Dear readers,

Today I’m starting a new section. I will present to you as many companies as I can from my watchlist. These are great companies that for whatever the reason (pricing, temporary issues, etc.), I don’t have in my portfolio.

With this new section I want to:

Learn and share it with the community these ideas with the purpose to extend knowledge and expanding the universe of potential companies joining the portfolio at some time.

Be ready to react when valuation adjusts, temporary issues seem over, etc.

As a new feature, at the end of the post I’m providing a basic financial model with the historical data that I will improve at each new research. Note I’m just including historical data to not influence the way to project financials - that’s something each investor should do, but I’m always happy to give a hand if necessary.

I’m introducing a new concept: the Asymmetric Test, by which I evaluate if a company is interesting if:

Provides an essential or high-value product - Aiming for companies that sell products or services that are essential, irreplicable of high-value.

Sole provider or oligpoly, avoiding industries with lot of competition

Huge barriers to entry, the moat protecting the competitive advantages

Low risk of disruption. I can’t predict who will be the winner in the AI revolution, but I know that the company we are analyzing today will not be disrupted (but will probably be positively impacted)

High earnings power and strong track record of growth, avoiding volatile businesses

Last, but not least, acquired at a low or reasonable valuation. Companies like this do not trade in the value territory, so I’m adding the reasonable term.

Hope you enjoy this new section, that kicks-off with one of the best and most boring companies out there:

Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

Executive Summary

Rollins, Inc. is the parent of Orkin and a family of pest-control brands that together form the second-largest pest-management company in the world and one of the two largest in the United States.

The business is simple to describe and unusually durable: it sends trained technicians to roughly 2.8 million homes and commercial sites to keep insects, rodents and termites away, mostly on recurring contracts, through more than 800 company-owned and franchised locations across some 70 countries

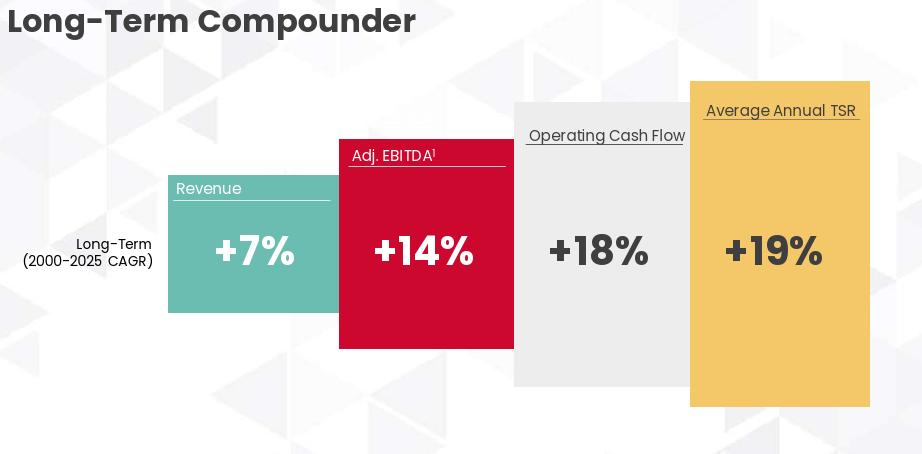

Over the last decade the financial pattern has been remarkably consistent.

Revenue grew from about $1.57 billion in 2016 to $3.76 billion in 2025 — a compound rate near 10% and, by the Company’s own count, a 24th consecutive year of revenue growth

EBITDA margins widened modestly over the same period, from roughly 20% to about 23%

Net income compounded in the mid-teens, free cash flow consistently exceeded reported earnings, and returns on invested capital settled in the low-twenties percent

Leverage is light, at roughly 0.6x net debt to EBITDA at the end of 2025

The industry around Rollins is large, slow-growing and highly fragmented.

Estimates of the global pest-control services market cluster around $26–30 billion, growing in the mid-single digits, with thousands of small operators below a short list of consolidators

That structure is the heart of the Rollins model: organic growth from price and route density, supplemented by a steady stream of bolt-on acquisitions. The principal listed peer, the UK’s Rentokil Initial, became the U.S. market leader after buying Terminix in 2022

The debate among investors is not about business quality but about price.

Rollins has traded for years at a large premium to the market and to its own peer — recently around 48–50x trailing earnings and roughly 31–32x EBITDA — even as the share price drifted lower through 2025 and into 2026

A soft fourth quarter of 2025 (weather-affected) and an FTC order on employee non-compete agreements have added near-term noise

View — Rollins is the kind of business that rewards patience: simple, recurring, low-cyclical, with a long consolidation runway. Whether it rewards a buyer at the current multiple is a separate and harder question.

I. Introduction

What the company does, where it is located, and the industry it operates in

Rollins, Inc. provides pest, termite and wildlife control services to residential, commercial and franchise customers. Its operating brand portfolio is led by Orkin, and includes HomeTeam Pest Defense, Clark, Northwest, Western, Waltham, OPC, IFC, McCall, PermaTreat, Crane, MissQuito, Trutech, Critter Control, Fox Pest Control (acquired 2023) and Saela (acquired 2025), as well as international brands such as Orkin Canada, Orkin Australia, Safeguard (UK) and Aardwolf (Singapore).

The Company is headquartered in Atlanta, Georgia, at 2170 Piedmont Road NE, listed on the New York Stock Exchange under the ticker ROL, and is a constituent of the S&P 500. As of December 2025 it employed roughly 21,900 people across more than 800 company-owned and franchised locations in about 70 countries; about 90% of revenue is generated in the United States, with the balance from a long tail of international markets.

Company history

The Company traces its origins to Rollins Broadcasting, founded in 1948 by brothers O. Wayne and John W. Rollins. The pivotal event in its corporate history was the 1964 acquisition of Orkin Exterminating Company — at that time one of the larger leveraged acquisitions in U.S. corporate history — which transformed the holding company into a pest-control operator. The parent was renamed Rollins, Inc. in 1965 and has traded on the NYSE since 1968

Over the following six decades, Rollins expanded principally by acquisition: dozens of regional and specialty brands have been folded into the group while operating largely under their own names — a deliberate strategy that preserves local brand equity in a service category where reputation travels by word of mouth. In 2024 and 2025 alone, the Company completed 26 acquisitions, including Saela Holdings (2025) for $207.2 million in cash and commercial paper.

II. Business model

What the company does

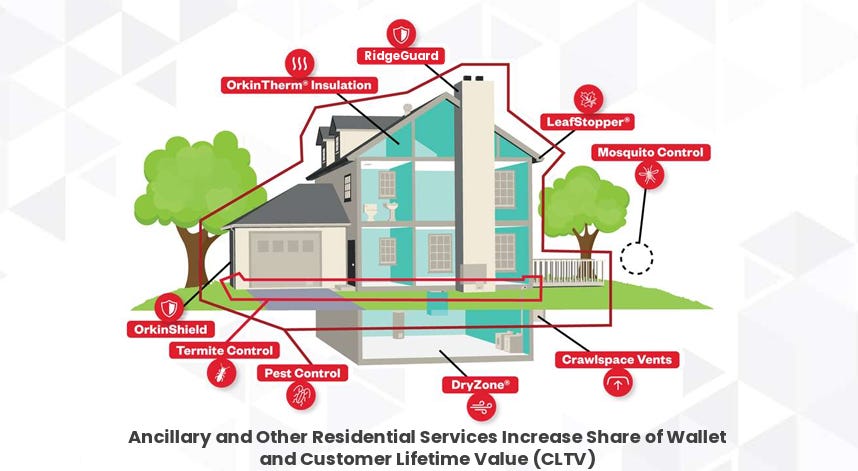

Rollins is a route-based service operator. Pest-control technicians drive an assigned route of homes and businesses, perform an inspection-and-treatment service per visit, and book the work against multi-period contracts. Roughly three-quarters of revenue is recurring (contracted, repeat-cycle visits), about a tenth is ancillary (mosquito, wildlife, attic insulation, related add-ons) and the remainder is one-time termite or initial-treatment work. The franchise programme adds 131 domestic and 66 international agreements that pay royalties on the franchise base.

Segment analysis

Rollins reports a single operating segment but discloses revenue across three service offerings:

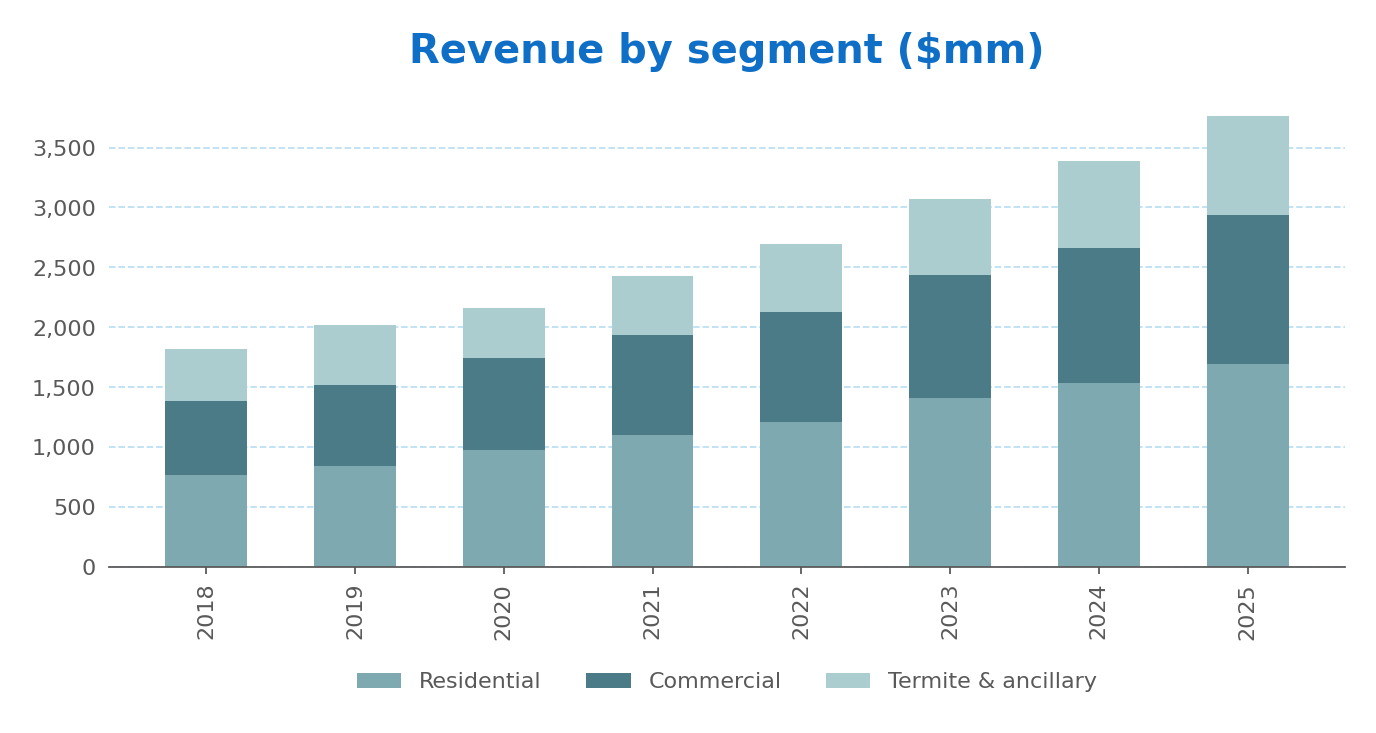

Residential pest control — recurring services to single-family homes against insects, rodents and wildlife. The largest line and the most recession-resistant: roughly 45% of total revenue in 2025, growing at high-single-digit / low-double-digit rates and supported by aging U.S. housing stock and rising consumer focus on hygiene.

Commercial pest control — workplace pest and rodent control for restaurants, food processors, hospitals, hotels and logistics customers, including specialised lines such as bird control. About a third of revenue; mix-shifted to non-discretionary categories where pest management is a regulatory and reputational necessity rather than a preference.

Termite & ancillary — termite treatment and prevention (Sentricon baiting, liquid soil treatments, wood treatments), termite pretreatment work supplied to homebuilders through HomeTeam and Northwest, plus mosquito control, attic insulation and franchise-related revenue. The fastest-growing of the three (14% in 2024, double-digit in 2025) and one of the highest-margin.

The three lines are different in seasonality and elasticity but share the same field workforce and route economics, which is part of why Rollins runs them as one segment.

Geography has been remarkably stable: international has hovered around 7% of revenue across the period, growing roughly in line with the U.S. business. The Company has consistently described the U.S. as its core market and international as a long-term option.

The economic engine common to all three lines is route density. Because a technician’s day is dominated by drive time, packing more nearby accounts onto each route lowers cost per visit and lifts margins; this is why local market share, branch network coverage and acquisition of nearby small operators are central to the strategy. The proprietary BOSS field-operating system feeds technician routing, scheduling, billing and customer history, and is treated by the Company as a core piece of operating infrastructure.

Two pieces of infrastructure quietly drive the franchise.

Brand portfolio. Orkin is among the most recognised names in the category, supported by decades of advertising spend (advertising expense $128.5 million in 2025; $119.6 million in 2024). Recognition lowers customer-acquisition cost; the multi-brand approach lets Rollins serve different price points and channels without cannibalising Orkin.

Route density. Once a market is densely populated with accounts, each new account is cheaper to serve than the average, which improves margins as a route fills out. Density also creates a local cost advantage for the leader that single-van entrants cannot match on a route-by-route basis. This is a key ratio for the industry, the cost-to-serve.

Main customers

Rollins serves more than 2.8 million customers across three buckets:

Residential. Mass-market homeowners and renters. The unit economics are small per account ($30–$50 per visit typically) but the cohort is very large and high-retention. There is no concentration risk: even the largest residential account is a rounding error in revenue.

Commercial. Food-service, food-processing, hospitality, healthcare, education, logistics and property-management customers. Many of these are bound by health-code and audit requirements that make routine pest service a compliance line, not a discretionary one. Contracts are typically multi-year and renew at high rates.

Franchise & other. Rollins franchises certain Orkin operations domestically and internationally (131 domestic, 66 international agreements), generating royalty income, and runs small specialty lines (Trutech, Critter Control wildlife). This segment is small but capital-light.

No single customer is material to the whole. The diffuse, contract-based customer book — millions of small recurring relationships rather than a few large ones — is itself a source of stability: revenue does not hinge on any one account, and high retention rates across the industry (peers cite mid-80s percent) mean the installed base compounds quietly from year to year.

The company has multiple ways to cross-selling its services as there are many different issues arising in a house, which are impacted by different insects.

In commercial segment, there are clear tailwinds from regulation, brand reputation, etc. It’s reputation, potential lawsuits, inventory write offs, etc. It’s not worth not having Rollins doing the service.

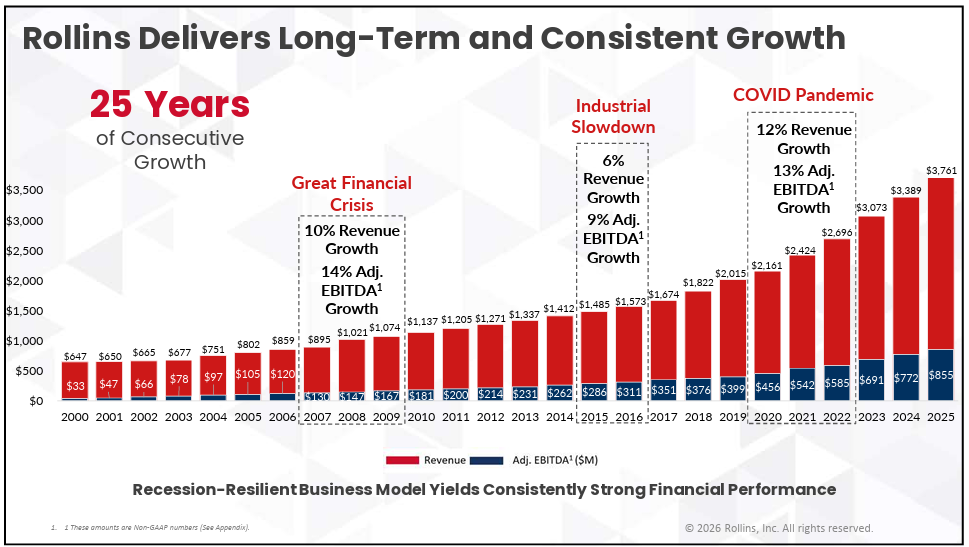

One of the most resilient companies on earth

This chart summarizes why Rollins trades at a premium multiple over many companies: 25 consecutive years of revenue growth.

In the Great Financial Crisis: +10%

Covid pandemic: +12%

In a crisis, people stop buying unnecessary things, but will keep using Rollins services. As simple as that.

III. Industry overview

Market size and how the industry is evolving

Pest control is a large, mature and slowly growing services market.

Independent estimates vary with scope and definition, but the global pest-control services market is generally placed in the region of $26–30 billion in 2024–2025, with projected compound growth in the mid-single digits (roughly 5–6.5%) out to the early 2030s

North America generated about $9.5 billion in 2024 revenue and is forecast to reach roughly $16.5 billion by 2034 (~6% CAGR), making it the largest single region (~36% of the global market)

The U.S. market specifically is sized at roughly $23–29 billion across providers, with the same mid-single-digit growth profile

Growth drivers are structural and unglamorous — but the data behind them is concrete.

Urbanisation and housing density. Per the U.S. Census Bureau, roughly 80–83% of the U.S. population already lives in urban areas, with forecasts pointing to ~89% by 2050; there are around 131 million occupied housing units in the country, an aging stock that creates ongoing pest-entry points. Multi-family housing and high-density living facilitate pest spread between connected structures

Climate change and lengthening pest seasons. The CDC reports more than 1.6 million U.S. cases of mosquito-, tick- and flea-borne disease between 2004 and 2023, and uses Lyme disease as an EPA climate-change indicator. Warmer winters and longer summers extend tick and mosquito activity windows and push their geographic range northward; termite ranges are also expanding

Tightening hygiene and food-safety regulation. Audit-driven commercial demand from food-service and healthcare customers continues to grow, particularly post-COVID, with surveys showing 85–90% of consumers more attentive to hygiene in public spaces.

Shift from DIY to professional service. In residential, the long-running migration from do-it-yourself sprays to contracted professional service supports volume growth on top of which operators layer annual price increases.

None of these drivers is dramatic on its own, but together they support steady volume growth on top of which operators layer annual price increases.

Why customers buy, how critical the service is, and what that means for pricing power.

Why they buy. On the commercial side, pest control is a compliance and reputation line — a positive rodent or insect finding can shut down a restaurant, fail a food-safety audit or trigger headlines for a healthcare facility, making the service close to non-discretionary. On the residential side, the work delivers protection-of-the-home value (peace of mind, prevention of termite or rodent damage) where the annual cost is modest relative to the asset being protected.

How critical. The cost of a pest-control contract is small relative to the cost of failure. A termite infestation can cause structural damage to a home that, according to the Company’s own materials, sums to roughly $5 billion in U.S. property damage each year, most of it not covered by homeowner insurance. A commercial pest incident can mean a temporary closure. The asymmetry — small recurring fee versus large potential downside — anchors customer willingness to pay and supports retention.

Pricing power. Rollins has been able to take low-to-mid-single-digit annual price increases without unusual churn. Organic revenue growth ran in the high-single digits through 2024–2025 with most of the contribution from pricing and the balance from volume / cross-sell. Adjusted EBITDA margins widened from roughly 20% in 2016 to ~23% in 2025, consistent with pricing exceeding cost inflation. The diffuse customer base — no single account is material — gives the Company leverage when re-pricing.

View — Customers buy a small recurring service to insure against an asymmetric downside; that economic structure, more than any single product feature, is what underwrites Rollins’ pricing power.

The most important structural feature, for an investor, is fragmentation. The United States alone is served by roughly 32,700 pest-control firms (per industry estimates), the great majority small, single-branch local operators, with median annual revenue around $400,000. Only a handful of companies have national scale. That long tail is the raw material for consolidation, and it is why the largest players can grow faster than the underlying market by acquiring routes year after year.

Competitors: an oligopoly at the top of a fragmented base

The competitive structure is best described as a fragmented market with a consolidated top. At the apex sit two listed leaders and a small number of large international or private players; beneath them lies the long tail of local firms.[33]

Listed leaders.

Rentokil Initial plc (LSE: RTO). UK-listed and the global #1 by revenue (~£5 billion in 2024). Acquired Terminix in October 2022 to become the largest pest-control operator in the U.S. by route count, then spent 2023–25 working through a complex integration. Rentokil EV/EBITDA has tracked roughly half of Rollins for the past two years, partly reflecting weaker organic momentum and integration cost.

Rollins, Inc. (NYSE: ROL). Cleaner business mix (more residential and small-commercial), no comparable large acquisition to digest, and consistently higher margins (~23% adjusted EBITDA vs. high-teens for Rentokil). Trades at a premium reflecting this.

Non-listed competitors of note.

Anticimex. Privately held, owned by EQT, sizable European footprint with a growing North American business. Known for a digital/Internet-of-Things-enabled commercial offering.

Truly Nolen, Aptive Environmental, Massey Services and roughly 32,000 local independents. The long-tail competition. Individually small, collectively large; the substrate of the M&A roll-up.

Competitive advantages

Rollins competes on three advantages, all of which compound over time.

Brand portfolio. Orkin is one of the most recognised category brands in the U.S.; recognition lowers customer-acquisition cost and reduces residential price sensitivity. The multi-brand strategy lets Rollins reach different price points and acquire local champions without cannibalising Orkin.

Route density. Local market share is the single most important driver of route economics. As accounts cluster, drive time per visit falls, technicians become more productive and margins expand. This is a competitive advantage held by the local leader in each market — Rollins is the local leader in a large share of its markets — but it is created and re-created continuously by good operations.

M&A engine. Three decades of disciplined small-deal acquisition (94 acquisitions in the last three years, including a step-up to Saela in 2025) is, in the Company’s own framing, the mechanism by which the leaders compound faster than the underlying market. Pricing on these deals is generally not disclosed in detail but appears to fall in a multi-of-cash-flow band well below where Rollins’ own equity trades, creating real value when integrated.

View — These are all genuine competitive advantages, but they are advantages a serious competitor could match in any single market. The question for the moat is whether the combination is harder to replicate at national scale than any one piece.

Is there a moat, and what could erode it?

A moat — a structural barrier to entry, not just an operating advantage — does exist here, but it is narrower than the headline competitive advantages suggest.

What constitutes the moat. The combination of:

(a) customer switching cost — once a homeowner is on an annual contract with a technician who knows the property, switching is friction-rich for a small absolute saving (but, let’s be honest, this is a modest barrier);

(b) brand trust at point of decision, which is unusually concentrated in Orkin; and

(c) national scale across thousands of routes that no single local entrant can match. Each piece is modest; the durability is in how slowly any of them erodes.

What is not the moat. Local route density, technician training and BOSS scheduling are operating advantages, not moat f9eatures in the strict sense — a well-run competitor in a given market can build them too. They underwrite returns; they do not by themselves prevent entry.

The risks to the moat are worth stating plainly.

Barriers to entry at the small end are low — a van, a licence and a sprayer will start a local firm — so the threat is not a single disruptive entrant but ongoing margin competition at the bottom.

Rentokil has the scale and capital to match many of Rollins’ advantages and is the credible peer challenger in the U.S.; integration noise has been a tailwind to Rollins, but that is not permanent.

The U.S. Federal Trade Commission’s 2025 order narrowing post-employment non-compete restrictions could, over time, increase technician mobility and modestly raise the cost of retaining experienced field labour, particularly at the commercial end

Climate variability cuts both ways: longer pest seasons and expanded ranges add demand, but unusually warm or wet quarters can also pull demand forward and create the kind of weather-driven quarterly volatility that hit fourth-quarter 2025.

View — The moat is genuine but narrow, and it depends as much on continued execution as on structural protection. The most plausible long-term threat is not disruption but slow compression of the small-deal acquisition spread that has powered the M&A engine.

IV. The management

Key executives, backgrounds and reputation

Jerry E. Gahlhoff, Jr. — President & Chief Executive Officer. Gahlhoff became CEO in January 2023 after serving as President and COO. He is a trained entomologist and a career operator in pest control, having joined Rollins through the HomeTeam Pest Defense business; he is regarded internally and externally as a domain expert who rose through operations rather than finance.

The separation of the CEO role from the Chairmanship — formalised when he became CEO — is viewed by the board as appropriate governance.

")

Kenneth D. Krause — Executive Vice President & Chief Financial Officer. Krause joined as CFO in September 2022 from MSA Safety, where he had been Senior Vice President, CFO, Chief Strategy Officer and Treasurer; before that he held finance leadership roles at MSA dating to 2006. He brings public-company finance and capital-allocation experience and has been associated with a sharper focus on margin, free-cash-flow conversion and disciplined leverage since arriving; he features prominently in the Company’s investor communications on profitability.

John F. Wilson — Executive Chairman; Gary W. Rollins — Executive Chairman Emeritus. Wilson, a long-tenured Rollins executive, serves as Executive Chairman. Gary W. Rollins — a member of the founding family who led the Company as CEO from 2001 to 2022 and oversaw much of its modern compounding — remains Executive Chairman Emeritus.

")

The leadership structure deliberately keeps the founding family close to the board while leaving day-to-day operations with a professional, operator-CEO.

Reputationally, the management team is generally well regarded for operational consistency and conservative finance; the principal external critique is not of competence but of the stock’s valuation. The board added experienced outside directors in recent years (including search and governance specialist Dale Jones, and Lead Independent Director Louise S. Sams), which is consistent with a maturing governance posture at a founder-controlled company.

Ownership and skin in the game

Ownership is the defining governance fact at Rollins.

The founding Rollins family — principally through Gary W. Rollins, family members and the family holding vehicle LOR, Inc. — has historically controlled approximately 38% of the shares outstanding. This is a controlled company in substance: the family’s vote effectively determines major board decisions, and major capital actions have repeatedly involved family liquidity events.

Two large secondary offerings have moved family stock into broader hands: a 2023 sale of 38.7 million shares at $35.00 (with the Company repurchasing 8.72 million shares for ~$300 million at $34.39), and a 2025 sale of 17.4 million shares at $57.50 (with the Company repurchasing 3.48 million shares for ~$200 million at $56.93). These transactions reduced the family’s percentage stake somewhat but left it firmly in control.

Day-to-day executives (Gahlhoff, Krause) hold meaningful but not controlling stakes built through annual equity grants. Insider transactions in 2024 and 2025 have been overwhelmingly programmatic sales (10b5-1 plan distributions of vested stock) rather than open-market purchases or sales — there has been no notable CEO or CFO open-market buying in 2025–26.[43]

View — Skin in the game is real but concentrated at the family rather than the operator level. For minority shareholders, this is mostly good — the family’s interests are long-term and shareholder-aligned — but it does mean that the most material capital decisions are made by people who already own a great deal of stock, and would gradually reduce the family stake.

Compensation and alignment of interests

Executive pay follows a conventional three-part structure:

Base salary. A modest fixed component; for the CEO it has been around $1 million per year. Salary is not the principal lever of alignment.

Annual performance-based cash incentive (bonus). The plan divides the bonus into two components, each tied to a financial target. Per the Company’s own bonus-plan documentation, the Pre-Tax Profit-to-Plan component pays up to a maximum of 90% of annual salary if profit reaches or exceeds the Board-approved annual plan (with pro-rata payment between 95% and 100% of plan), and the Revenue-Growth-to-Plan component pays up to 60% of annual salary on the same scale. No bonus is paid under any component if the Company’s pre-tax profit does not improve year-on-year — a ‘circuit-breaker’ that ties the bonus to absolute earnings progress, not just plan achievement. The combined maximum cash bonus is therefore 150% of salary

Equity-based awards. The largest part of the package: restricted stock and performance-share units vesting over 3–4 years on a mix of time- and performance-conditions (revenue growth, EPS growth, total shareholder return). For both the CEO and CFO, equity has been the dominant share of total reported compensation; the Company does not currently grant stock options.

Reported pay for the two operating executives looks like this (fiscal 2024, per the 2025 Proxy Statement and parsed regulatory data):

CEO Jerry Gahlhoff — total compensation ~$8.2 million for fiscal 2024 (estimated by Quiver Quantitative from the Company’s 2025 DEF14A: ~$6.7 million in fiscal 2023 and ~$9.0 million in fiscal 2025), with the substantial majority delivered in equity awards. The CEO pay-mix is salary in the low-millions, two-component cash bonus (capped at 150% of salary), and the remainder in performance-conditioned stock — i.e. the operator’s outcome is more sensitive to the share price than to either his salary or his bonus.

CFO Kenneth Krause — total compensation ~$4.2 million for fiscal 2024 (roughly $0.77 million salary, $0.78 million cash bonus and ~$2.6 million in stock awards, with no stock options) — a mix in which equity again clearly dominates.

Stock-ownership guidelines reinforce the equity emphasis: the CEO is required to hold Company stock with a value equal to six times base salary, the CFO three times, with five years to comply.

View — The structure is conventional and shareholder-aligned. Cash compensation is modest, the bonus has a clean circuit-breaker tied to actual profit improvement, and the dominant equity component means that operators’ wealth tracks shareholders’ wealth in both directions. The principal limitation is that the long-term incentive metrics — revenue, EPS, TSR — are output measures rather than capital-efficiency measures, which would be a constructive addition over time.

Recent insider trading

Insider activity over the last 24 months has been dominated by family secondary sales (Gary W. Rollins voting trusts and Randall Rollins voting trusts collectively reducing positions through registered offerings), and by programmatic small disposals by named officers under 10b5-1 plans. There has been no material open-market buying by the CEO, CFO or COO in 2024–26, and disposals by named officers have been small in dollar terms relative to their remaining stakes — net, a ‘no signal’ read.

Sources: Rollins, Inc. Definitive Proxy Statement (Schedule 14A) filed March 13, 2025; 2023 Executive Bonus Agreement (Justia public archive of Company filing); Quiver Quantitative parsing of 2025 DEF14A; SEC Form 4 filings via GuruFocus and StockTitan.

V. Financial analysis

6.1 Revenue

Rollins’ revenue line is the cleanest part of the story.

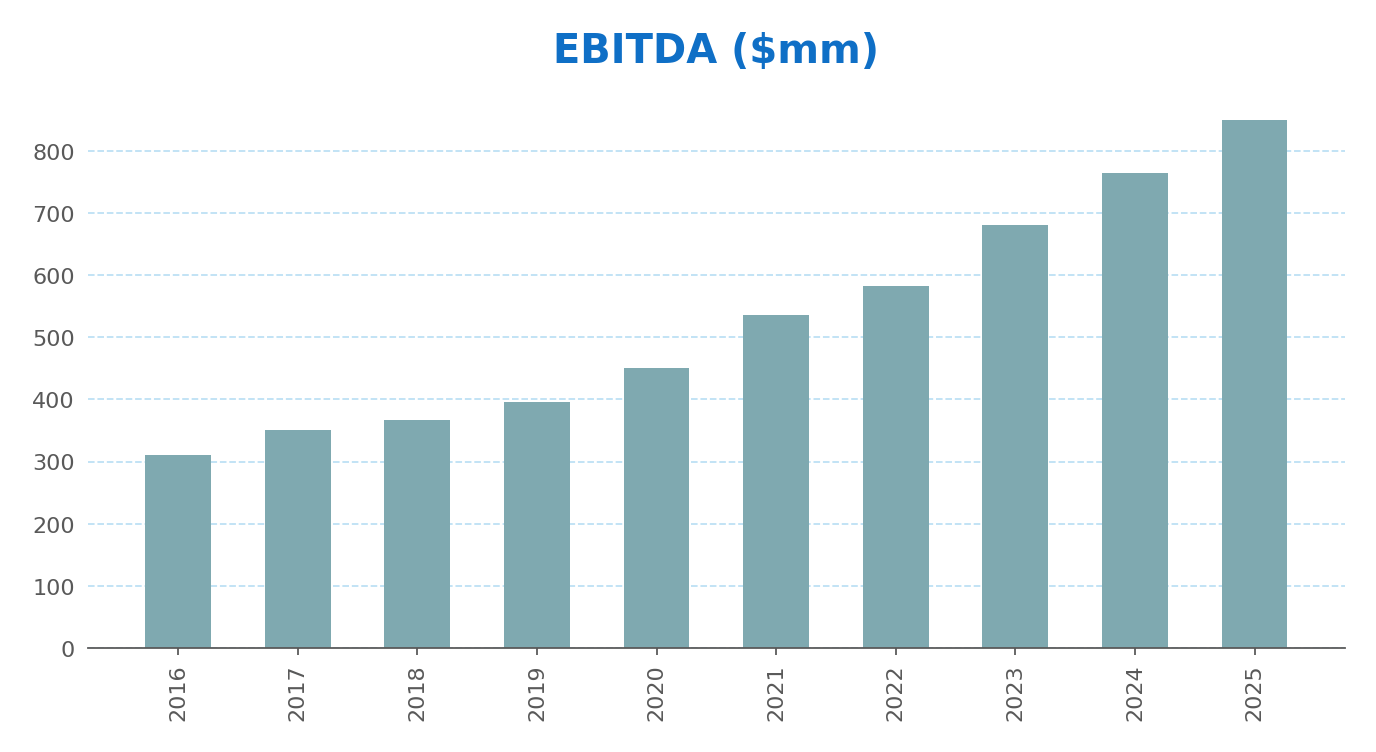

Total revenue compounded from $1.57 billion in 2016 to $3.76 billion in 2025 — a 9.8% CAGR over nine years and a 24th consecutive year of revenue growth by the Company’s count.

Growth has been a mix of price, volume and acquisitions. The Company discloses an ‘organic’ revenue measure (excluding revenue from the trailing 12 months of acquisitions): organic growth has run at 7–9% through most of 2024 and 2025, with M&A adding 2–3 points on top.

By segment, termite and ancillary has been the fastest-growing line (14% YoY in 2024, double digit in 2025), supported by Sentricon baiting and HomeTeam pretreatment work; residential and commercial each compound in the 9–11% range.

By geography, growth has been remarkably balanced: US and international both compounded at ~11.7% over 2020–25; international remained ~7% of total revenue throughout.

Price-versus-volume disclosure is not fully granular, but Company commentary on quarterly calls is consistent with most of the organic growth in 2024–25 having come from pricing rather than account count — i.e. customers are paying more per visit, with modest underlying account growth. This is the textbook signature of a route-density business with limited cyclical exposure.[51]

EBITDA and operating income

Margins have expanded slowly and steadily.

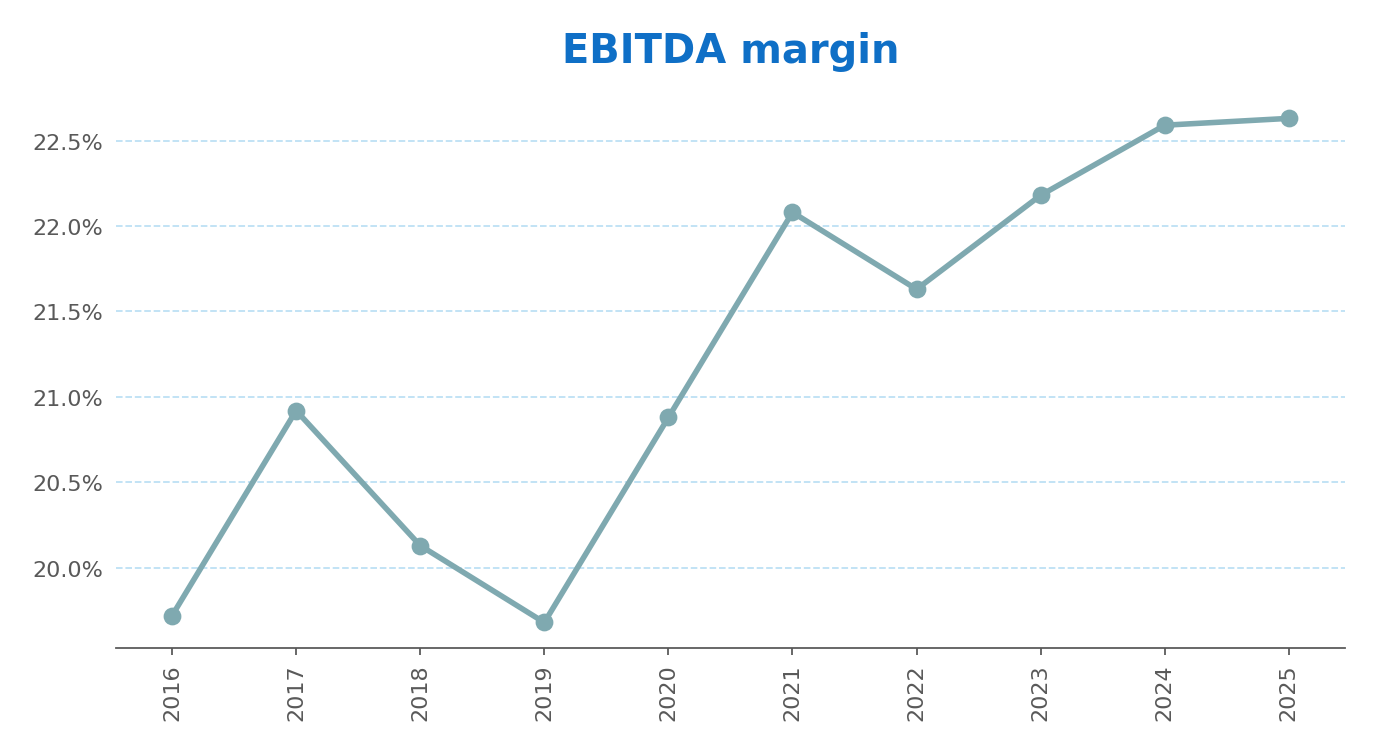

EBITDA margin (Revenue + Cost of services + SG&A + restructuring, in the model’s negative-expense convention; equivalent to the GAAP gross-profit-less-SG&A construct) widened from roughly 20% in 2016 to about 23% in 2025, on revenue that has more than doubled.

Operating margin followed: from ~17% in 2016 to ~19% in 2025.

The path was not perfectly linear — FY2019 saw a non-cash pension settlement, FY2022 included property-disposal gains, FY2023 carried a $5.2 million restructuring charge, FY2025 saw insurance-claim noise — but the underlying trend is up.

Rollins’ own ‘Adjusted EBITDA’ (which adds back acquisition-related items) ran at 22.8% of revenue in 2024 and ~23% in 2025; the Company’s own framing of margin progression is therefore very close to the GAAP-based picture, which is a sign of low non-GAAP intensity by U.S. large-cap standards.[54]

View — Margin expansion has come from operating leverage and price, not from heroic cost-cutting. That is the right pattern for a service business — it suggests the gains are stable rather than one-off.

Earnings and free cash flow

Earnings and cash flow tell the same story as revenue and margin, only better.

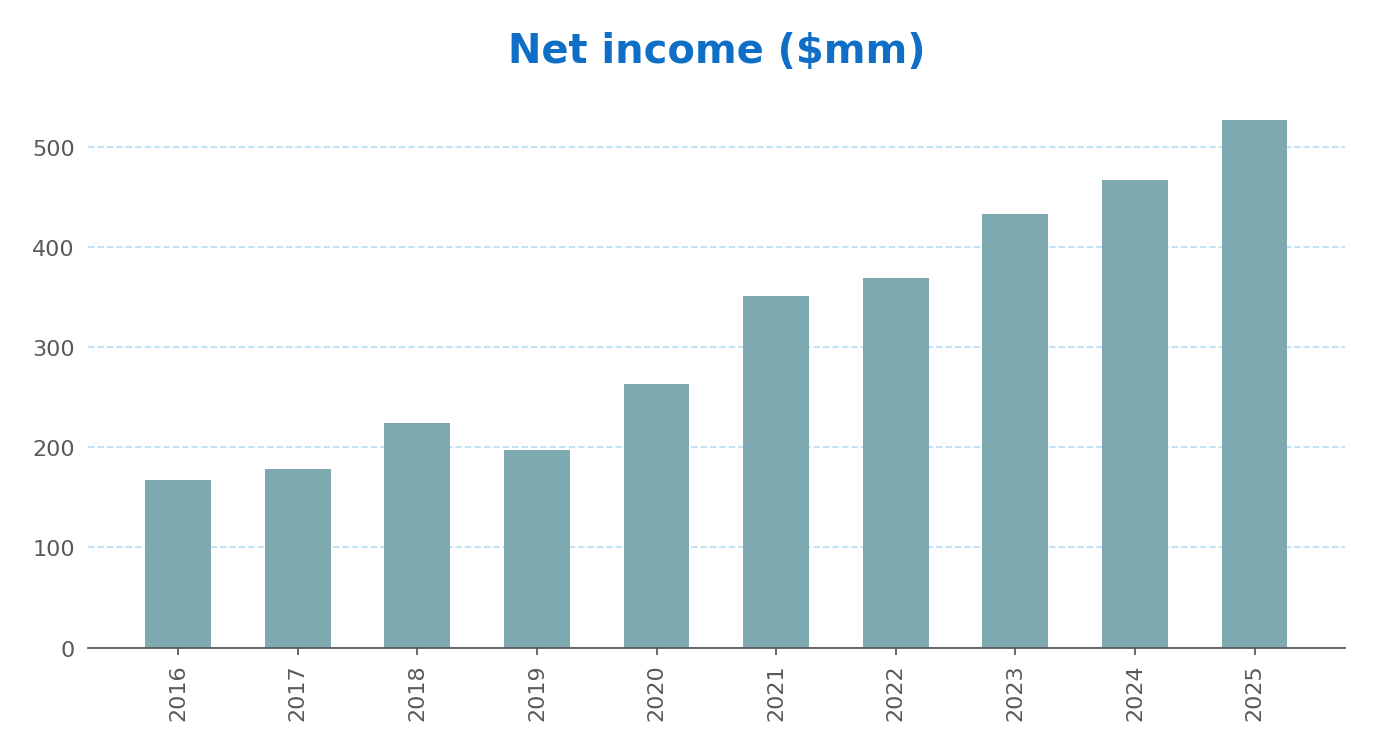

Net income rose from $167 million in 2016 to $527 million in 2025 — a 13.6% CAGR — and diluted EPS from $0.34 to $1.09 on a share count that is essentially flat (split-adjusted) over the period.

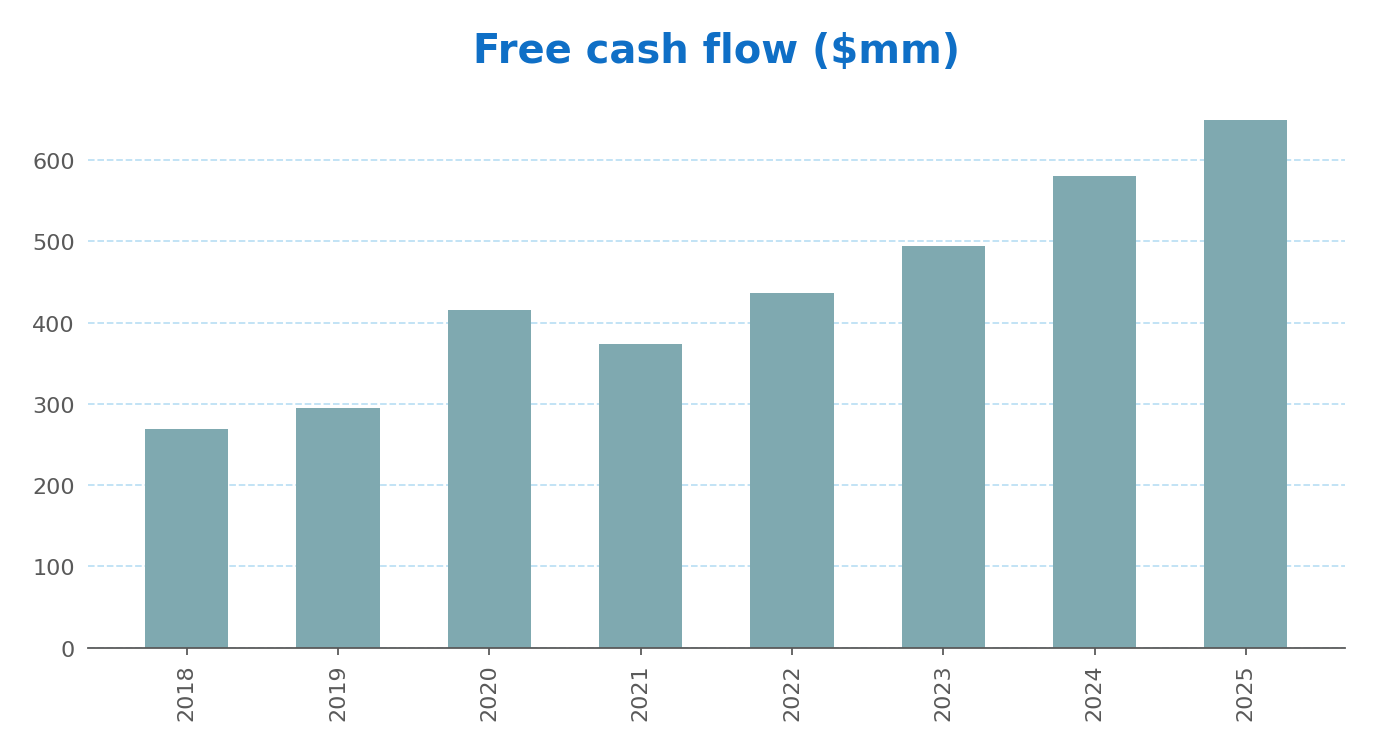

Free cash flow (CFO less capex) has consistently exceeded reported net income — a quality marker. FY2025 free cash flow was about $650 million on net income of $527 million, an FCF conversion ratio of 123%.

Capex is structurally light — under 1% of revenue — because the business is essentially routes and people rather than fixed plant. Working-capital absorption is modest given the recurring billing model.

Stock-based compensation is small relative to FCF ($40 million in 2025 vs. $650 million FCF); on the firm’s preferred ‘Asymmetric Ventures’ definition (CFO less capex less SBC), FCF was about $610 million in 2025.

This is part of the family’s 2023 and 2025 secondary sales: cash-flow conversion above 100% of net income is a recurring feature and a guidance point for 2026.

Balance sheet

The balance sheet is conservative.

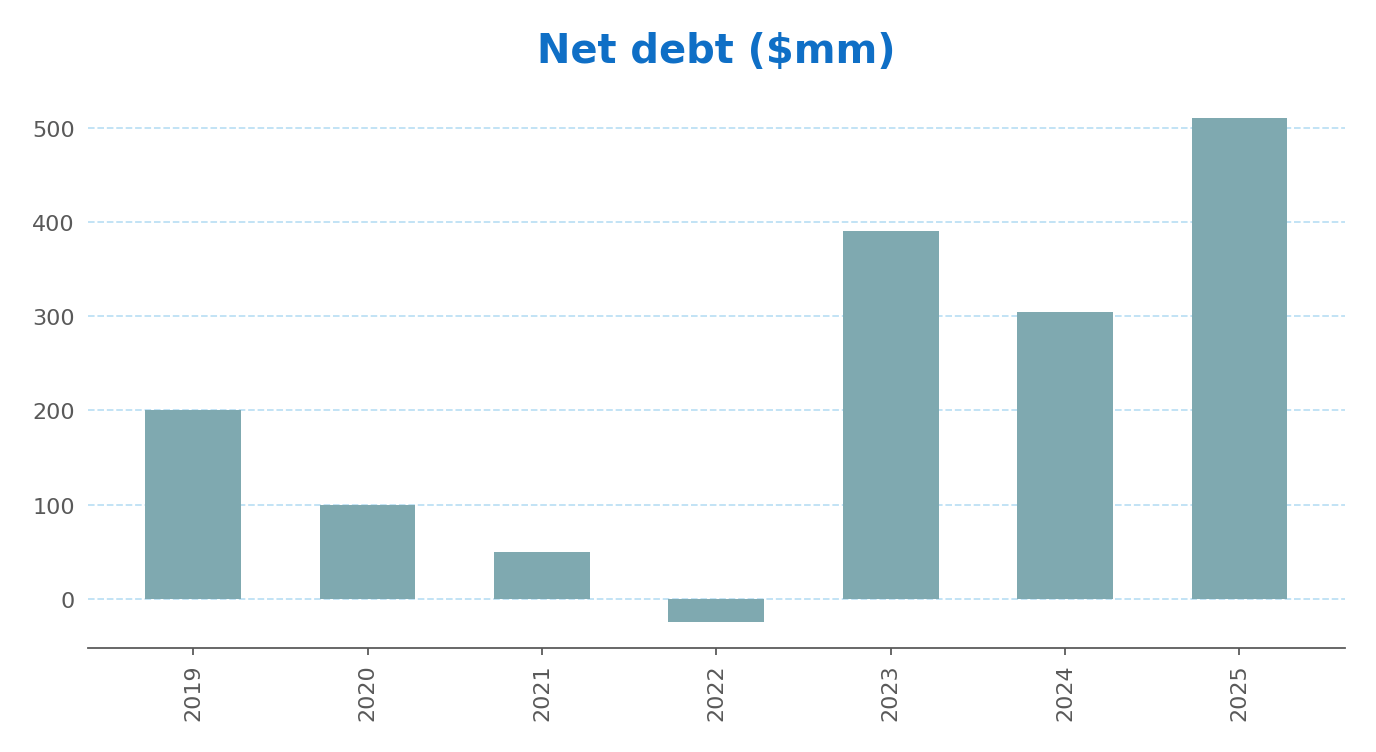

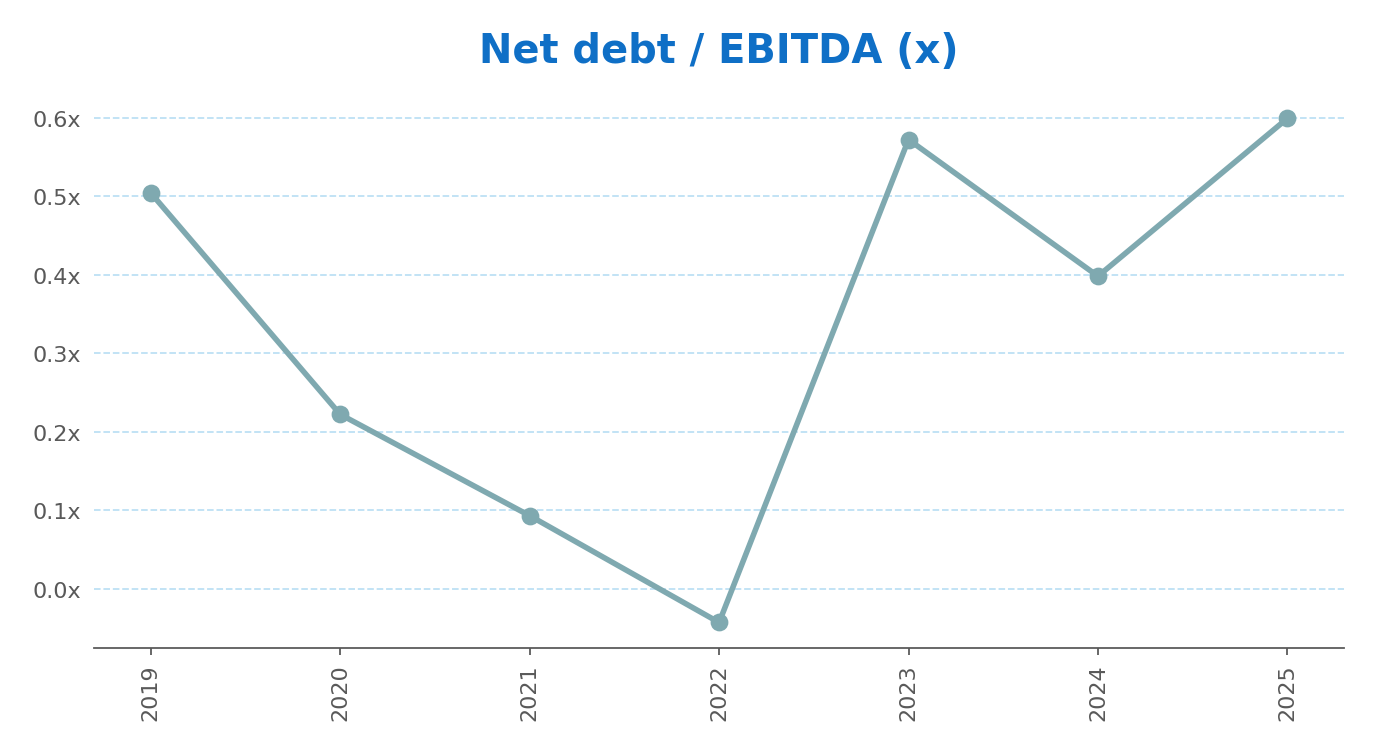

Net debt at the end of 2025 was about $510 million against EBITDA of about $851 million — roughly 0.6x — and the Company’s own leverage ratio (which capitalises leases) stood near 0.9x.[59]

Debt is modest and well-termed, including a $500 million senior note due 2035 and a commercial-paper program backed by a $1.0 billion revolving facility. The Company has at times operated in a net-cash position (2022) and has comfortably re-levered to fund acquisitions and buybacks since.

Two balance-sheet nuances are worth flagging for completeness.

Goodwill and intangibles are large relative to total assets — an arithmetic consequence of a business built by acquiring hundreds of companies — so reported book equity is not a meaningful guide to value, and tangible capital is small.

Off-balance-sheet and contingent items are ordinary-course: operating-lease obligations (captured in the leverage ratio); routine litigation and insurance reserves; an environmental matter in California settled in 2025; and the FTC non-compete order, which the Company expects to be immaterial financially. Earn-out and contingent-consideration liabilities arise from the acquisition programme but are individually small.

View — There are no obvious hidden assets and no alarming hidden liabilities. The asset-light, goodwill-heavy structure is exactly what one expects from a serial acquirer of service routes; the key point is that the returns must be judged on cash flow and ROIC, not on book equity.

6.5 Capital allocation

Capital returns to shareholders have been steady, growing and disciplined.

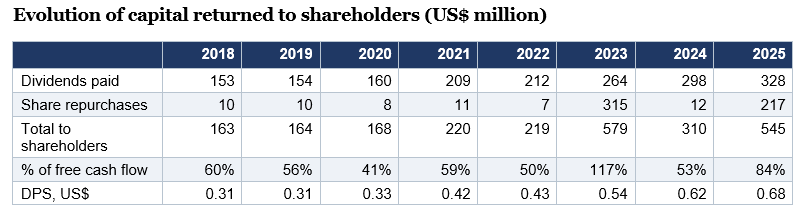

Dividends per share have grown every year of the decade, from $0.222 in 2016 to $0.6775 in 2025 — a 13.2% CAGR. The trailing dividend yield at recent share prices is approximately 1.2–1.3%, modest in absolute terms but reflecting that the stock trades at a low free-cash-flow yield. A special dividend in 2020 (during the pandemic) is the only step in the otherwise smooth growth pattern

The payout ratio (dividends divided by net income) has hovered in the 55–63% range across the decade — a high but stable share of earnings — and the dividend-to-FCF ratio is lower (49% in 2025) reflecting FCF in excess of net income.

Share repurchases have been event-driven, not programmatic: small amounts in most years ($8–11 million for net-of-tax-related buying), with two large bursts coinciding with the family secondary offerings — $315 million in 2023 (8.72 million shares at ~$34.39 average) and $217 million in 2025 (3.48 million shares at ~$56.93 average). Outside those two windows, the buyback has not been a meaningful capital-return lever.

Together, dividends and buybacks have absorbed about 67% of cumulative free cash flow from 2018–25; acquisitions account for most of the balance, with very modest organic capex.

Notes: Free cash flow defined as CFO less capex. The 2023 % of FCF exceeds 100% because the $315 million repurchase was funded partly with new debt; the 2025 figure reflects a similar but smaller pattern.

View — Capital allocation is in the right spirit — high cash conversion is mostly returned to shareholders, with small-deal M&A absorbing the rest. The mainly opportunistic, family-aligned buyback pattern is a feature rather than a flaw: management has not destroyed value chasing the share price at every level.

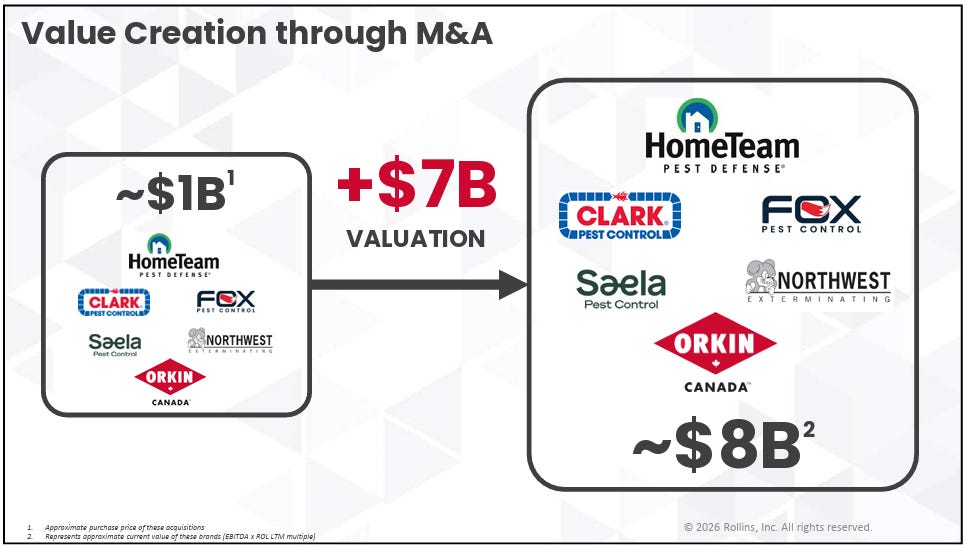

M&A is one of the core engines of value creation. The company acquires companies significantly below their premium valuation, instantaneously creating value through multiple re-rating.

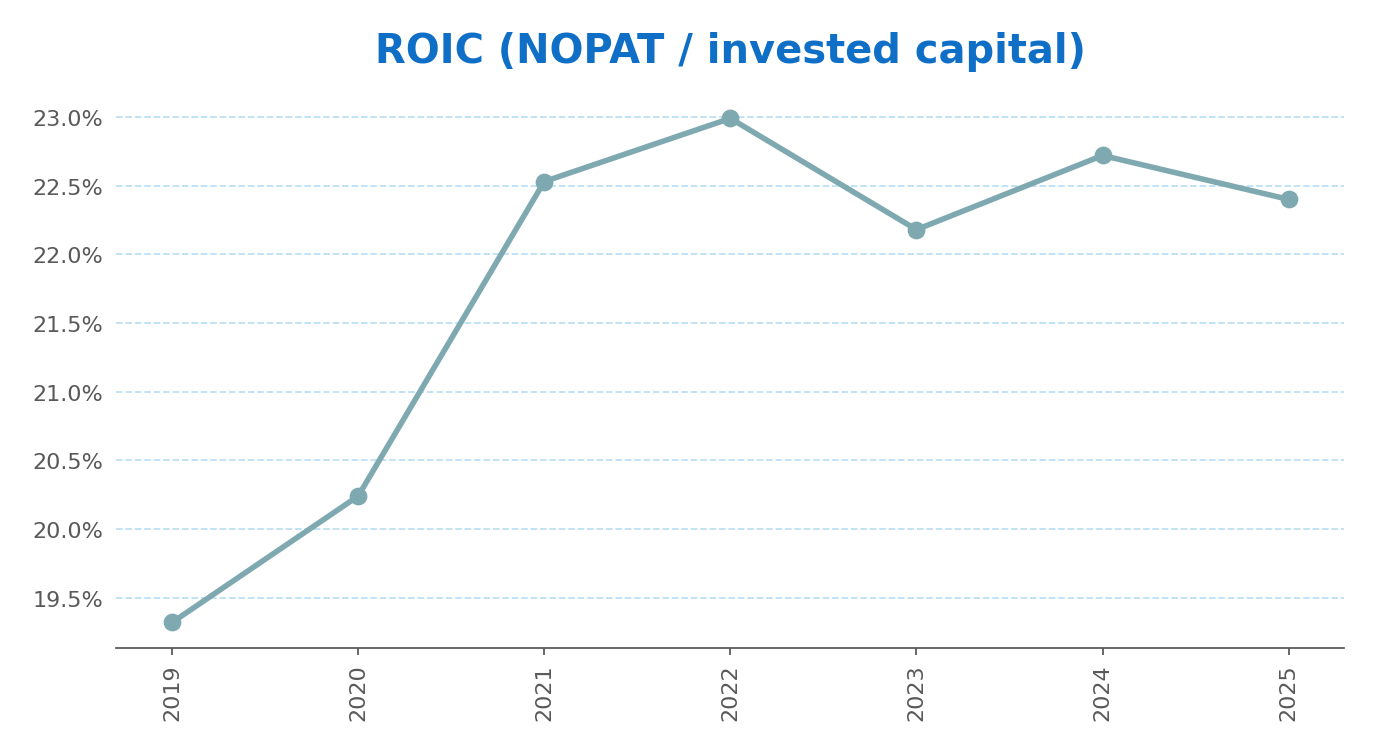

Return on invested capital

Returns on capital are the clearest quantitative signature of business quality, and here Rollins scores well.

On the model’s definition — NOPAT over invested capital (operating working capital plus net property, right-of-use assets, goodwill and intangibles) — ROIC rose from about 19% in 2019 to roughly 22–23% in recent years, settling near 22.4% in 2025.

Stripping out goodwill and intangibles, the return on tangible operating capital is in the triple digits — the natural consequence of a goodwill-heavy serial acquirer.

ROIC has held up while the business has grown from $2 billion of revenue to $3.8 billion, which is the harder feat: many acquisitive businesses see returns drift down as the average deal becomes less differentiated. Rollins has avoided that, partly because it has remained disciplined on deal pricing and partly because the underlying single-route economics remain attractive.

View — A consistent 20%+ ROIC over a decade of compounding revenue is the single hardest-to-fake feature of the financial profile, and it is what justifies the multiple in the first place.

VI. Valuation

Rollins is a textbook example of a high-quality business carrying a high-quality price tag.

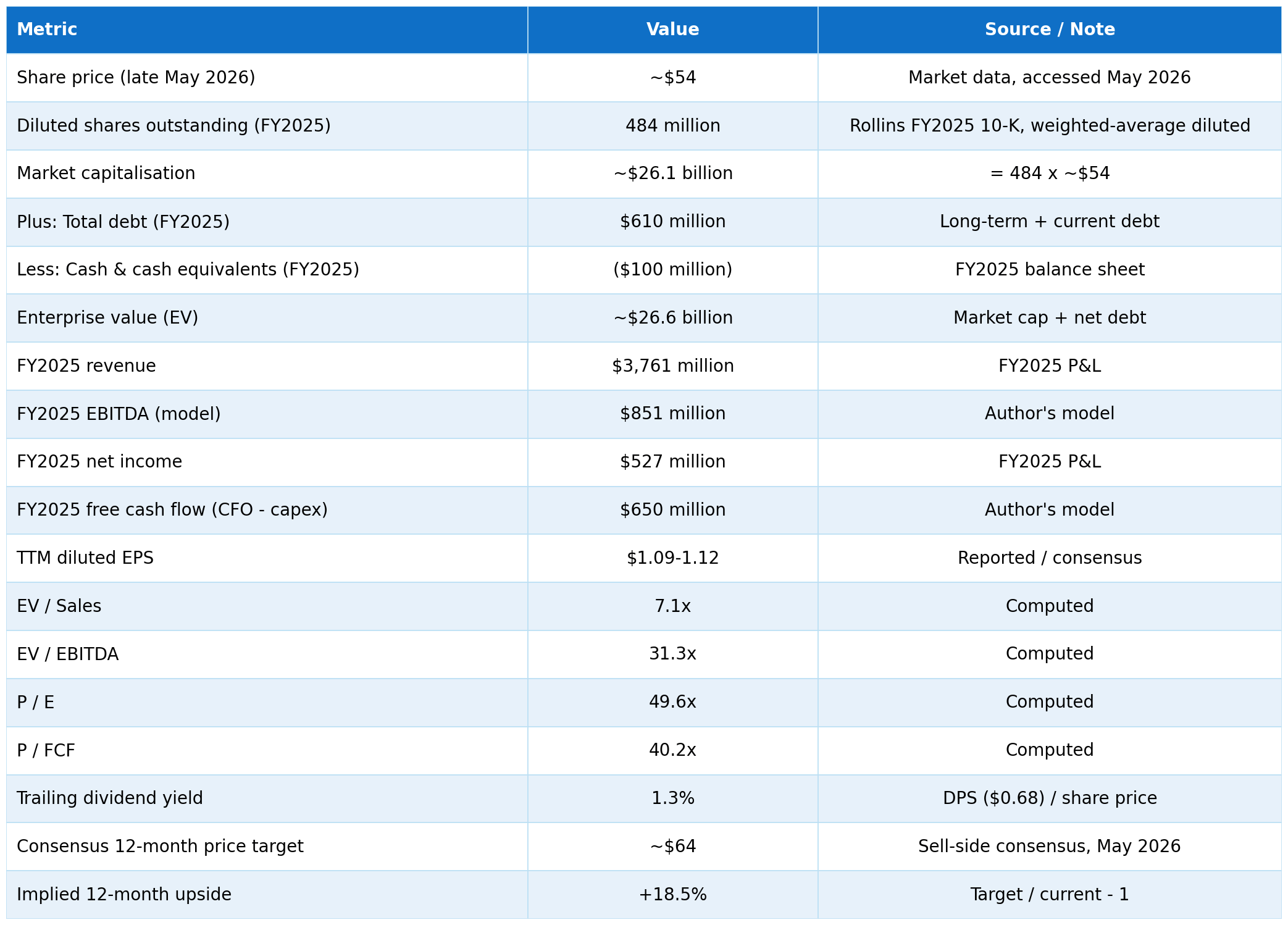

As of late May 2026, the shares traded around the low-$50s. The table below sets out the resulting market capitalisation, enterprise value and implied multiples on trailing 2025 results.

Multiples in context.

These are premium multiples by almost any yardstick. They sit well above the broad market and far above the listed peer: Rentokil Initial has for some time traded at EV/sales and EV/EBITDA multiples roughly half of Rollins’, reflecting Rollins’ higher margins, cleaner focus and more consistent organic growth, as well as Rentokil’s post-Terminix integration challenges.

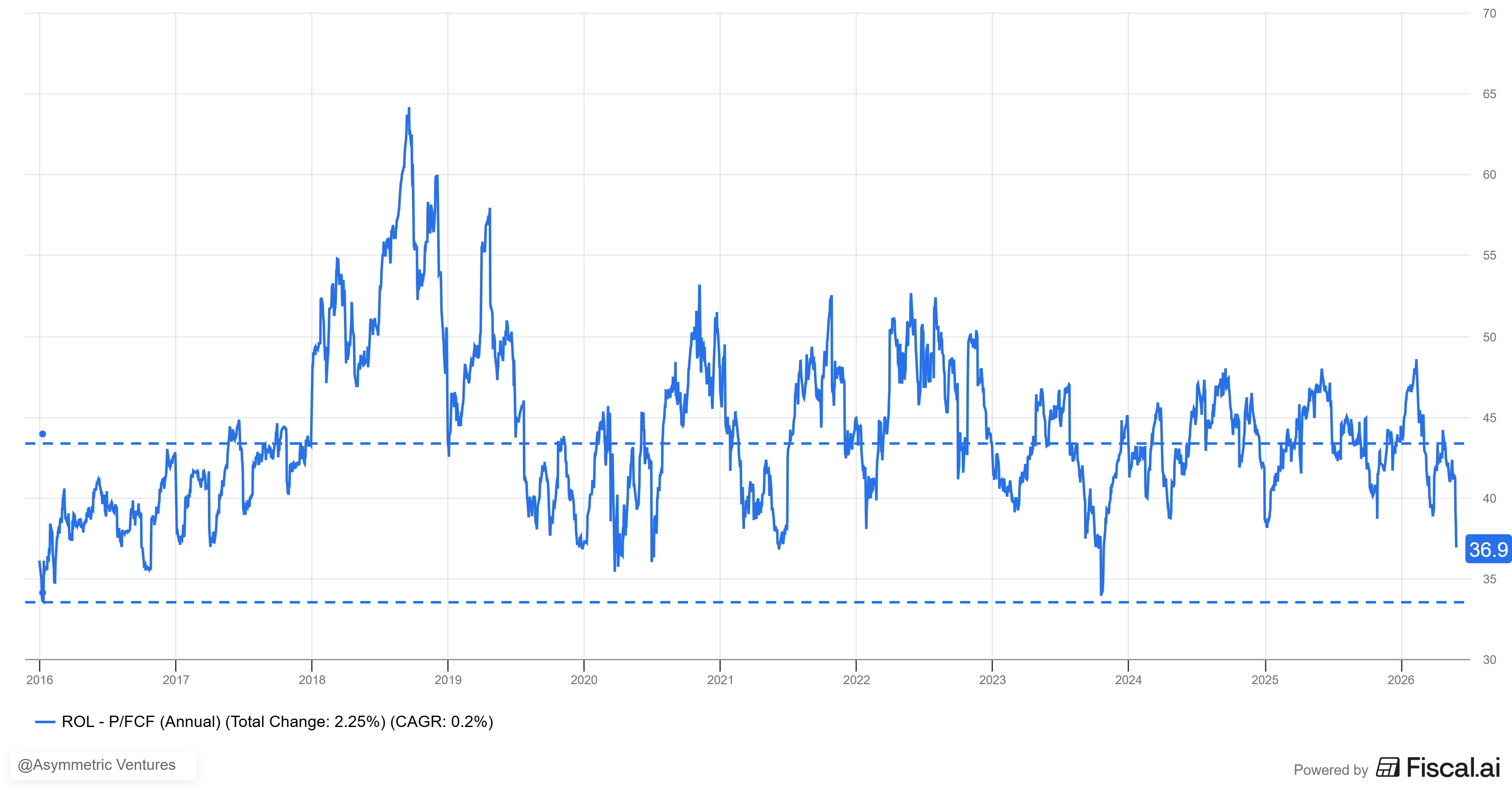

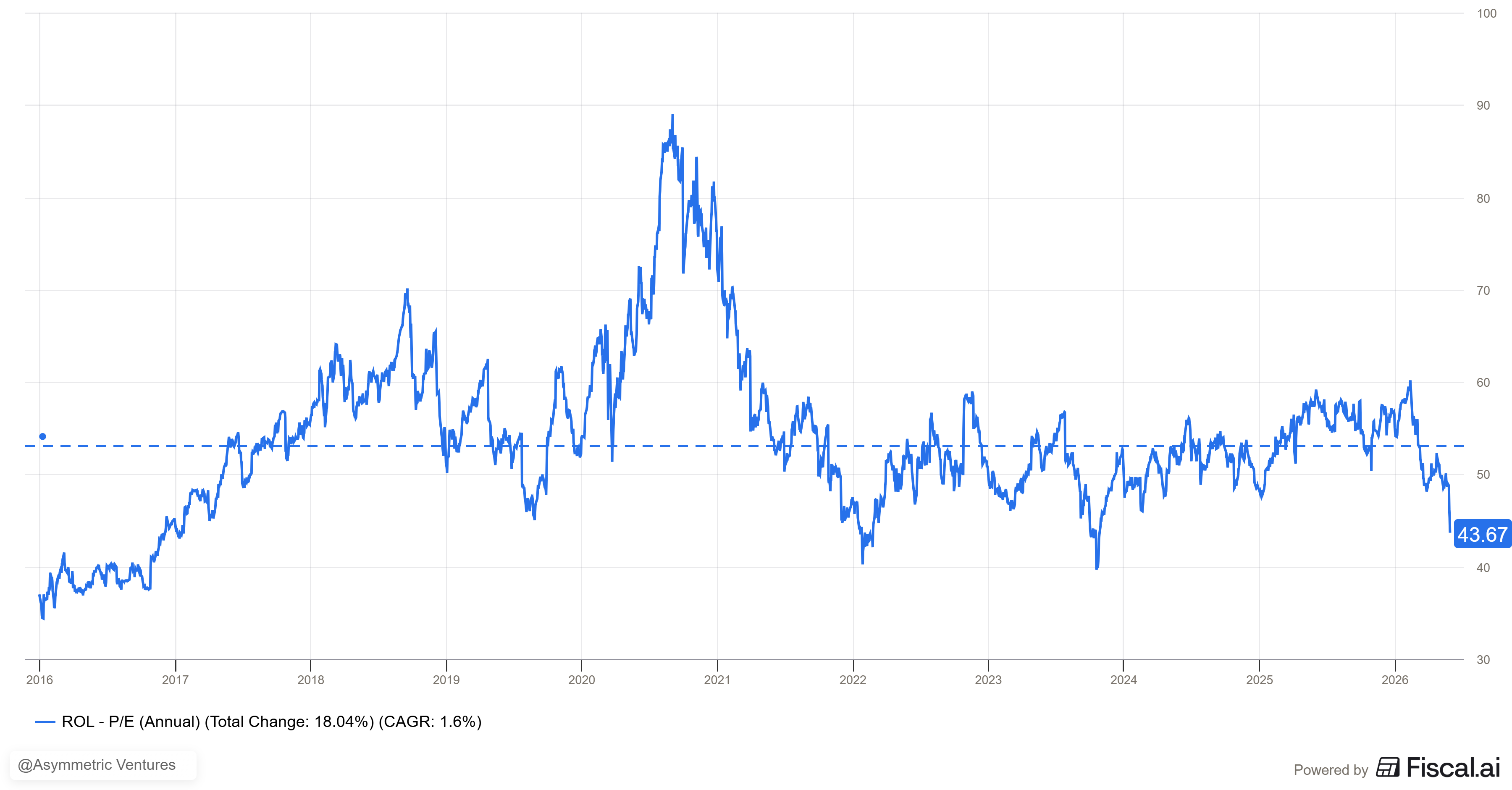

On a historical basis, Rollins’ own EV/EBITDA has ranged from the high-teens to the high-40s over the past decade, with a median around the low-30s — so the current multiple is near, not above, its own long-run norm even after the 2025–26 de-rating.

The share price tells its own story. Rollins de-rated through 2025 and into 2026: a weather-affected fourth quarter of 2025 (revenue and EPS just below expectations) triggered a sharp one-day fall, and the stock spent early 2026 in the low-to-mid-$50s, near the bottom of its 52-week range, even as the business kept compounding (Q1 2026 revenue grew about 10% with organic growth in the mid-single digits). Sell-side price targets cluster in the mid-$60s with a generally constructive but not uniform rating mix.

View — Valuation is the crux of the entire Rollins case. The business comfortably clears almost every quality test - I would say is one of the best businessess I’ve analyzed; what it does not obviously clear is price.

At ~40+ times FCF the stock is priced for many more years of the same disciplined compounding, which the track record supports but does not guarantee. An investor’s answer to Rollins is therefore mostly an answer to one question: how large a premium is a genuinely durable compounder worth? Nothing here resolves that question — it is a judgement about price, and reasonable investors will differ.

Sources: Market-data and valuation providers (stockanalysis.com, GuruFocus, Robinhood), accessed May 2026; published sell-side price targets; Rentokil Initial disclosures; author’s model; Rollins results releases.

VII. The Asymmetric Ventures Test

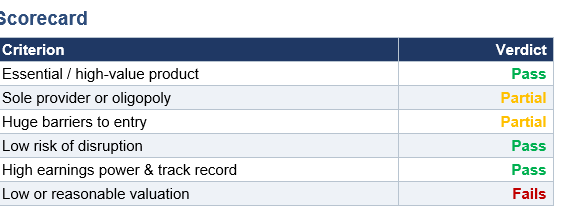

Up to this point the study has been neutral and explanatory. This final section is explicitly evaluative: it applies the firm’s six-criterion Asymmetric Ventures framework, grades each criterion PASS / PARTIAL / FAIL, and concludes with an overall verdict. The grading is the author’s judgement; the supporting facts remain footnoted to primary sources.

Criterion-by-criterion assessment

(a) Essential or high-value product — PASS.

Pest control is close to non-discretionary, especially on the commercial side. For food processors, restaurants, hospitals, hotels and logistics operators, pest management is a regulatory and reputational necessity, not a luxury; failure carries shutdown and liability risk. For households the cost is modest and the value (protection of the home, peace of mind) is high relative to price. The work is recurring and out of sight when it works, which is precisely why customers keep paying.

This is a clean pass: the service is essential where it is commercial and high-value where it is residential.

(b) Sole provider or part of an oligopoly — PARTIAL.

This is the criterion Rollins fits least neatly. The pest-control market is highly fragmented — thousands of small local operators in the U.S. alone — with only a handful of scaled players on top: Rollins, Rentokil (which absorbed Terminix in 2022), Ecolab in commercial, and the private consolidator Anticimex. So there is an oligopoly, but only at the top of a fragmented base, and Rollins is one of two leaders rather than half of a true duopoly.

Partial pass: it is a leading position within a consolidating market, not a structural duopoly like Visa/Mastercard or Moody’s/S&P. The important thing to factor is the ability of the company to keep growing through accretive M&A transactions, which are providing high value creation to the shareholders.

(c) Huge barriers to entry — PARTIAL.

Entering pest control at the small end is easy — a van, a sprayer and a licence. The barriers that matter are at scale: national brand (Orkin’s recognition is hard to replicate), route density (locked in by years of acquired share), the BOSS technology platform, and the trained-technician workforce. None of these is impossible to replicate; together they are very hard to replicate at national scale within a useful timeframe. The 2025 FTC non-compete order modestly weakens the technician-mobility component.

Partial pass: high barriers at the top of the market, low barriers at the bottom. On the other hand, today everybody seems to be focused on technology, rather than boring businesses like this one.

(d) Low risk of disruption — PASS.

Pest control is one of the lowest-disruption-risk services one can find. The work has to be done physically, on-site, by a person who can find and treat the actual infestation; there is no plausible software substitute. New baiting and monitoring technologies (digital traps, IoT sensors) are tools for pest-control operators, not substitutes for them. Pest behaviour and biology change slowly. A 10-year forward view of the industry looks much like the current one, only larger.

Clean pass: this is a low-tech, slow-moving, route-based service category, which is exactly what the framework rewards.

(e) High earnings power and demonstrated track record — PASS.

The pricing power is real: Rollins has taken low-to-mid-single-digit price increases consistently with minimal churn, and adjusted EBITDA margins have widened from ~20% in 2016 to ~23% in 2025. The track record is the most impressive part: ten years of mid-teens earnings compounding, free cash flow consistently above reported net income, and ROIC settling around 22%. Twenty-four consecutive years of revenue growth, per the Company.

Clean pass: earnings power demonstrated through a multi-year price-up cycle and through both economic expansions and the COVID disruption.

(f) Acquired at a low or reasonable valuation. As of late May 2026 Rollins traded in the low-$50s for a market capitalisation in the mid-$20-billion range — roughly 48–50x trailing earnings, about 31–32x EV/EBITDA, and the low-40s on free cash flow.

That is a large premium to the market and roughly double the multiple of its listed peer Rentokil. Even after de-rating through 2025–26, the multiple sits near the middle of Rollins’ own historical range rather than at a trough.

A company like this deserves a premium, but 40+ times FCF leads to no margin of safety at all if growth for whatever the reason starts to slowdown.