In the prior post about Rollins we concluded that it was quite expensive at 40x FCF despite being one of the best best and most defensive businesses out there.

We did find out that there was another similar company called Rentokil, which apparently trades at lower multiples.

I decided to take a look at it.

Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

I. Executive Summary

Rentokil Initial plc is a UK-headquartered global services group that, since the October 2022 acquisition of Terminix, is the world’s largest pest-control company by revenue.

The business has two reporting categories:

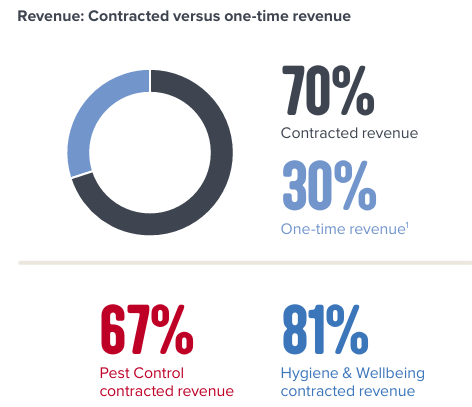

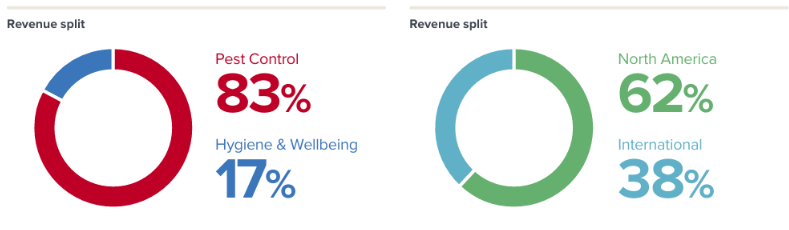

Pest Control (commercial, residential and termite — ~83% of 2025 revenue)

Hygiene & Wellbeing (washroom, dental waste, specialist hygiene — ~17%).

It operates in approximately 90 countries with around 60,000 employees

The financial pattern over the last decade has two distinct chapters.

From 2012 to 2024 Rentokil was a steadily compounding mid-cap services business, growing revenue from £2.2bnn to £5.4bn (≈8% CAGR) with an Adjusted EBITDA margin in the mid teens and some level of leverage.

In October 2022 the Company acquired Terminix for ~$6.7bn, issuing ~290m new shares and assuming substantial debt. Revenue stepped to £5.4bn in 2023 and ~$6.9bn in 2025 (company changed their functional currency to USD).

The post-deal period has been more uneven: organic growth in North America slowed to low single digits, integration costs and a U.S. termite-damage litigation provision pulled reported earnings below their pre-deal trajectory, and leverage peaked before de-leveraging back to 2.6x at the end of 2025.

The industry is large, growing and structurally fragmented.

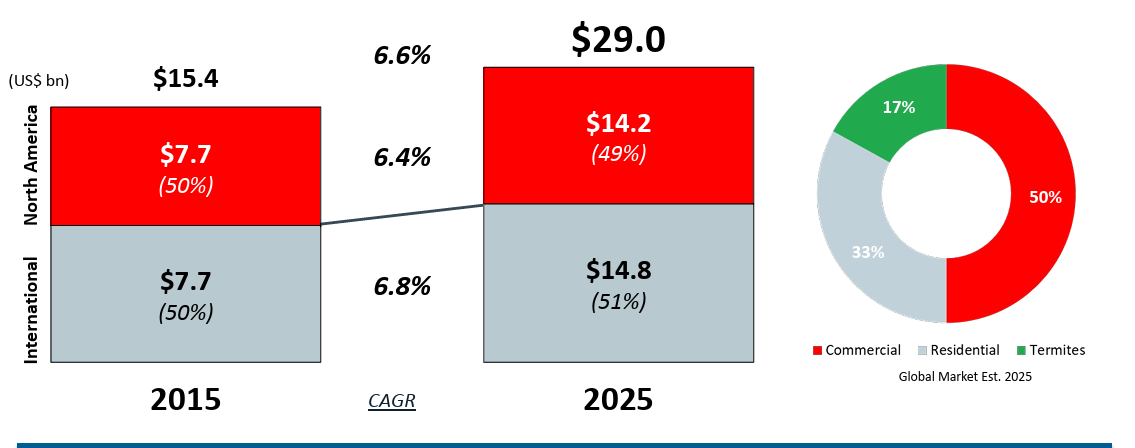

The global pest-control market is sized at roughly $25-27bn and is forecast to grow at 5-8% per year through the next decade, driven by urbanization, climate-driven pest migration, regulatory tightening and growth of integrated pest management.

The top six providers — Rollins, Terminix (now Rentokil), Rentokil, Ecolab, Anticimex and Aptive — collectively hold ~45% of the market. The remainder is fragmented across thousands of regional operators.

On the Asymmetric Ventures framework, Rentokil reads as 3 PASS / 3 PARTIAL — a different pattern from Rollins.

Essential product and low disruption risk: clear PASS.

Oligopoly structure and barriers to entry: PARTIAL — Rentokil enjoys global scale advantages but, especially in North America, faces intensive route-density competition from Rollins.

High earnings power & track record: PARTIAL — pre-Terminix ROIC of ~12-16% has stepped down to ~4-5% on the larger, goodwill-heavy capital base, with recovery dependent on integration delivery.

Reasonable valuation: PASS — at roughly 10x EV/EBITDA and 23x FCF, Rentokil trades at less than a third of Rollins’ EBITDA multiple, reflecting a discount that based on the past trajectory might be justified.

II. Introduction

What the company does, where it is located, and the industry it operates in

Rentokil Initial plc is a global business-services group, dual-listed on the London Stock Exchange and the New York Stock Exchange via American Depositary Receipts.

Its head office is at Compass House, Manor Royal, Crawley, West Sussex, in the United Kingdom; the operating headquarters of the largest business, North American Pest Control, are in Memphis, Tennessee — Terminix’s former home. The Company operates in roughly 90 countries through approximately 60,000 employees.

After the disposals of its France Workwear business in September 2025 and various other smaller non-core assets, Rentokil now operates in two reporting categories: Pest Control and Hygiene & Wellbeing. Pest Control accounts for ~83% of FY2025 revenue; Hygiene & Wellbeing for the remainder.

View — By revenue, Rentokil is now overwhelmingly a pest-control company with a complementary hygiene tail. The character of its earnings is closer to its U.S. listed peer Rollins than the conglomerate that traded under the same ticker a decade ago, making the company potentially more interesting than it was before.

Company history

Rentokil’s pest-control origin dates to 1925 when Harold Maxwell-Lefroy, Professor of Entomology at Imperial College London, developed a woodworm-treatment fluid commissioned to tackle a deathwatch-beetle infestation in Westminster Hall.

After his accidental death later that year, his assistant Bessie Eades acquired the formula and incorporated Rentokil Ltd. A parallel rodent-control business, British Ratin Co. Ltd., was founded in 1927 using a bacterial poison developed by Danish pharmacist Georg Neumann. British Ratin acquired Rentokil in 1957 and adopted the Rentokil name in 1962.

Through the 1970s and 1980s Rentokil expanded into hygiene services and acquired hundreds of small businesses under Sir Clive Thompson. In 1996 it merged with the FTSE 100 business-services group BET (which owned the Initial linen-rental business), forming Rentokil Initial plc. The 2000s saw a long period of restructuring as the Company narrowed its portfolio away from facilities services and back toward pest control and hygiene. The disposal of the CWS-boco workwear joint venture in 2017 was a notable inflection — it generated a one-time gain large enough to distort that year’s reported operating profit and net income.

Andy Ransom became CEO in October 2013 and led the strategic refocus, culminating in the October 2022 acquisition of Terminix Global Holdings — at roughly $6.7bn one of the largest UK-led cross-border deals of that year. Terminix was the second-largest U.S. pest-control operator behind Rollins, with around 2.9 million customers and a national branch network. Rentokil financed the deal with $2.4bn of new bond debt and ~290m new ordinary shares issued to Terminix shareholders, who emerged with ~26% of the combined entity. From January 2025 Rentokil changed its presentation currency from sterling to U.S. dollars, reflecting the fact that the U.S. is now the source of more than half of group revenue and roughly 60% of profit.

In January 2026 the Company announced that Andy Ransom would retire from the CEO role following the 2026 Annual General Meeting (7 May) and be succeeded by Mike Duffy, a U.S. citizen and career operator most recently CEO of OnTrac, the logistics business. Duffy joined Rentokil on 16 February 2026 as CEO Designate and assumed full executive responsibility on 16 March 2026.

View — Rentokil’s century-long history is one of acquisition-led growth interrupted by periodic strategic refocus. The Terminix deal is the largest single bet in that sequence, and the second half of the 2020s will be judged in large part on whether it pays off.

III. Business model

What the company does

The core business is identifying, treating and preventing pests to protect the safety and hygiene of our customers’ premises.

Rentokil sells recurring service contracts that send trained technicians to commercial and residential premises to prevent and remediate infestations, manage washroom hygiene, and provide related specialist hygiene services. Pricing is per visit or per period; visits typically occur monthly or quarterly for commercial accounts and on an as-needed or contract basis for residential customers.

Both Pest Control and Hygiene & Wellbeing are largely subscription-based businesses, where customers pay for regular inspections, treatments or servicing over a defined contract period. This enables steady, predictable revenue streams, and a low level of exposure to economic cycles.

70% is contracted revenue — Company has a high degree of stable revenue providing stable and predictable cash flows. In pest control, most clients are on annual or multi-annual contracts

30% of the revenue is a one-off (per-job or per-incident basis), which is dependent on clients requesting their services for specific tasks

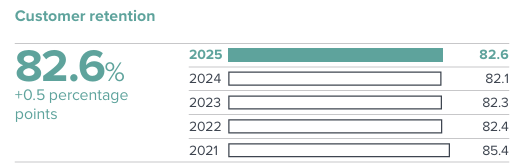

Customer retention is high — pest-control churn rates are routinely in the 80-90%+ range across the industry — and pricing power is supported by the small share of customer spend that the service represents.

Segments and revenue mix

Pest Control: by far the largest line.

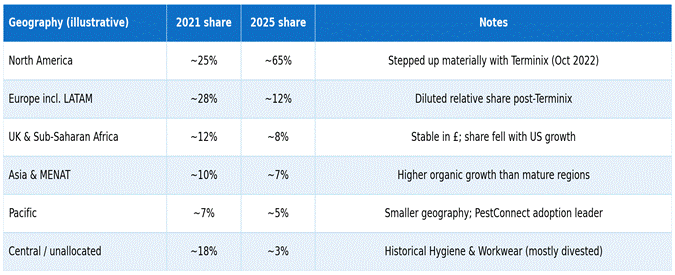

Pest Control — North America (now ~65% of group revenue): commercial, residential and termite pest control delivered through the integrated Rentokil-Terminix branch network. This business is the global market leader by revenue and is the main driver of group growth and integration challenges.

Pest Control — International (~17% of group revenue): operations across Europe (including Latin America), the UK, Sub-Saharan Africa, Asia, MENAT and the Pacific. International posted 3.7% organic revenue growth in 2025 — the fastest-growing part of the Group on a like-for-like basis — supported by both pricing and volume.

Hygiene & Wellbeing: the complementary services tail.

Hygiene & Wellbeing (~17% of group revenue, $1,205m in 2025): washroom-hygiene services, specialist hygiene (e.g. healthcare, food service), and Dental Waste Disposal. Revenue grew 4.3% in 2025 (2.3% organic), with margin similar to International Pest Control.

The compositional shift is dramatic. Pest Control North America was $440m in 2016, sat at $800m in 2021, then quadrupled to $4.25bn in 2023 once Terminix was fully consolidated. The Hygiene & Other category fell as a share of total because the denominator grew, and because of selective disposals; the absolute revenue contribution of Hygiene & Wellbeing alone has actually risen.

Geographic mix shifted accordingly. The illustrative split below sketches the structural change.

Main customers and contract economics

Rentokil serves a mix of commercial and residential customers:

Commercial accounts dominate by revenue: food processors, restaurants, hotels, hospitals, logistics operators, retailers, schools and offices. Commercial pest control is increasingly a regulatory and reputational necessity rather than a discretionary spend — food-safety authorities require evidence of integrated pest-management programes, and a single rodent sighting can close a food-service location.

Residential customers, while smaller per account, are higher-margin and more loyal on a multi-year basis.

Service contracts are typically annual with multi-year renewal patterns. Rentokil’s industry-standard retention rate is in the 80-90% range; for the Terminix residential book in North America the integration period has seen retention pressure that the Company has been working to recover through the “RIGHT WAY 2” growth plan launched in 2024.

View — The economics of pest control are unusually stable for a services business. Recurring contracts, small per-customer ticket sizes (a few hundred dollars per year for residential, a few thousand for commercial) and high retention combine to produce free-cash-flow streams that are remarkably defensive across the cycle.

Last, I think it’s important to analyze how today’s society can’t live with insects or small animals near them. We are more and more becoming less connected with nature — and don’t get me wrong, I don’t want to have rats at home, but we are less tolerant with rodents, insects, etc. These are good news for these companies are there services become even more important. The covid pandemic has probably accelerated this trend.

IV. Industry overview

Market size and how the industry is evolving

Independent market-research providers size the global pest-control services market at roughly USD 25-27 billion in 2024-25, with forecast compound annual growth rates of 5-8% over the next decade, implying a market that roughly doubles by the mid-2030s. The variance across providers reflects different scope definitions (some include pest-control products and adjacent hygiene services; others limit the count to commercial and residential service revenue only).

Three structural drivers underpin growth.

Urbanization and food density. As populations concentrate in cities and food production scales, the breeding environments for pests multiply. Rentokil has cited demographic urbanization as a primary long-cycle growth driver in its annual report.

Climate-driven pest migration. Warmer winters and shifting climatic zones are extending the geographic range of vector species (mosquitoes, ticks, termites). The WHO recorded 14.6 million dengue cases globally in 2024 — a record — and rising tropical-disease incidence creates a public-health imperative for pest control beyond the traditional commercial use case.

Regulatory tightening and integrated pest management. Food-safety, healthcare and hospitality regulators increasingly require documented integrated pest-management (IPM) programes. Chemical bans push the industry toward higher-skill, higher-priced biological and technological alternatives — favorable to scale operators like Rentokil that can invest in R&D and digital tools.

There is scientific evidence that urbanization and climate change is driving the growth of rat populations in large cities.

Science Advances: Increasing rat numbers in cities are linked to climate warming, urbanization, and human population

PMP: Study shows rat populations are on the rise thanks to warming temperatures, city growth

On the demand side, the residential segment is becoming more digital: inbound leads from search and price-comparison platforms now dominate new-customer acquisition. Rentokil’s 2024 commentary highlighted the rebound in inbound digital lead flow as a key signal of North America’s growth recovery.

Competitors: a partial oligopoly at the top of a long fragmented tail

Industry concentration is meaningful at the top but limited overall. The six largest players — Rollins, Terminix (now part of Rentokil), Rentokil itself, Ecolab Pest Elimination, Anticimex, and Aptive Environmental — collectively hold approximately 45% of the global market. The remaining 55% is split across thousands of regional and local operators ranging from $1-100m in revenue.

The structure of the top tier is distinct from a true oligopoly because the major players have very different geographic footprints and ownership structures.

Rollins, Inc. (NYSE: ROL): the U.S. pure-play pest-control compounder. Owns Orkin and a portfolio of brands; ~$3.8bn revenue in 2025; over 30% family ownership through the Rollins family; trades at a premium valuation (~31x EBITDA) reflecting consistent execution and a fortress balance sheet. The most direct listed competitor to Rentokil in North America. We reviewed this company during the last week:

Anticimex (Sweden): private, owned by EQT (since 2012). Highly acquisitive across Europe, North America, Asia Pacific and Latin America. Has been the industry’s digital-services pioneer, claiming 500,000 IoT-enabled SMART devices installed globally by early 2025. The natural acquisition target or merger partner for either Rentokil or Rollins, though private-equity ownership makes timing unpredictable.

Ecolab Pest Elimination (NYSE: ECL division): a division of Ecolab Inc., the global cleaning, sanitation and water-treatment major. Focuses on commercial/industrial pest control bundled with broader sanitation contracts. Distinct go-to-market — sold as part of a wider hygiene programe — limits direct overlap with residential focus, but competes hard in commercial.

Aptive Environmental (private): U.S. residential-focused, door-to-door sales model. Smaller than the top three but growing rapidly. Has been a source of customer churn for the larger players in U.S. residential.

Long tail of regional operators: Massey Services, Dodson, Arrow Exterminators in the U.S.; family-owned regional operators across Europe and Asia. Many of these are bolt-on acquisition candidates for the larger players — Rollins, Rentokil and Anticimex have each completed dozens of bolt-on deals annually.

Here lies a key factor to consider: Rentokil, Rollins and other players will keep consolidating the industry. Little by little, year by year, these companies are going to become more relevant and gain strong pricing power with the lack of competitors.

Competitive advantages

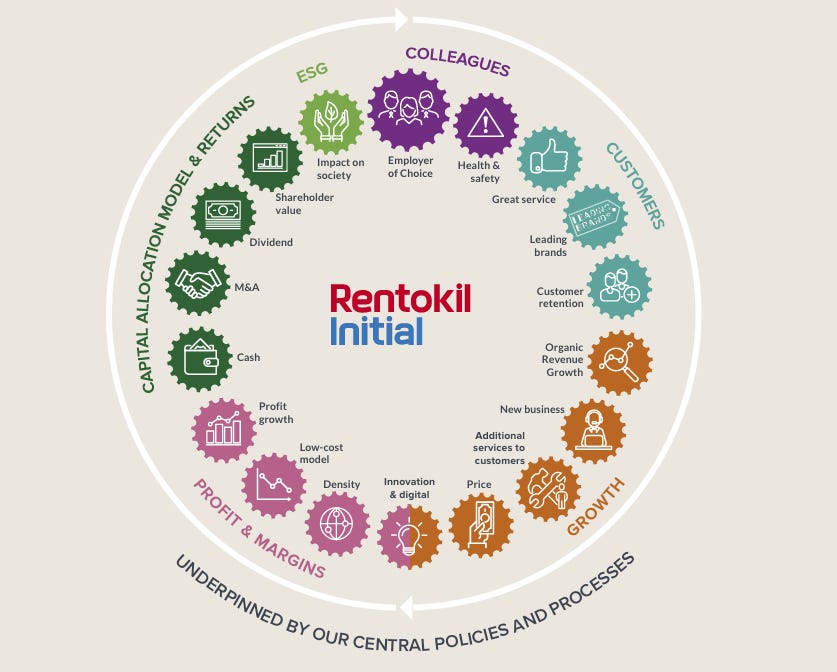

Rentokil divides its operating model into 6 drivers:

1- Colleagues. The company is delivering positive returns in this area, increasing the health & safety of customers and reducing employee churn. This increases efficiency of the operations.

2- Customers: The company retains at least 80% of their customers, a strong retention rate considering it’s a highly fragmented market and, despite the management talks a lot about the brand, I don’t think brand becomes as relevant as in other industries.

3- Growth: the company is investing in improving their services and is increasing the value of the contracts. Pricing is being increased slightly above inflation.

4- Profit & margin - Route density and cost control is key to keep healthy margins. With increased size the company can become much more efficient than local players.

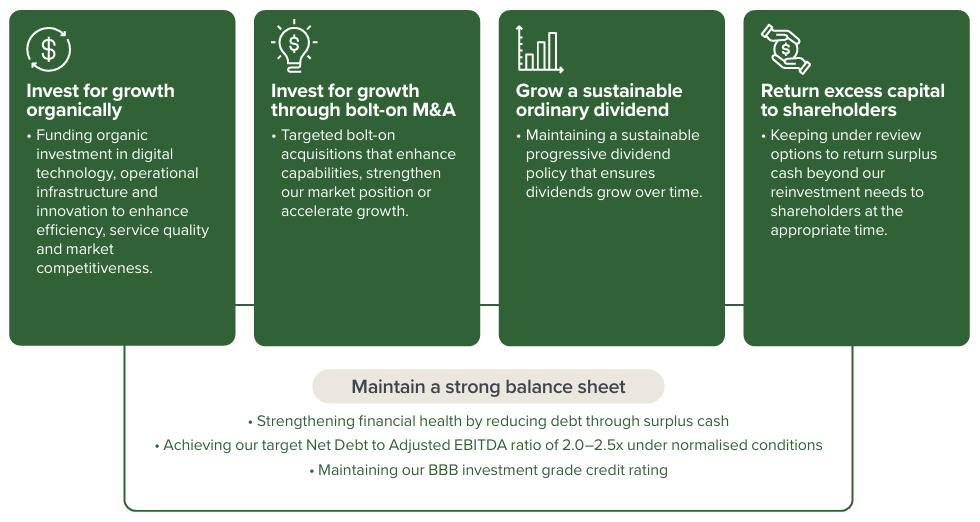

5- Capital allocation framework: divided in 4 buckets, cash, M&A, dividend and shareholder value. We will cover it later.

6- ESG.

In the following slide from 2025 results, we can see how the company is progressing and delivering in each of these 6 topics/initiatives:

Pest-control operators win or lose on three competitive advantages, all of which Rentokil possesses to differing degrees.

Route density. Service routes are densest where customer bases are most concentrated, and density drops drive-time per service stop dramatically. Rentokil’s combined Rentokil-Terminix North American footprint is the largest in the industry by branch count (~600 at deal close, targeted at ~400 optimized branches by 2026).

Brand and trust. In residential pest control, branded incumbents win because the service is intermittent, the consequences of poor service are high (re-infestation, property damage), and trial is socially expensive. Rentokil and Terminix are both globally recognized names; the integration into a single “Rentokil North America” legal entity in 2025 was a key step in consolidating that brand equity.

Digital and data platforms. Rentokil has invested significantly in its PestConnect IoT platform and myRentokil customer-management interface, and the integration of the Terminix PestPac and Wayport systems into a unified operational stack is targeted to complete in 2026-27. These platforms generate operating leverage and switching costs for commercial customers integrated into them.

Switching costs in commercial. Integrated commercial accounts (food production, healthcare, hospitality) embed Rentokil into their compliance documentation and IPM systems; the cost and risk of switching providers is materially higher than the cost of the service itself.

Density-based unit economics in established markets. In mature geographies the existing branch network creates a route-density advantage that compounds; a new entrant must subsidize the same coverage on a much smaller revenue base.

When reviewing the Annual Report of 2025, one thing that surprised me is how operations are gaining efficiencies every year in many fronts:

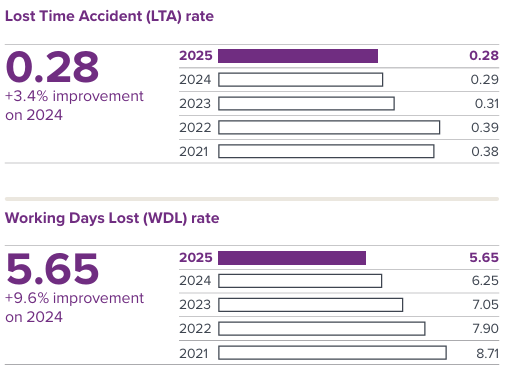

Investing in the employees to avoid accidents and avoid working days lost. The rate of working days lost has decreases from 8.7 in 2021 to 5.65 in 2025. Multiply this figure by thousands of people and the impact is meaningful.

Keeping customer retention high in the 80s

The company has the ability to raise prices with inflation every year as they provide a service that many people in today’s world see as extremelly necessary.

Is there a moat, and what could erode it?

There is not a clear moat in these companies, as barriers to entry are low. What creates the moat is the scale of these companies that can compete globally against any local competitor, and also have the financial strength to acquire competitors.

Barriers to entry are relatively low, as you need pest control products and a van. However, becoming efficiently to compete against these larger companies is another story.

Rentokil and Rollins are so big that we can’t think about potential new direct competitors, in an industry that nobody is watching. All eyes are on AI and technology.

Rentokil and Rollins are more efficient, have huge fire power and extended branding in their territories.

What can erode this moat?

It’s difficult to find reasons. Probably their biggest enemies are themselves. If they keep discipline and acquiring the right companies, these companies will be able to protect their moat.

V. The management

Key executives, backgrounds and reputation

Mike Duffy — Chief Executive Officer (from 16 March 2026).

U.S. citizen, based in North America. Joined Rentokil as CEO Designate on 16 February 2026 and succeeded Andy Ransom as CEO on 16 March 2026, ahead of the 7 May 2026 Annual General Meeting.

Career background: 25+ years of US business leadership across B2B and B2C services. Most recently CEO of OnTrac (a last-mile residential parcel delivery business owned by LaserShip, 2023-2025); CEO of FleetPride (largest US heavy-duty truck-parts distributor, 2021-2023); CEO of C&S Wholesale Grocers (one of the largest US grocery wholesalers, 2018-2020). Earlier senior roles at Cardinal Health and Gillette. Independent director of Republic Services (NYSE: RSG) since 2020.

This background is very interesting, because these companies operate similar to logistics companies. Route density is core to maximize revenue, and therefore, this profile makes total sense. Although he has no background in the industry, he will likely focus on operations and efficiencies.

Andy Ransom — outgoing CEO.

CEO from October 2013 to March 2026 (12.5 years), the architect of Rentokil’s strategic refocus on pest control and the Terminix acquisition. To remain with the Company in a transition capacity until the 2026 AGM. Lower personal shareholding than US peer CEOs (~0.09% of Rentokil) reflecting UK governance norms rather than lack of alignment.

Paul Edgecliffe-Johnson — Group Chief Financial Officer.

Joined as CFO in early 2025 after extended tenure as CFO of InterContinental Hotels Group (IHG). Successor to Stuart Ingall-Tombs, who departed in late 2024. Aaron Coley was previously North America CFO. The CFO transition coincides with Rentokil’s currency-presentation change and ongoing Terminix integration.

Richard Solomons — Board Chair.

Independent Chair. Former CEO of InterContinental Hotels Group (which shaped his prior working relationship with Paul Edgecliffe-Johnson). UK plc governance — majority-independent board, one-share-one-vote, no dual-class structure.

Ownership and skin in the game

Rentokil’s ownership is overwhelmingly institutional.

Approximately 88% of free float sits with institutional shareholders;

No single holder is controlling.

Insider ownership at the executive level is very modest: the outgoing CEO held ~0.09% of the Company. Mike Duffy’s joining package includes a minimum shareholding requirement of 400% of base salary, which over time should build a more meaningful executive stake.

The most strategically significant minority shareholder is Trian Fund Management (Nelson Peltz’s activist vehicle), which disclosed an initial stake in 2023 and built up to roughly 64.6 million ordinary shares (~2.6% of share capital). Trian secured a board seat in 2024 and has been an active voice on integration KPIs and capital-allocation priorities. The CEO-succession process and the choice of a US-based operator reflect that engagement.

View — Trian’s involvement and the choice of a US-based, integration-focused CEO together suggest the next chapter will emphasize operational delivery, cost-efficiency capture and — possibly — a re-listing or partial US listing. The latter is speculation, but the choice of a North-America-resident CEO is at the very least a strong directional signal.

Compensation and alignment of interests

The incoming CEO’s pay package illustrates how the Board has positioned alignment going forward.

Base salary of US$1,600,000 — substantial in absolute terms but, as a proportion of total potential pay, modest.

Annual bonus of up to 225% of base salary (i.e. up to $3.6m). Performance measures will be disclosed in the 2025 Directors’ Remuneration Report; in line with prior practice these typically reference Group revenue growth, Adjusted Operating Profit margin and Free Cash Flow conversion.

Long-Term Incentive Plan (LTIP) awards of up to 375% of base salary (up to $6m at grant date). Performance metrics historically include relative TSR, EPS growth and ROIC — putting capital efficiency at the heart of executive incentive design.

Replacement awards of US$3.98m in Rentokil shares to compensate for forfeited awards at OnTrac, vesting over time.

Shareholding requirement of 400% of base salary, with post-employment shareholding requirements that prevent immediate disposal after departure.

Andy Ransom’s outgoing pay was £1.91m total for FY2024 (51.5% salary, 48.5% variable, including share awards). This figure is materially below the median FTSE-100 CEO and well below his nearest listed peer (Rollins’ CEO Jerry Gahagan).

View — The compensation step-up for the incoming CEO is large, but explicit — and the 400% shareholding requirement and ROIC-weighted LTIP design align Duffy’s economics with the kind of capital-discipline outcomes that should matter most after the Terminix capital deployment.

Recent insider trading

There has been no material insider buying or selling by Rentokil executives in the period leading up to the CEO transition that would carry strong signaling value. Trian’s stake is unchanged at recent disclosure. The 2025 disposal of France Workwear was a corporate transaction rather than an insider trade and signals a sharper portfolio focus rather than executive sentiment.

Sources: Rentokil Initial press release 13 January 2026 (CEO succession); Rentokil 2024 Annual Report (Directors’ Remuneration Report); Simply Wall St management and ownership data; Investing.com institutional holdings; Trian Fund Management Schedule 13G disclosures; Bloomberg executive profiles.

Quick Review of the Strategy

2012 — Turnaround conglomerate; the last year before focus

CEO: Alan Brown | Chair: John McAdam.

Rentokil Initial was still a six-market conglomerate — pest control, hygiene, workwear, facilities services, plants and the City Link parcels business — and posted a statutory pre-tax loss of about £50.5m, driven largely by writedowns at City Link, even as revenue rose ~2.8% and adjusted operating profit improved ~5.1%.

The statement framed progress against the Operational Excellence Agenda launched in 2008 and signalled that the heavy restructuring was largely complete, freeing the group to pivot toward growth and innovation.

Acquired Western Exterminator (~$100m), expanding into the US West Coast and becoming the third-largest pest controller in America (part of ~£128m of acquired annualised revenue in the year).

Continued efforts to turn around the loss-making City Link parcels business (losses narrowed; volumes up ~17%).

Transitioned Initial Facilities toward Total Facilities Management while scaling back the Spanish operation to reduce exposure.

Early innovation that would later mature — PestConnect concept, bed-bug detection, heat treatment.

2013 — The pivotal year: City Link sold, Ransom takes over

CEO: Alan Brown until 1 October, then Andy Ransom | Chair: John McAdam.

This was the strategic hinge of the whole period. The disposal of the deeply loss-making City Link and the subsequent CEO succession reset the company’s direction.

Announced (April) the sale of City Link to private-equity firm Better Capital for a nominal sum, triggering a one-off disposal loss of ~£41.0m (mostly a non-cash writedown).

Andy Ransom appointed CEO from 1 October, succeeding Alan Brown after a succession process; Ransom immediately launched a full review of group strategy.

Agreed (announced February 2014) the sale of Initial Facilities to Interserve for £250m — together with City Link, refocusing the group on core categories: pest control, hygiene and workwear.

Balance-sheet actions: a renegotiated, lower pension-contribution schedule and a new €350m bond to refinance a maturing €500m bond, taking the average cost of debt below 4%.

Underlying trading only “steady” amid a weak Europe (Benelux); growth came mainly from M&A (Western Exterminator plus 19 pest-control bolt-ons).

2014 — Ransom’s first full year: the focused strategy is born

CEO: Andy Ransom | Chair: John McAdam.

The modern Rentokil strategy crystallised here, alongside completion of the Initial Facilities exit.

Introduced a new four-quadrant capital-allocation framework — Emerging, Growth, Protect & Enhance, and Manage-for-Value — to prioritise investment and M&A.

Set the company’s first-ever medium-term financial targets for revenue, profit and cash, plus a progressive dividend policy and a commitment to pay down debt.

Established “speed of execution” as a defining management principle.

Strong financial reset: net debt down £260m to £775m (lowest in 15 years), restructuring costs down ~£38m, free cash flow up ~£93m, and an S&P upgrade to BBB.

Launched PestConnect and made 30 acquisitions, the large majority in the Growth and Emerging quadrants. (Workwear was still core, ~23% of revenue.)

2015 — Building the North American platform

CEO: Andy Ransom | Chair: John McAdam.

The defining move was scaling North America.

• Acquired Steritech, a large US commercial pest-control and food-safety auditing business, transforming Rentokil’s North-American scale.

• Anchored the decision to make North America — roughly half the global pest-control market — the primary growth engine, via organic growth plus heavy bolt-on M&A.

• Embedded the RIGHT WAY plan: two core categories (Pest Control and Hygiene) across five regions on a low-cost, single-country operating model.

2016 — Reshaping the portfolio toward Pest Control & Hygiene

CEO: Andy Ransom | Chair: John McAdam. The pivotal decision was a portfolio pivot away from textiles/workwear.

• Announced (December) a joint venture with Franz Haniel (CWS-boco), folding Rentokil’s lower-growth Workwear and Hygiene operations in Benelux, Sweden and Central & Eastern Europe into Haniel’s business and retaining a ~17.8% stake.

• Continued dense bolt-on M&A; progress toward market leadership in India (the PCI tie-up).

• Delivered pest control for the Rio 2016 Olympics; engaged with the US CDC on Zika/mosquito control.

• Agreed a “next-generation pest control” digital partnership with Google and PA Consulting.

2017 — Completing the Haniel JV and the “big five” framework

CEO: Andy Ransom | Chair: John McAdam. The CEO statement moved to a “Q&A with Andy Ransom” format around this time.

• Completed the Haniel / CWS-boco JV (June), formally exiting much of the European workwear/hygiene business.

• Framed strategy around five challenges: organic growth in Pest Control, value through digital, building Hygiene, M&A execution, and Employer of Choice.

• Ongoing revenue grew 14.5% (10.7% from acquisitions) across 41 deals in 24 countries; Pest Control organic +5.8%.

• Formed Rentokil PCI, establishing clear No.1 status in India; identified vector/mosquito control as a major new growth line (VDCI).

2018 — Redeploying JV proceeds; France turnaround

CEO: Andy Ransom | Chair: John McAdam (his final report). With Pest Control and Hygiene now ~89% of operating profit, the strategy was to reinvest the Haniel proceeds into the two core categories.

• Became America’s No.1 in mosquito/vector control (VDCI, Mosquito Control Services, Aquatic Systems).

• Returned the France business to profitable growth for the first time since 2014 via a quality agenda.

• Scaled the Lumnia LED fly-control range and opened the Power Centre innovation hub in the UK.

• A reported pre-tax loss (£114.1m) reflected accounting remeasurement linked to the Haniel JV, not operating weakness; ongoing operating profit rose 13.3%.

2019 — Record organic growth and intensified M&A

CEO: Andy Ransom | Chair: Richard Solomons.

• Delivered the highest organic revenue growth in 15 years (4.5%), ahead of medium-term targets.

• M&A reached £316.5m across 41 deals, around 30 in Pest Control and nearly half of those in North America.

• Emphasised innovation as culture (“innovate or die”) and digital remastering of frontline service (PestConnect).

• Hit the 20% emissions-reduction target a year early; partnered with Cool Earth; entered Uruguay, Jordan and Sri Lanka.

2020 — COVID-19: defend, then pivot

CEO: Andy Ransom | Chair: Richard Solomons. The CEO described a three-phase approach — Crisis, Recovery, Strategic opportunity.

• Launched disinfection services across 60 countries in four weeks (training 7,000 technicians), generating ~£225m of revenue.

• Major balance-sheet protection: ~£100m+ of cost savings and ~£400m of cash-preservation measures, suspending M&A and the dividend and using the Bank of England financing facility (later repaid early).

• Accelerated the strategic decision to expand Hygiene beyond the washroom into surface and air hygiene (e.g. VIRUSKILLER).

• Resumed M&A later in the year as conditions stabilised.

2021 — Announcing Terminix and creating “Hygiene & Wellbeing”

CEO: Andy Ransom | Chair: Richard Solomons. Two landmark decisions.

• Announced (December) the agreement to acquire Terminix — to become the clear No.1 in North America and globally.

• At the September Capital Markets Day, launched the next evolution of the RIGHT WAY plan from January 2022: the enlarged Hygiene & Wellbeing category (folding in Ambius, Dental Hygiene and Cleanroom), a revised regional structure, and upgraded medium-term targets.

• Continued M&A at pace — 52 businesses acquired for £495.5m, part of 245 bought since 2016.

2022 — Completing Terminix: “a seminal year”

CEO: Andy Ransom | Chair: Richard Solomons.

• Completed the Terminix acquisition (October), creating the world’s largest pest-control company (~4.9m customers, ~58,600 colleagues).

• Integration plan built on seven workstreams; branch consolidation from 600+ to ~400 to drive route density and margin.

• Brand convergence: Terminix for residential/termite/SME, Rentokil for larger commercial.

• Raised the net cost-synergy estimate from at least $150m to at least $200m by 2025; continued ~one-deal-per-week pace, including first entries into Pakistan, Argentina and Israel.

2023 — First full integration year; the North America wobble

CEO: Andy Ransom | Chair: Richard Solomons.

• Delivered 4.9% organic revenue growth and a 16.6% margin despite inflation, but US growth in the second half disappointed.

• Launched THE RIGHT WAY 2 plan to reinvigorate US organic growth after a review found both weaker consumer demand and the company’s own sales-lead generation underperforming.

• Overachieved cost synergies ($69m vs a $60m target) and raised the total gross-synergy target by $50m to $325m by 2026; branch network already reduced by 97.

• Opened a new US science/innovation centre; made fresh North-America leadership hires; expanded the Trusted Advisor technician-lead programme.

2024 — Fixing North America while International powers ahead

CEO: Andy Ransom | Chair: Richard Solomons. A candidly challenging year.

• North America organic growth was just 1.5% as the integration weighed on performance, while International grew revenue 8.2% (organic +4.7%).

• Piloted satellite branches (smaller, fully branded, low-cost local hubs — 22 by year-end) to improve digital lead flow and local search presence.

• Overhauled paid and organic search marketing; pushed hard on five-star reviews; migrated branches onto the unified PestPac platform (49% of technicians).

• Piloted new sales/service pay plans and added a Customer Save team; integration targeted for completion by end-2026.

2025 — Turnaround taking hold; portfolio and structure simplified (Ransom’s last report)

CEO: Andy Ransom | Chair: Richard Solomons. Performance was in line with expectations, with clear signs the revised North-America strategy was working and improving second-half International growth.

• Disposed of the France Workwear business (treated as a discontinued operation), completing the long pivot to a pure Pest Control and Hygiene & Wellbeing company.

• Simplified the reporting structure into just two segments — North America and International — from 1 January 2025.

• Continued the satellite-branch rollout; ran a door-to-door sales pilot (judged a success as a pilot, with modest 2026 ambitions); introduced the Branch 360 “single pane of glass” management tool.

• Leadership transition: CEO Andy Ransom and Chair Richard Solomons both announced their departures; Paul Edgecliffe-Johnson joined as the new CFO.

VI. Financial analysis

After acquiring Terminix, a leader player in the US, the company is making moves to become more American and less from from the UK. They recently changed their functional currency to the USD, as North America represents around 60% of the revenue. The move makes sense as probably management wants to attract American capital and seek a valuation closer than Rollins.

The company has been involved in a mega-deal after acquiring Terminix and the synergies are below expectations. Large M&A is always harder than smaller acquisitions.

A decade ago, Rentokil had several non-core business and has disposed all of them focusing solely on pest control and hygiene. This has been a smart move and will allow the company to become more defensive.

However, the change to USD makes any comparative very challenging. To avoid any issues, I keep the historic figures until 2024 in GBPs, and add 3 years with the USD (reported by the company).

Revenue

Revenue has compounded steadily, with a step-change in 2022 from the Terminix acquisition.

From £2.2bn in 2012 to £5.4bn in 2024 — a 7.7% CAGR — with the bulk of the growth coming in two phases: organic and bolt-on M&A (~6% per year) through to 2021, then a step-change with the Terminix deal in October 2022.

Organic revenue growth in 2025 was 2.6% — at the low end of management’s medium-term 3-4% guidance — with North America at 2.2% and International at 3.7%. Pricing was the dominant component throughout 2024-25 as volumes proved soft in the early innings of post-deal integration.

By segment the post-2022 transformation is total: Pest Control North America rose from £1.0 in 2021 to $3.2bn in 2024, while the formerly dominant Hygiene & Workwear category fell as France Workwear was carved out and other smaller assets divested.

View — Rentokil’s growth profile post-Terminix has been below pre-deal expectations. The Company guided for an Adjusted Operating Margin above 19% by FY2025 at the time of the deal announcement; FY2025 actual was 15.5%. The gap explains much of the share-price under-performance versus pre-deal expectations.

EBITDA and operating income

Margins have expanded substantially over the decade — from mid-teens to low-twenties — but remain below their post-deal trajectory targets.

Adjusted EBITDA margin declined from 20.2% in 2016 to 14.9% in 2025

Reported Operating Income (EBIT) of $720m in 2025 trails Adjusted Operating Profit of $1,070m by approximately $350m — this gap reflects amortisation of acquired intangibles (Terminix customer relationships, brands; ~$200-250m/year) and ongoing termite-damage litigation provisions.

View — The margin story is the central operational debate. Bulls point to the FY2025 second-half acceleration, the $100m cost-reduction programme on track, and the North-America branch consolidation (from 600 to ~400 branches by 2026) as evidence that the integration thesis is intact. Bears point out that 5 years post-deal-announcement Rentokil is still below the margin guidance set on Day 1.

Earnings and free cash flow

Free cash flow has been the most consistent positive in the post-deal financials — and is what has supported de-leveraging.

FCF of $530m in 2025 was up 29% year on year, with a Free Cash Flow Conversion of 113% (ahead of guidance). Some of this was helped by real-estate disposals and one-off working-capital benefits, but the underlying conversion rate has been consistently strong.

Reported net income in 2025 of ~$470m sits below the Adjusted measure because of non-cash amortization of acquired intangibles and the cash and provision impact of US termite-damage litigation.

Net income is not an appropriate measure for this company as it’s impacted by non-cash items such as amortization of intangible assets that arise after acquiring a company.

Balance sheet

Leverage stepped up materially with the Terminix deal and is now de-leveraging.

Net debt rose from £1.0bn at end-2021 to £2.7bn at end-2022 (Terminix completion). By the end of 2025 it had de-leveraged to ~$3.2bn. If we includ leases, the total net debt stands at $3.8bn and leverage ratio at 3.7x. The Company has $2.6bn of liquidity headroom, including $1bn of undrawn revolving credit facilities maturing in October 2029.

Goodwill and intangibles together represent ~$7bn of the asset base — by far the largest single item — reflecting the cumulative consideration paid in Rentokil’s acquisitive growth, with Terminix being the largest single contributor. The Company has noted that goodwill impairment testing has not identified any need for write-downs to date.

Currency mix of debt at year-end 2024: 63% USD, 21% EUR, 14% GBP, 1% other — reflecting deliberate hedging of debt against forecast operating profit by currency. The 2025 currency-presentation change to USD partly recognises this dollar-weighting of the balance sheet.

View — There are no obvious hidden assets and no flagged hidden liabilities. The asset-light operating model is buried under a heavy goodwill stack; investors should assess returns on cash flow and ROIC, not on book equity.

Capital allocation

Capital allocation since the Terminix deal has been dominated by integration and de-leveraging.

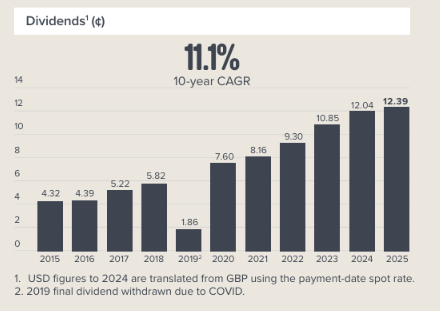

Dividend per share has grown every year since 2015 in line with the Company’s progressive dividend policy, except for 2019 impacted by the global pandemic. FY2025 DPS was $0.1239 on the ordinary share (equivalent to ~$0.62 per ADR after the 5:1 ratio), up 3% YoY. Trailing dividend yield is approximately 1.6%.

Share buybacks have been absent in this period — the Company has prioritised de-leveraging over buyback. With leverage now back to 2.6x and the goal of 2-2.5x in sight, capital-return optionality is expected to broaden from 2026.

Bolt-on M&A has continued at a modest pace ($130-180m/year in 2023-25 vs $7.25bn in 2022), with eight deals in 2024 adding ~$60m of annualised revenue. Capex has stepped up post-deal to ~$430m/year, reflecting Terminix’s larger footprint and continued investment in digital platforms.

I believe company should do share buybacks instead of dividend, considering:

There is no single majority shareholder that doesn’t allow for SBB

Company is not overvalued, and once Terminix is fully integrated, it has the potential for a multiple re-rating closing the gap with Rollins (which will be a function of margins and growth)

but, in the long-term, dividends can also offer a meaningful return to shareholders as they grew at a CAGR of 11% during the last 10 years.

Last, dilution to shareholders need to be considered as the company has financed some acquisitions with shares (e.g., Terminix), affecting the capital structure of the company.

On the positive side, the company increased capital when the stock was trading at high multiples.

Return on invested capital

ROIC has fallen materially post-deal and is the most important number to watch.

Pre-Terminix Rentokil ROIC ran at ~12-13% in the 2018-2021 period — solid for a services company though below Rollins’ 20%+. Post-deal ROIC has compressed to ~6-7% as goodwill and intangibles ballooned the invested-capital denominator.

Stripping out goodwill and intangibles gives a much higher operating ROIC (low-twenties), which is informative about the underlying operating-asset returns but is not the relevant number for shareholders — the goodwill is real money paid by the equity base.

The recovery path: the Company’s stated targets imply ROIC recovery toward 10%+ over the medium term as integration completes, the cost programe delivers and margins step up toward 20-22%. This is the central operational debate for the equity story.

View — Six-percent ROIC is below the cost of capital for almost any reasonable assumption set. For Rentokil to be a value-creating investment from here, ROIC must move materially higher. The pre-Terminix history suggests the operating business is capable of high-teens unlevered returns; whether Mike Duffy can deliver that on the larger goodwill-heavy base is the headline question for the next 3-5 years

VII. Valuation

⚠️ Not Investment Recommendation⚠️

As of late May 2026, Rentokil’s NYSE ADR (ratio one ADR for five ordinary shares) traded at approximately $23.95. The implied market capitalization, enterprise value and trading multiples on FY2025 results are summarized below.