Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

Dear reader,

This will be the last deep dive on Uber’s investment thesis. Today we focus on valuation.

To value Uber, we first need to add some context.

Uber is by far the largest mobility platform on earth.

It might not be number 1 in all the markets where they operate, but on aggregate, there is no company with similar size.

This obviously should command a premium vs. peers when discussing valuation. But… It might not be the case.

Uber is sometimes cheaper than competitors, despite having a superior market positioning.

Current valuation is not in the “value” territory, but offers some margin of safety, which for a company like this, it’s not common.

Investors need to have their own views on the risk of disruption by AVs in order to consider if current valuation is attractive or not.

Uber vs. Peers

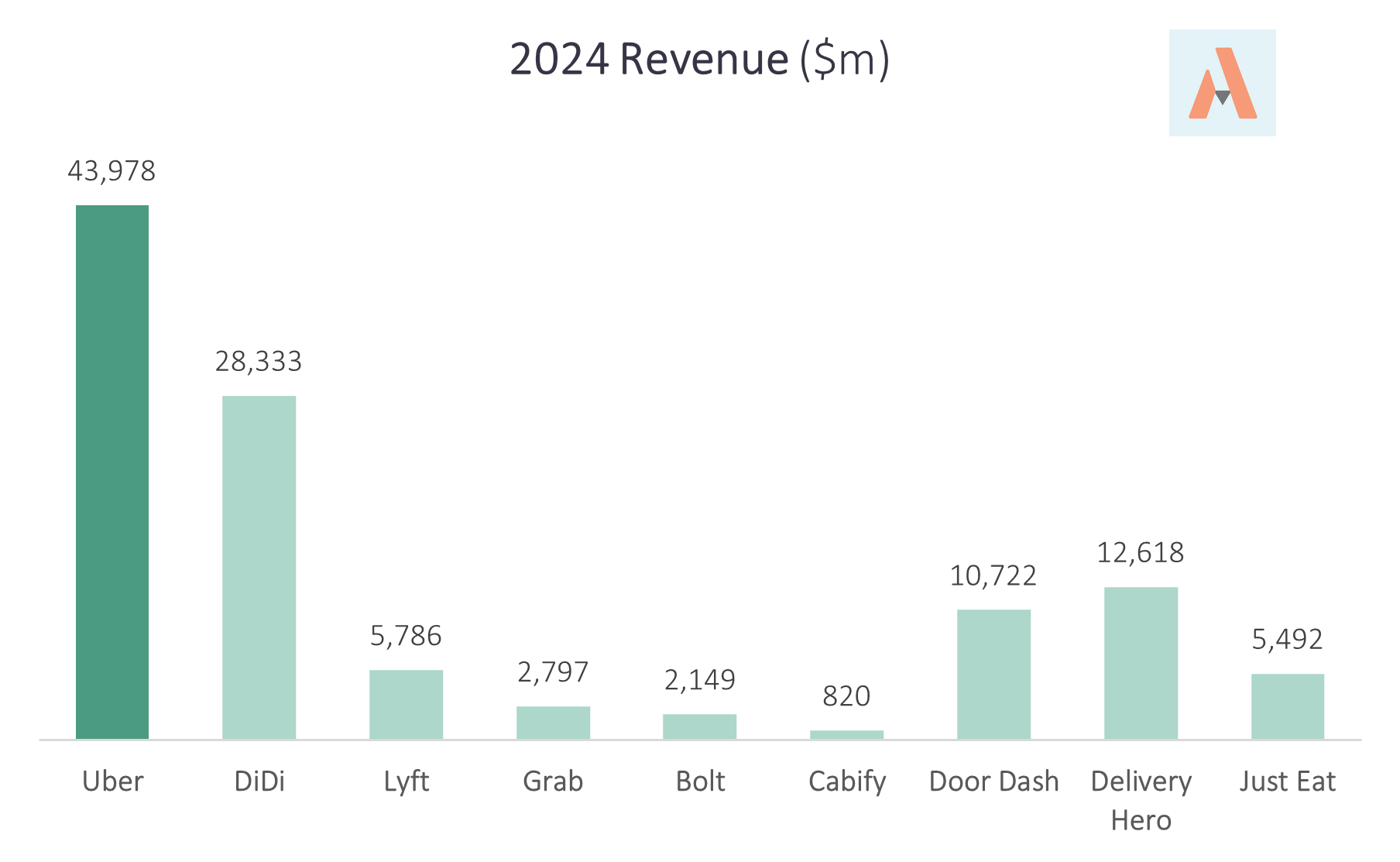

Uber is larger than the sum of DiDi and Delivery Hero, the largest competitors in the mobility and delivery space.

This matters because when the focus in on the risk from AVs, many people underestimate the power of the platform and the benefits from diversification.

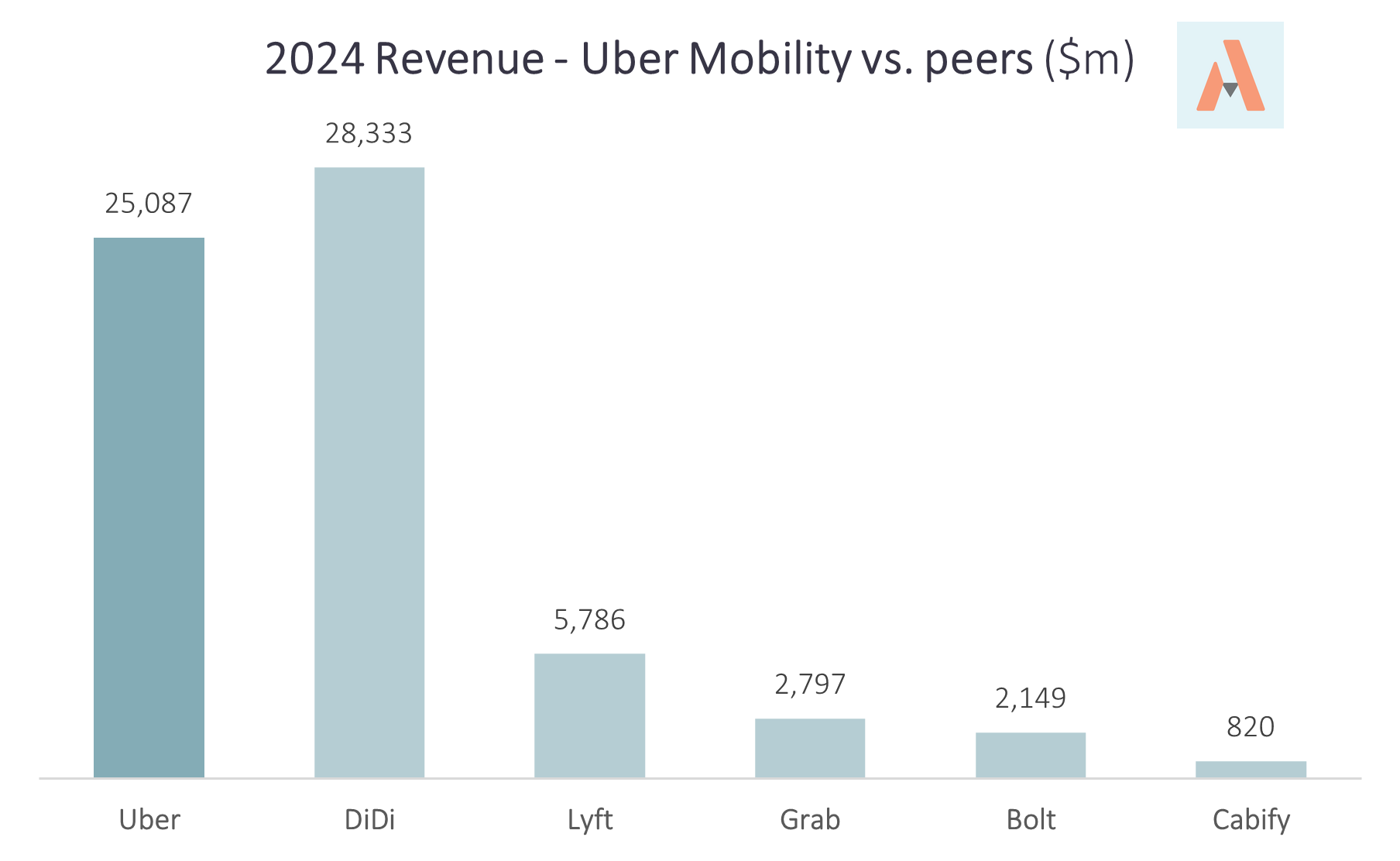

In mobility, only Didi is larger than Uber, as the company is the leader in China. Exclude Didi, and no company comes close to Uber.

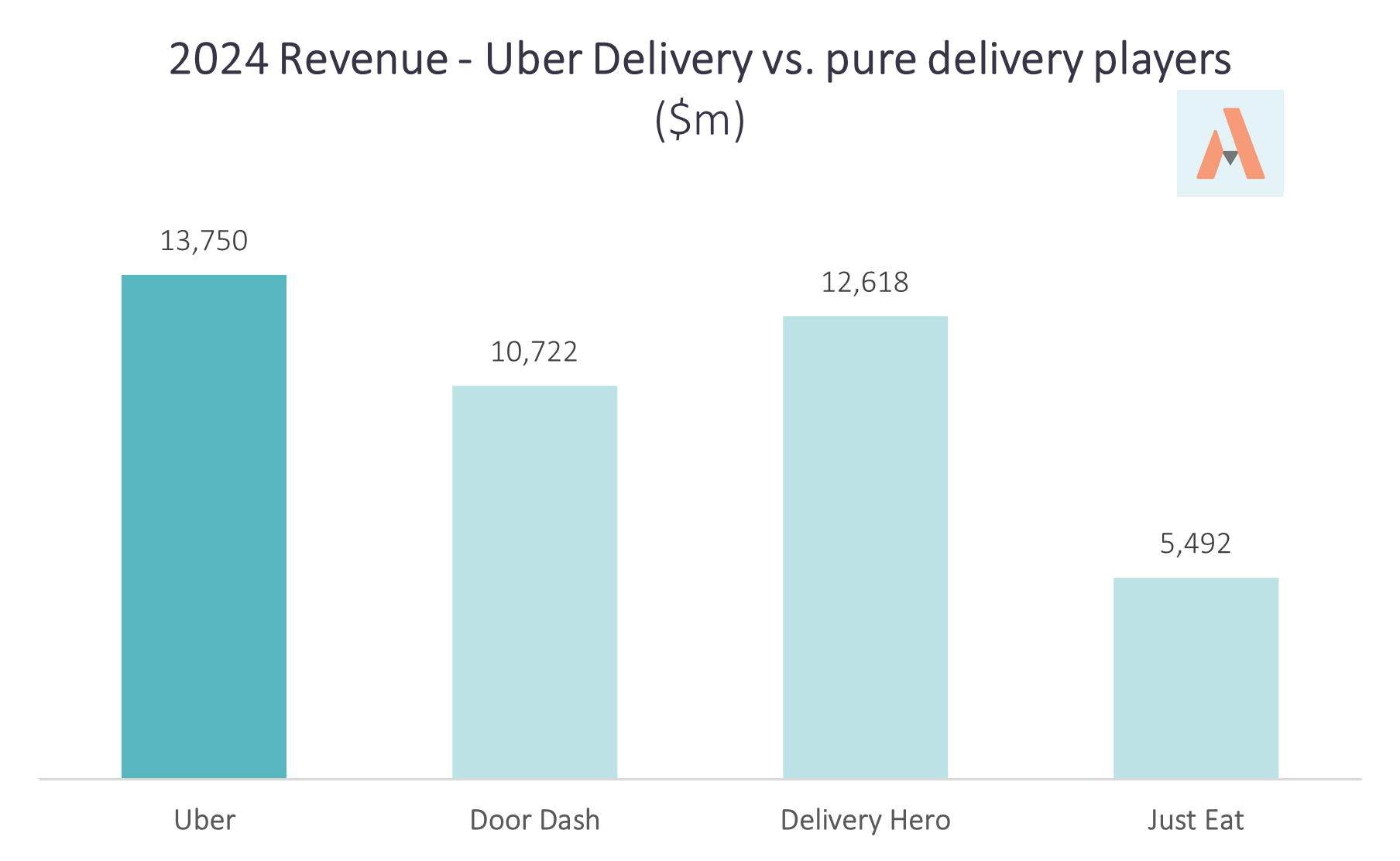

In the delivery segment, Uber seems to be less ahead than competition.

Door Dash is the #1 player in the US, and significantly ahead of Uber.

Delivery Hero is the largest pure delivery competitor around the world, with focus on emerging countries.

Uber is expanding its TAM across all geographies and becoming a last-mile logistic platform in the major cities.

As seen in these charts, Uber has a dominant position in Western economies.

A position that can continue to consolidate as all other companies are significantly below in terms of returns.

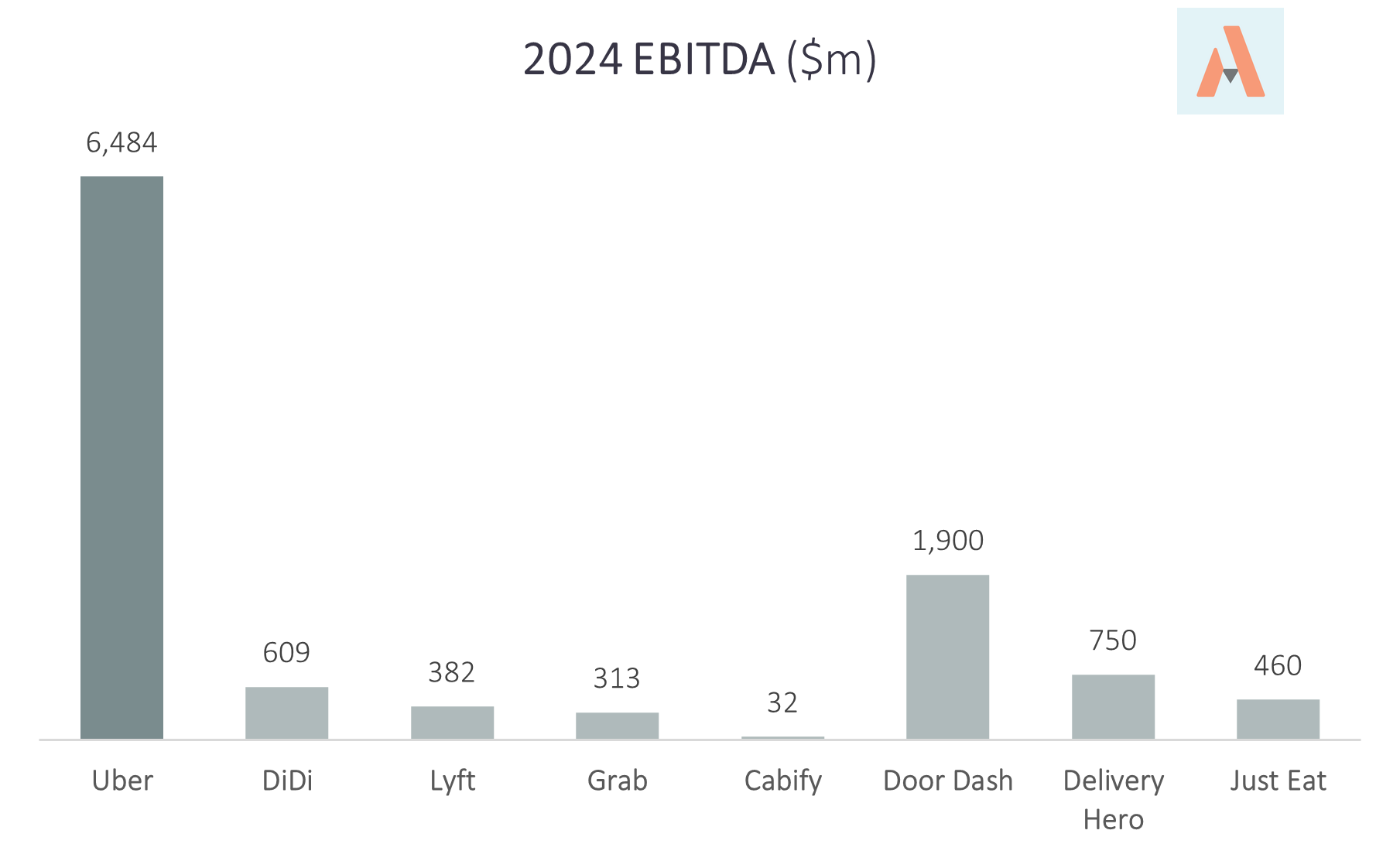

Uber generates 3x more EBITDA than Door Dash, the second largest player in the mobility industry by EBITDA.

Only Door Dash posts a higher 2024 Adjusted EBITDA margin of 17.7%, compared to 14.7% of Uber (in 2025 it’s closer to 17%). Adjust for SBC, and the gap is significantly reduced.

The rest of the players post low-single-digit EBITDA margins, except Grab with 11%.

As a conclusion, in terms of size, Uber stands clearly above all companies. It might not be the largest player in all geographies where they operate, but it’s the largest platform in Western economies.

This is very important because it generates a moat over the company. What matters in this business is having a reliable source of permanent customers.

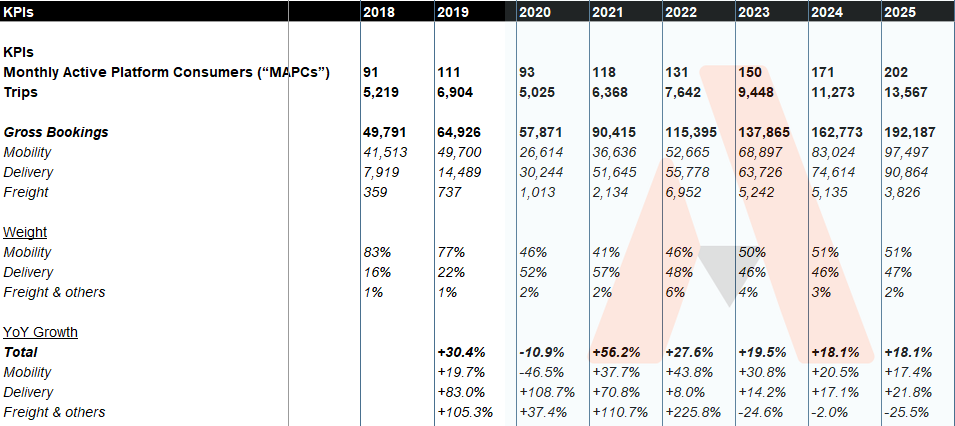

Uber reached 200m in the 4Q 2025, and there is still room for further growth.

Summary of Uber Financials

P&L

Uber is considered a mature platform given they are already present in every major city.

Despite this consideration, Uber is a growth company that is generating strong KPIs, and more importantly, it’s a very profitable company.

Company surpassed the 200m active customers in the latest results.

Gross bookings kept growing in the high teens (2025 gross bookings great at +18.1%)