Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

One of the readers recommended to take a look to Azelis, IMCD’s main rival. I love receiving suggestions from all of you, so I took it seriously.

Here is an analysis of Azelis. I’m not covering any more the sector, and business model analysis will be shorter than IMCD as some things are common to both companies. You can fin the prior analysis here:

I. Introduction to Azelis

I.I Introduction

Azelis is the second largest specialty chemicals distributors, just behind IMCD. Two similar companies, but different exposure, balance sheet, and valuation.

The company is headquartered in Antwerp, Belgium.

It has a similar geographical exposure as IMCD, being EMEA the largest region representing ~50% of the EBITA.

Company has a higher leverage than IMCD, being a BB+ company vs. IMCD’s BBB- rating. This is not material, but provides a quick overview of the balance sheet of the company.

I.II History of the Company

Similar to IMCD, Azelis has grown by acquiring dozens of companies. During its past history, it was owned by private equity firm EQT, which then exited through an IPO and subsequent sales.

Company was founded by a man called Dr. Hans Udo Wenzel, a German business executive and entrepreneur in the specialty chemicals and ingredients distribution industry.

In 1996, he acquired an Italian specialty chemicals distributor called Organa.

This is often considered as the starting point of Azelis.

During the next years he continued acquiring small distributors in Italy and created Novorchem.

In 2001, Azelis was created through the merger of Novorchem (Italy) and Arnaud (France), establishing a chemistry-driven specialty distribution platform.

The company will be headquartered in Antwerp, Belgium.

Main reasons is that Belgium is major European chemicals hub. Port of Antwerp is one of the biggest chemical ports in the world, and close to Germany, the Netherlands, and France.

It was also a neutral location for a multinational group.

During the early years (2001–2014) company focused on acquiring European distributors to build critical mass.

The first acquisition came in 2002 and was in the UK.

In 2003, Azelis expanded to the DACH region (Germany, Switzerland, and Austria).

In 2004 company strengthened its operations in the Benelux region and expanded to Spain and Portugal.

In 2005, the company acquired a Nordic distributor, and will now cover a significant part of Europe.

In 2006, the company was acquired by 3i Group, initiating a series of multiple private equity ownership.

By that time, IMCD was now owned by a second private equity firm ABN AMRO.

With 3i Group, the company kept expanding into Europe (the Netherlands, Germany, UK, Turkey, Serbia, etc.), and reorganized all companies under the Azelis brand in 2011.

Additionally, the company expanded outside Europe. It opened offices in APAC region in 2013, including Shanghai, Beijing, Tokyo, etc., and tackled the US market by acquiring Koda Distribution.

After this expansion, the company expanded its revenues to around €1bn and 3i sold sold the business to Apax Partners in 2015. Under their ownership, the company kept expanding.

Acquired more companies in Europe, strengthening its operations in Italia, Switzerland, Nordics, etc.

Additionally, company kept expanding in APAC region (Australia, new HQs in Singapore, etc.), and in the Americas.

Three years later, Apax sold the company to EQT/PSP

EQT acquired the company through Fund VIII together with PSP Investments.

Under their leadership, the company completed around 60 acquisitions including the major Vigon International deal, grew revenue from €1.9bn to ~€3bn, and expanded materially in the Americas and APAC

The pandemic and the subsequent growth fueled by the bottlenecks of 2021, EQT IPOed the company just 3 years after.

In September 2021 it listed on Euronext Brussels at €24/share, raising €880m to partially deleverage to ~2.5×.

2022–2023 — Peak performance: Revenue reached ~€4.4bn and adj. EBITA margin peaked at ~12.5%, driven by post-COVID restocking demand and continued M&A. The business refinanced its debt into a bond-and-term-loan structure, but at materially higher rates as the ECB tightened aggressively.

2024 — Leadership transition: Anna Bertona succeeded Dr. Hans Joachim Müller as Group CEO on 1 January 2024, after serving as CEO of Azelis EMEA. She is the first internal promotion to the Group CEO role, having joined in 2014 as Chief Strategy & Principal Officer.

2025 — Deterioration and stress: Three consecutive years of negative organic revenue growth (driven by customer destocking, tariff uncertainty, and APAC structural pressures) compressed adj. EBITA margin to 10.0% and pushed net profit down 40% to €113m. Net leverage rose to 3.3×, the CFO departed, and the stock has declined -71% since going public.

EQT has gradually sold its stake in Azelis until final exit in 2026.

This is a normal strategy when a private equity divests through an IPO. EQT couldn’t sell all its 70% stake at once during IPO, as that would put pressure on the share price.

IPO investors usually impose lock-up agreements to align interests.

However, the multi-year strategy has taken longer than normal timings and has probably impacted the IRR of the investment.

EQT Fund VIII is a 2018 vintage — therefore, it needs to return the capital to investors during these years. Company finally exited in February after 7 years invested. This can potentially mean that EQT does not foresee major recovery soon, and/or the sale was part of a planned liquidity strategy.

From IPO to February 2025, the fund sold half of its stake at €18-26 per share.

Major sell came in November 2025, when the fund sold nearly 20% of the company in a private placement to Temasek and other investors. Following the sale, EQT retained about 10% stake, and was subject to a standard 90-day lock-up period.

After the lock-up ended, EQT sold the remaining stake and exited the company.

In any case this must be taken as a negative development, as the sale from EQT is part of the investment strategy. In fact, having no controlling shareholder can make Azelis a new target for future PE funds.

The group today operates in 63 countries with 4,206 employees, serving 65,000+ customers through 2,800+ principal relationships.

II. Company Analysis

Note: Azelis is a very similar company to IMCD. Given we’ve already covered the business model of IMCD in the prior post, this section will be shorter.

II.I Company Introduction

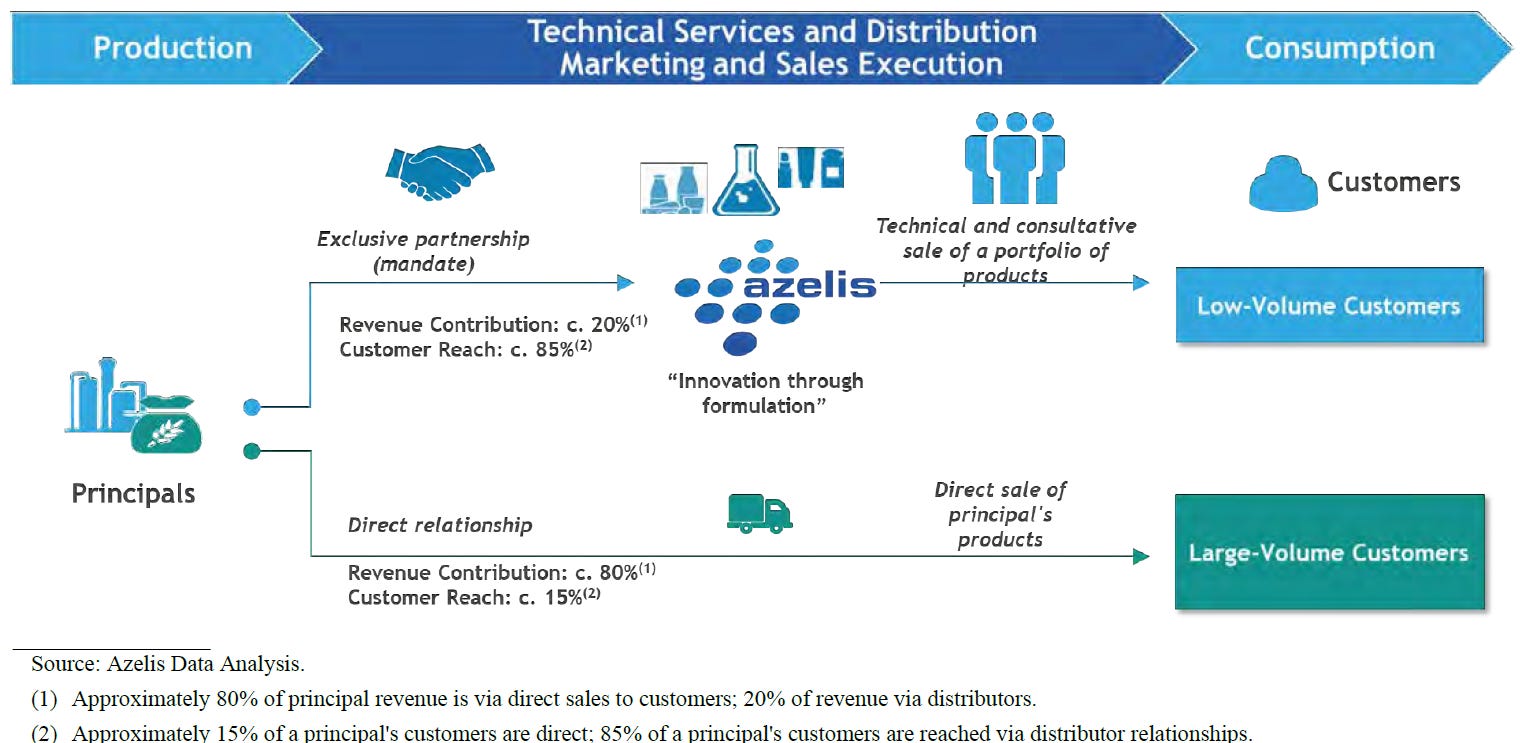

We already covered during the analysis of IMCD, but it’s important to recall that Azelis addresses 85% of the customers of the principals, representing 20% of the revenue.

The perfect Pareto rule applies here, where Azelis does what Principals can’t — distributing chemicals in a very fragmented industry.

It’s highly unlikely that principals try to by-pass companies like Azelis or IMCD as it’s not profitable to focus on smaller clients.

Azelis generates revenue by selling specialty chemicals and food ingredients, enhanced by value-added services

Value-added services include formulation expertise, regulatory support, warehousing, and marketing. These services improve margins without being separately charged to customers.

The business runs an asset-light model, outsourcing its warehousing and logistics while maintaining strict third-party audits to uphold its standards.

Capex/revenue is below 1% revenue

It’s the same model as IMCD which helps the company navigating challenging times like the actual

II.II Key Strengths

Azelis is one of the only two global pure-play specialty chemicals and good ingredients distributors

Following IMCD, Azelis is currently #2 player worldwide

Company operates in more than 56 counties, and is the leader in the Americas and holds second place in EMEA, with a growing APAC presence.

Same as IMCD, Azelis provides formulation services

The company has 70+ laboratories spread across the globe

While formulation doesn't generate direct revenue, it drives strong customer loyalty and stickiness, since formulations are tied to products only Azelis exclusively distributes.

The business serves 2,800+ principals and 55,000+ customers across life sciences (63% of revenue) and industrial chemicals, with no significant concentration by product, customer, principal, or geography.

II.III Management Team

Azelis operates with a lean five-person executive team; two of those five roles changed hands during 2025 itself, and a third had a significant transition in early 2024 — making this one of the most disrupted management periods in the company’s listed history

Anna Bertona, CEO — joined 2013, became Group CEO January 2024 (first internal promotion to the role)

Boris Cambon-Lalanne, CFO — joined January 2026, replacing Thijs Bakker who stepped down after 10 years

Evy Hellinckx, CEO EMEA — joined 2016, became CEO EMEA in January 2024 (same day as Bertona’s promotion)

Todd Cottrell, CEO Americas — joined September 2023, external hire from Hempel A/S

Benoit Fritz, CEO APAC — took over September 2025, replacing Sertaç Sürür who left “for personal reasons”

Same as IMCD, there is a new management team — a new cycle in the chemicals distribution sector is for sure taking place.

Something surprising is that neither IMCD nor Azelis have profiles entirely focused on strategy and M&A in their executive teams.

These companies require complex decisions and strategy in order to sustain growth and keep acquiring companies.

I’m missing some profiles in the Executive Committee focused solely on strategy and having a CFO with more investment banking background.

Bertona has ample experience in the chemicals sector, having spend time in consultancy and other companies

30+ years of experience across consumer goods, automotive, and chemicals

Career before Azelis: partner at A.T. Kearney, focused on chemicals strategy, sales excellence, and post-merger integration

At Azelis: joined 2013 as Group VP Strategy & Implementation → Chief Strategy & Principal Officer 2014 → CEO EMEA 2016 → Group CEO January 2024

Education: MSc Industrial Design Engineering, Delft University of Technology; MBA, Rotterdam School of Management

Total remuneration in 2025: €964,746 (base €784,128 + STI €180,618; no LTIP vested in 2025)

Bakker was the financial architect of Azelis from €90m EBITDA and 7x leverage to a listed company — his departure at a moment of margin compression and 3.3x leverage is the most significant governance event of 2025

Led the 2021 IPO, all debt refinancings, and approximately 40 M&A transactions

At the time of the Q3 2025 call, Anna Bertona publicly acknowledged: “When he joined Azelis, we had an EBITDA of €90 million, leverage of almost seven, and a disjointed finance organization”

Boris Cambon-Lalanne, effective January 2026.

More than 20 years at Solvay, where his most recent role was Capital Markets Director. Prior to that he was Finance Director for Solvay Materials, Finance Director…

He is an outsider to Azelis — no prior connection to the company or the specialty distribution sector.

His first public appearance was the FY2025 earnings call in February 2026, where he introduced a formal capital allocation priority framework (EBITDA growth → deleverage → dividend → M&A/buybacks) and confirmed the cost savings programme delivered more than €20m run rate

Difficult to assess what to expect from him in the long-term, but compared to CFO from IMCD, it might seem more strategic rather than accounting/audit background.

He has strong challenges ahead.

II.IV Retribution

Similar to IMCD, the retribution system is not fully aligned with the value creation drivers, but has some interesting topics included.

CEO and CFO earn short-term and long-term bonuses depending on factors such as EBITDA growth, etc.

Short-term criteria are the following:

50% of the weight is attributable to Adjusted EBITA, which does not capture organic growth, but rather the EBITA level.

20% is gross profit.

10% is the net working capital, which is interesting.

There is 20% attributable to individual performance, and above all, an ESG multiplier between 0.9x to 1.1x.

I consider that these criteria are not fully aligned with shareholder’s interest: