisitions: exploiting a highly fragmented distribution market where suppliers increasingly want to consolidate around fewer, larger, technically capable partners

IMCD’s scale and network create a compounding competitive advantage:

3,000+ principals (suppliers) in its network

68,000+ customers across 60+ countries

The combination of breadth and technical depth makes replication by either suppliers or competitors structurally difficult

{kind=link}