Disclaimer. Please read full disclaimer at the end of the page before reading the article. This publication is only for information and entertainment purposes. It doesn’t constitute financial advice.

The information provided in this blog is for informational purposes only and should not be considered as financial, investment, or professional advice. The valuations and analyses presented here are based on publicly available

Please remember that nothing in this post is investment recommendation.

What a year for PayPal shareholders, including myself.

So far, I’ve lost nearly 40% in the stock, 46% after accounting the impact of the weaker USD. I bought the shares during April 2024 at an average price of ~$68 per share and kept them until now, where I will go through what will be my decision.

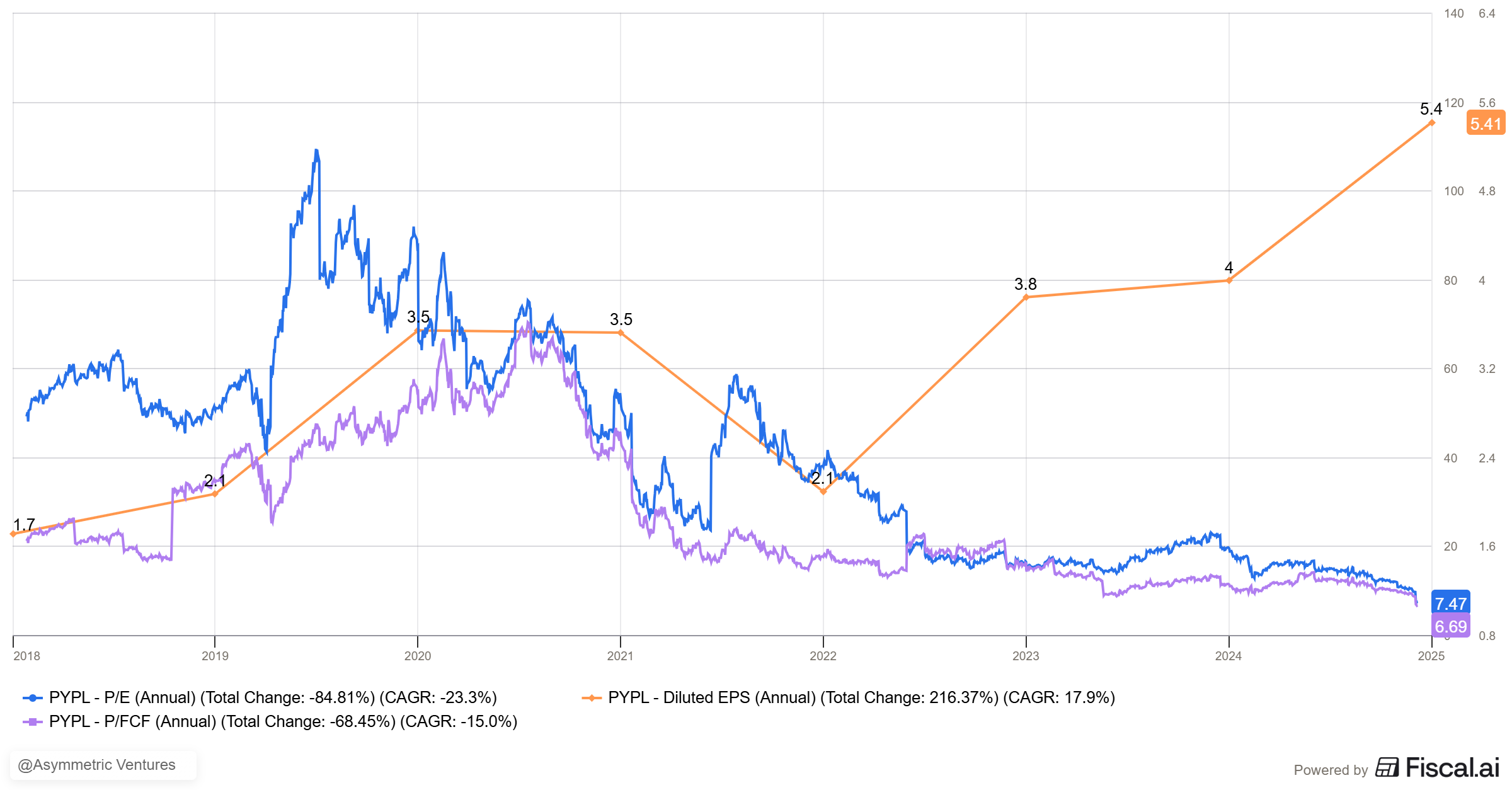

In terms of valuation, the stock suffered a brutal re-rating over the past years.

While EPS stands at historical max, multiples has significantly contracted over the past decade.

From extreme multiples during 2021-2022 period of 50+ times FCF, to reasonable multiples of around 15x earnings until the recent crash.

Today, the stock trades at 9x 2025 FCF, and according to Marketscreener at 6-8x next 3 years earnings.

Once again, the stock market teaches us a fundamental lesson: a stock declining with an optically low P/E doesn’t mean it’s cheap.

It will be cheap if PayPal proves the current narrative to be wrong, something it didn’t do during the last results.

It’s my worst investment since I created this blog and I have to admit it’s probably a mistake, although I believe market is overreacting.

The Recent Collapse

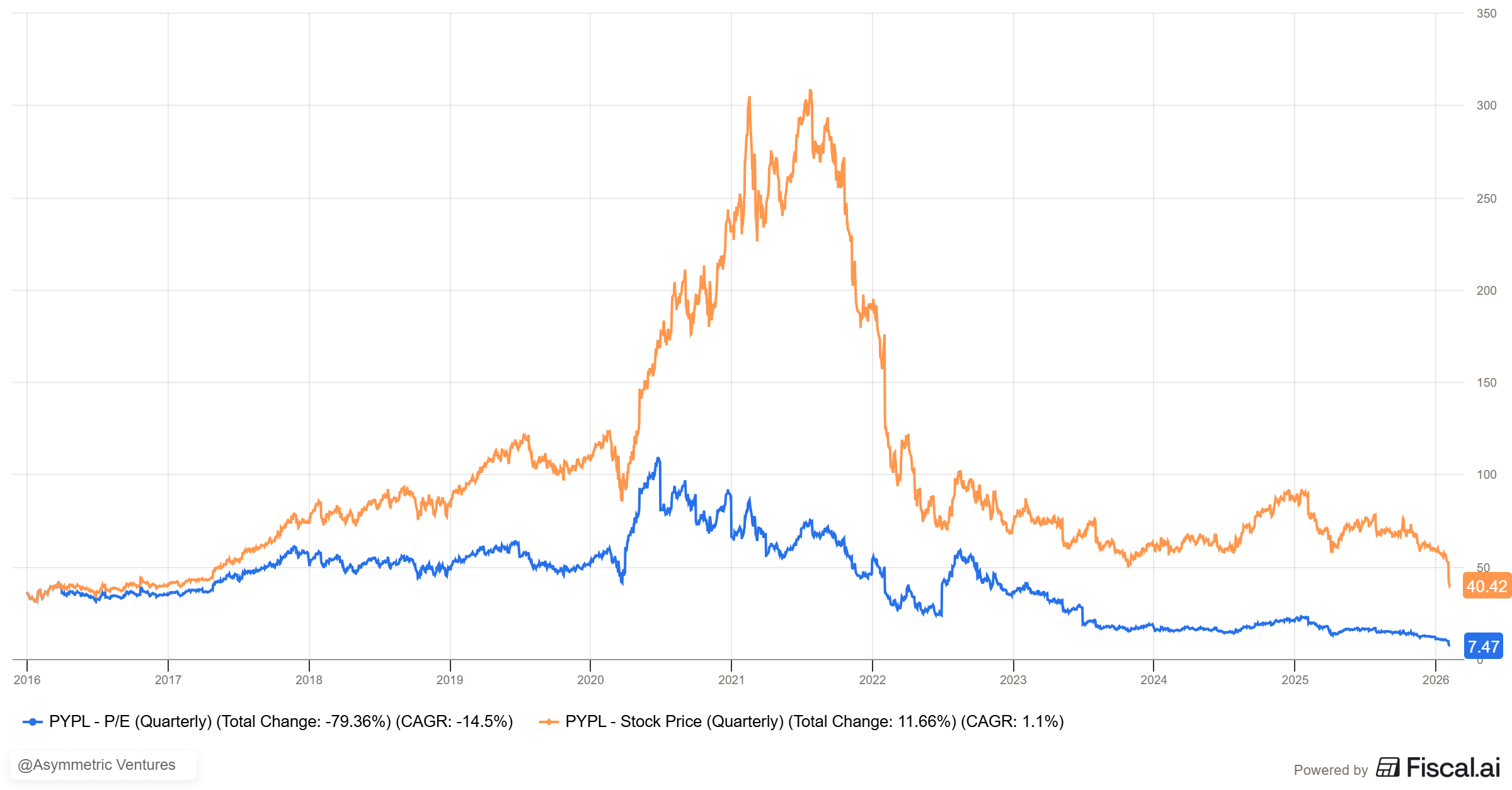

Introduction

The stock just suffered a brutal 19-20% drop some days ago (February 3, 2026) after reporting Q4 2025 results. The price fell to around $42-43, representing approximately a 50% decline from early 2025 highs when it was trading around $81-90. The year's peak was $91.81 in January 2025.

There were four key factors behind the collapse:

Disappointing results that were below analysts’ expectations (although I don’t care about their quarterly expectations, a stock like PayPal missing estimates will inevitably suffer more).

Disastrous 2026 Guidance The company projects EPS could actually decline or grow minimally in 2026, when Wall Street expected 8% growth.

CEO Replacement Alex Chriss, who arrived in 2023 to turn the company around, has been replaced. The board clearly stated that "the pace of change and execution was not in line with expectations". Enrique Lores (current HP CEO) will take over on March 1.

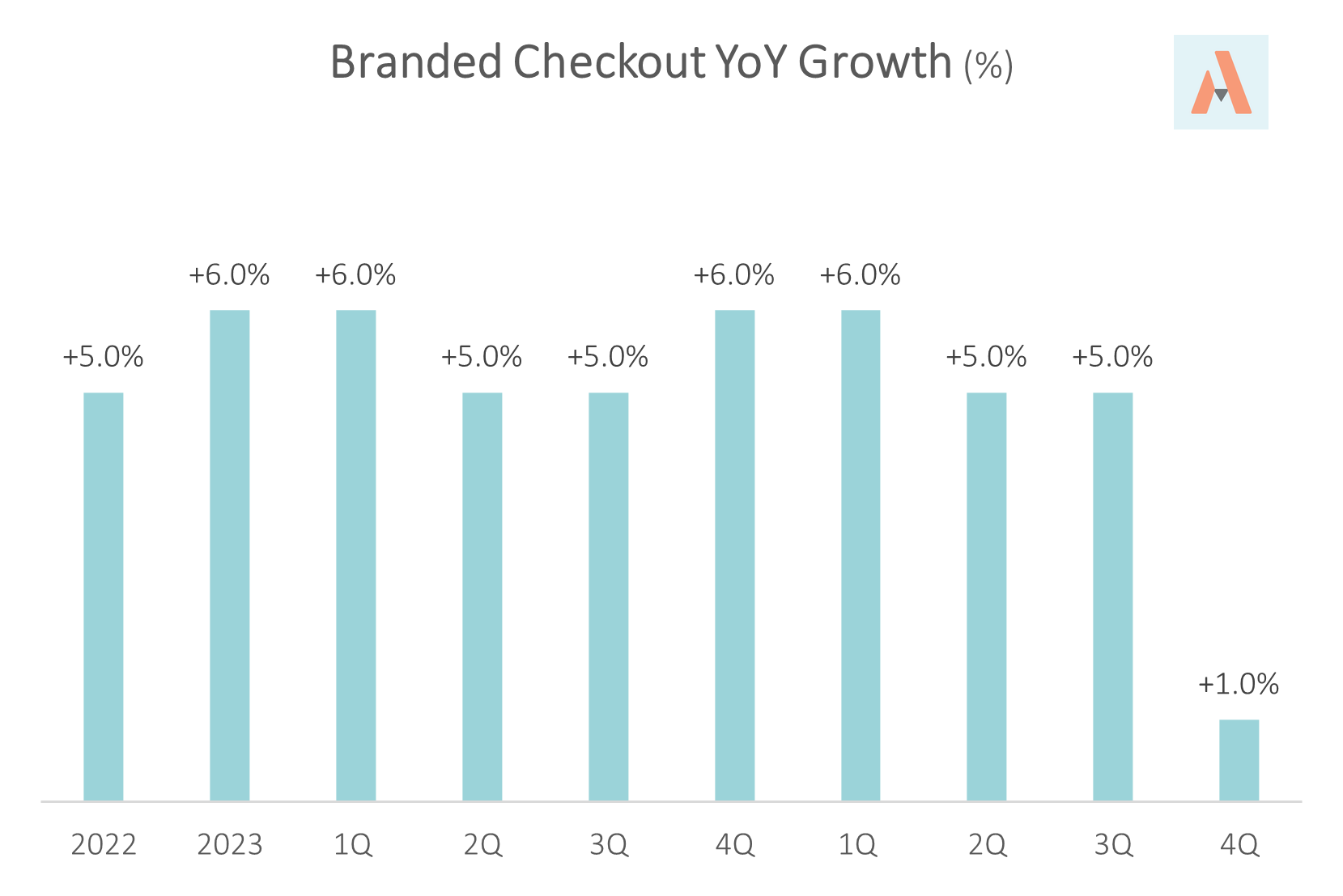

The Core Problem: Branded Checkout This is the heart of the issue. Branded checkout growth (the PayPal button you see at online checkout, their highest-margin business) collapsed from 6% in Q4 2024 to just 1% in Q4 2025. This is critical because it's the most profitable business and what differentiates PayPal from competitors.

Addressing Some of the Main Issues of 2025 FY Results

PayPal Total Payment Volume (TPV) comes from three different sources:

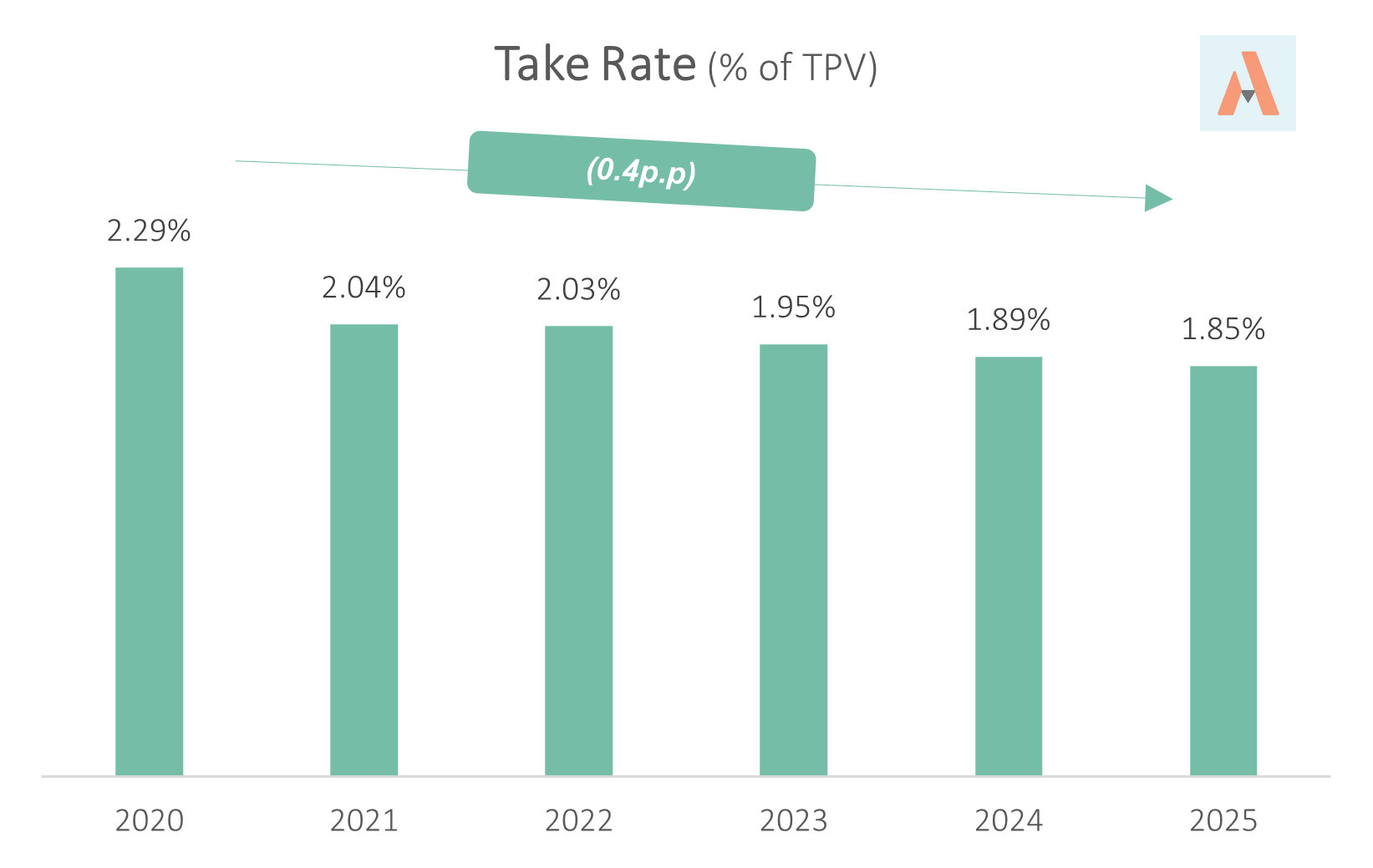

Branded checkout (online) — This is when customers see and click the PayPal button at online checkout to pay using their PayPal wallet or account. The customer knows they’re using PayPal, and the brand is very visible. This provides the highest margin business (take rate of around 2.25% of the volume).

P2P & Other Consumer — This includes Peer-to-Peer payments like sending money through PayPal, etc. This activity provides little amount of fees. This is offered through PayPal and Venmo.

Payment Service Provider (PSP) — Unbranded payment processing where PayPal processes transactions in the background, but the customer never sees the PayPal brand. Services are mostly offered through Braintree (company sold by Bryan Johnson — the man behind the Don’t Die Netflix documentary).

#1 Is Branded Checkout Slowly Dying?

Branded checkout is the core business for PayPal. It’s the checkout bottom you find in websites when you plan to purchase an item. It’s widely used when you don’t trust 100% the merchant’s website.

Growth has been stable in the past at around 5-6% YoY. However, last quarter saw a growth of just +1% YoY.

This is an issue because branded checkout is the crown jewel. The service driving the highest margins.

As other services grow faster than branded checkout, take rate is declining from 2.3% in 2020 to 1.85% in 2025.

It’s weight has remained stable, a clear signal that PayPal is not able to extract more from this service.

If you add to this poor quarter a very poor guidance, the result is a 20% price drop.

#2 PayPal Faces Intense Competition

The business faces intense competition mainly from Apple Pay and Google Pay, where both companies are eating PayPal’s lunch slowly.

Apple Pay and Google Pay are built into devices and browsers

They’re the default payment option on iPhones, Macs, Chrome

One-tap checkout with Face ID/Touch ID—ultra frictionless

PayPal requires users to click their button, then log in (extra steps)

However, no this seems logic, but prior quarters where showing a modest growth of +5 to 6% YoY, which is very modest in the sector, but still provides a decent growth for a company that traded below 15x earnings.

“We saw pressure across our retail merchant portfolio, particularly among lower and middle-income consumers” CFO Jamie Miller during 4Q ‘25 earnings call

While the quarterly results are very weak with just a 1% YoY increase in Branded Checkout, it seams that:

Lower and middle-income consumers are pulling back on discretionary spending

They’re prioritizing necessities over online shopping

This is a macro headwind hitting PayPal harder than competitors

The K-shaped recovery: Affluent consumers (who might use Apple Pay or premium credit cards) are doing fine.

This should also be seen as a warning sign: is the US economy becoming weaker? Should we worry about this, not just for PayPal? The answer is yes:

#3 Growth In The US Is Also Slowing Down

During 2025, all metrics decreased, some of them signaling issues:

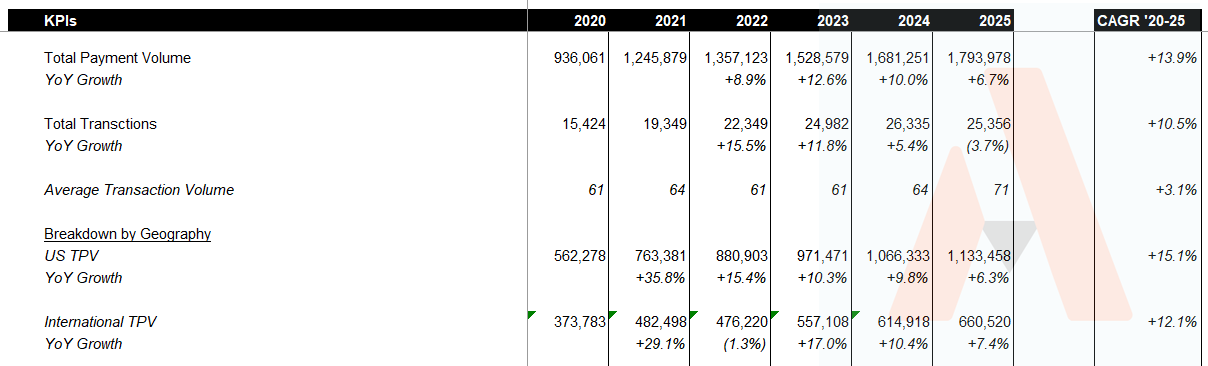

Total Payment Volume (TPV) growth remains solid at +6.7% YoY

The number of transactions has decreased by 3.7%, which led to an increase in the average transaction volume from $64 to $71 per transaction.

By geography, growth in the US is slowing down, from c.10% to +6% during 2025.

US retail seems to be in a difficult period, or at least this is how PayPal’s management frames it: Branded checkout deceleration was "driven by weakness in U.S. retail, international headwinds and tougher comparisons".

While it’s true that some companies are facing difficulties, it’s not clear that the reasons provided by PayPal are accurate.

#4 Transactions Per Active Account Are Declining

Uncertain if its due to the macro environment or the product offering, the reality is that users are transacting less frequently with PayPal’s products.

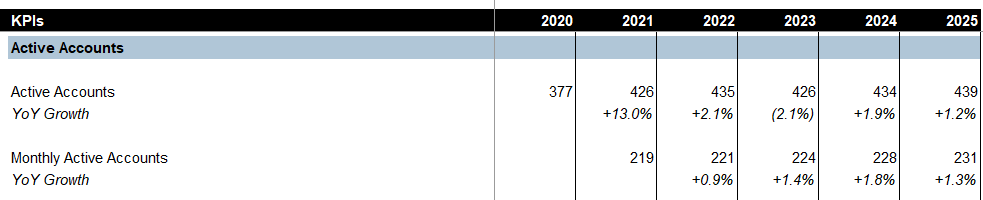

Transactions per active account: down 5% (trailing 12 months)

People have PayPal accounts, but they’re using them less

Even if PayPal has currently 439 million active accounts, if each person uses it 5% less often, total volume shrinks. This suggests:

PayPal isn’t “top of mind” anymore

Users are choosing alternatives (Apple Pay, cards, BNPL)

The wallet has become less sticky

While PayPal keeps increasing the number of customers, the rate is simply very low considering the tailwinds of the digital industry.

#5 Checkout Page Real Estate Is Crowded

Company is facing competition from all directions, including Apple and Google, Affirm/Klarna for Buy Now Pay Later, etc.

As internet evolves and competitors offer cheaper products, the risk of de-prioritizing PayPal by merchants becomes real.

PayPal has one of the highest take rate in the industry, charging merchants ~3% of the value

On the other hand, Apple Pay it’s nearly free — because Apple doesn’t act as an intermediary.

#6 PayPal’s Fixes Haven’t Worked Out

Since Alex Chriss took over as CEO, the company tried several strategies to optimize and improve the operations of its checkout process, including:

Fastlane: One-click guest checkout (still rolling out)

Enhanced rewards program: Cash back offers (limited adoption)

Redesigned PayPal app: Better UX (hasn’t moved the needle)

Passkeys: Biometric login (too new to impact)

These initiatives are directionally correct but haven’t achieved scale fast enough. Management admitted: “We have not moved fast enough or with the level of focus required.”

Even when Fastlane shows 80% conversion rates in tests, it’s only with a small group of merchants. Getting broad adoption takes time PayPal doesn’t have.

#7 Alex Chriss Couldn’t Fix It And Got Fired

The former CEO — who started is tenure saying they were “going to shock the world”— was fired after the strategies deployed didn’t achieved the expected results.

During the last quarters he tried:

Investing in product (Fastlane, rewards, UX)

Pushing partnerships (Google, OpenAI, Microsoft)

Improving merchant tools

Marketing campaigns

But none of them had meaningful impact, and the board’s verdict was very clear:

"The pace of change and execution was not in line with expectations."

Now, the question is: where expectations of the board aligned with the reality of the competitive landscape? Is the board wiling to take on risks? Do they have a clear view on what should be the strategy going forward?

I believe Alex Chriss overpromised many times, and under-delivered many others. Setting the bar to high can lead to excessive expectations, and when not met, it’s time for a change.

What Are the Options Going Forward?

The new CEO Enrique Lores faces a very difficult challenge, and will certainly need to take one the following paths:

Accept branded checkout will be a low-single-digit growth business forever and he starts milking the cow as much as possible, maximizing efficiencies inside the company to deliver all possible cash to shareholders.

Make a massive bet on transforming how PayPal competes (maybe through AI/agentic commerce, maybe through totally reinventing the checkout experience).

Pivot the company toward unbranded PSP and Venmo monetization, accepting lower margins but higher volume and compete against firms like Adyen, Stripe, etc. Not a recommended path, but maybe it’s the only alternative to survive.

"Enrique is widely recognized as a visionary leader who prioritizes customer-centric innovation with demonstrable impact. His strong track record leading complex transformations and disciplined execution on a global basis will ensure PayPal maintains its leadership of the dynamic payments industry now and into the future,"

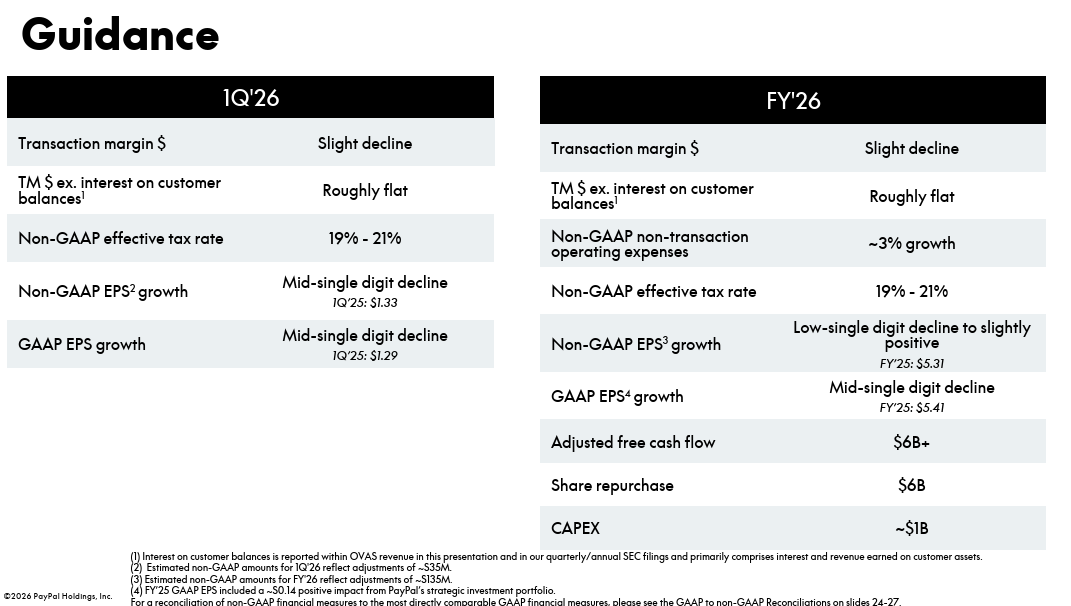

The 2026 Guidance Includes Repurchasing Around 10% of the Shares

While the guidance looks bad, but we should add some context:

Transaction margin is expected to slightly decline — This has happened in the past (e.g., 2022 and 2023). We shouldn’t be surprised.

At EPS level, it will decline on a GAAP basis, which also happened in 2022.

Should we think this guidance as a very poor one to give the new CEO room for improvement?

Last, the is a major thing we should consider. Despite a potential negative transaction margin, the company will generate strong cash flow and will repurchase a significant amount of stock.

They announced a SBB program of $6bn. After excluding $1bn of SBC, the company will effectively repurchase $5bn of shares, representing 13% of the market cap. Am I missing something??

Market Now Discounts PayPal’s Fall

The market is already discounting a scenario of profit decline, as the company is currently trading at 8.6x 2025 FCF.

Current market cap: $40 per share x issued shares = $37,000

Last 12M FCF: $4,300 million

Company is guiding around $6bn of adjusted FCF which will translate to $4.0-4.5bn of FCF Adjusted by SBC, etc.

While The Narrative Remains, The Business Delivers Acceptable Economics

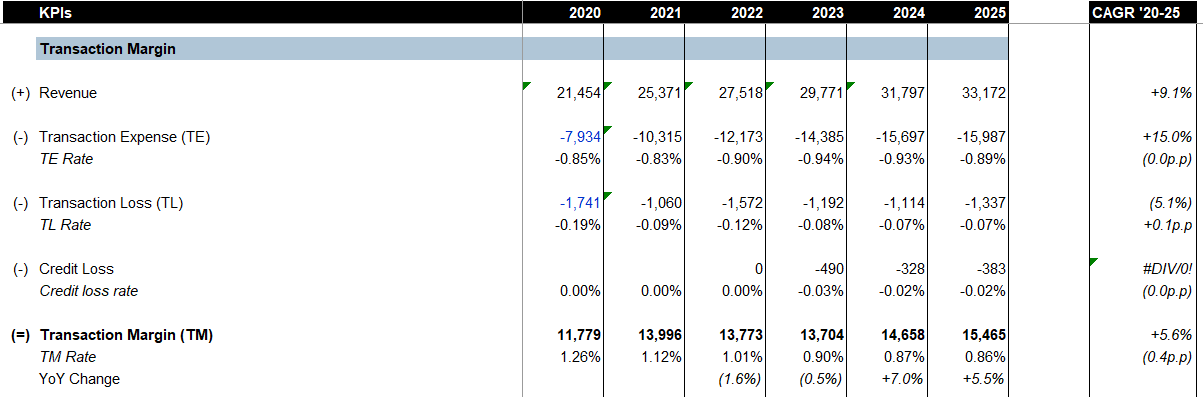

Transaction Margin Remains Stable But Might Decline In The Years Ahead

Transaction margin increased by +5.5%, in line with the historical average. TM rate stood at 0.86% of TPV, which is stable vs. the prior year, but has fallen from 1.26% in 2020.

TM will decline during 2026 as the company is guiding lower TM. This might be due to an expected decline in both volume and take rate.

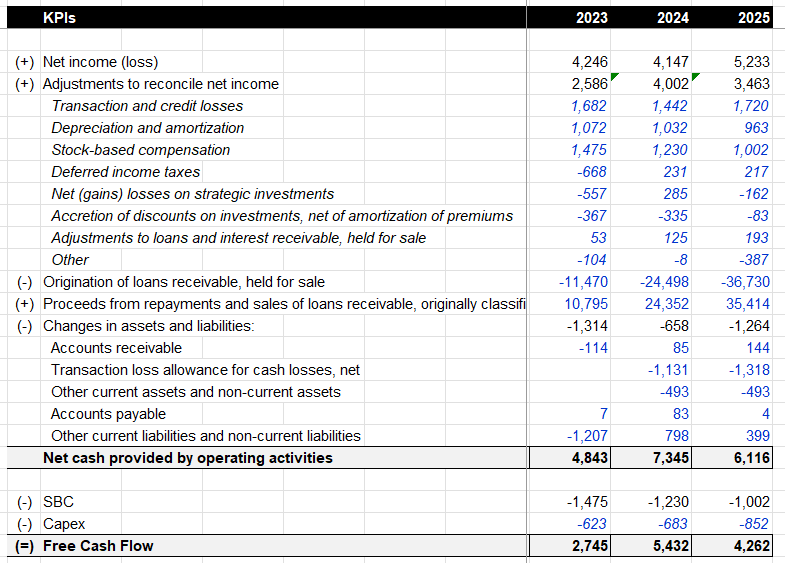

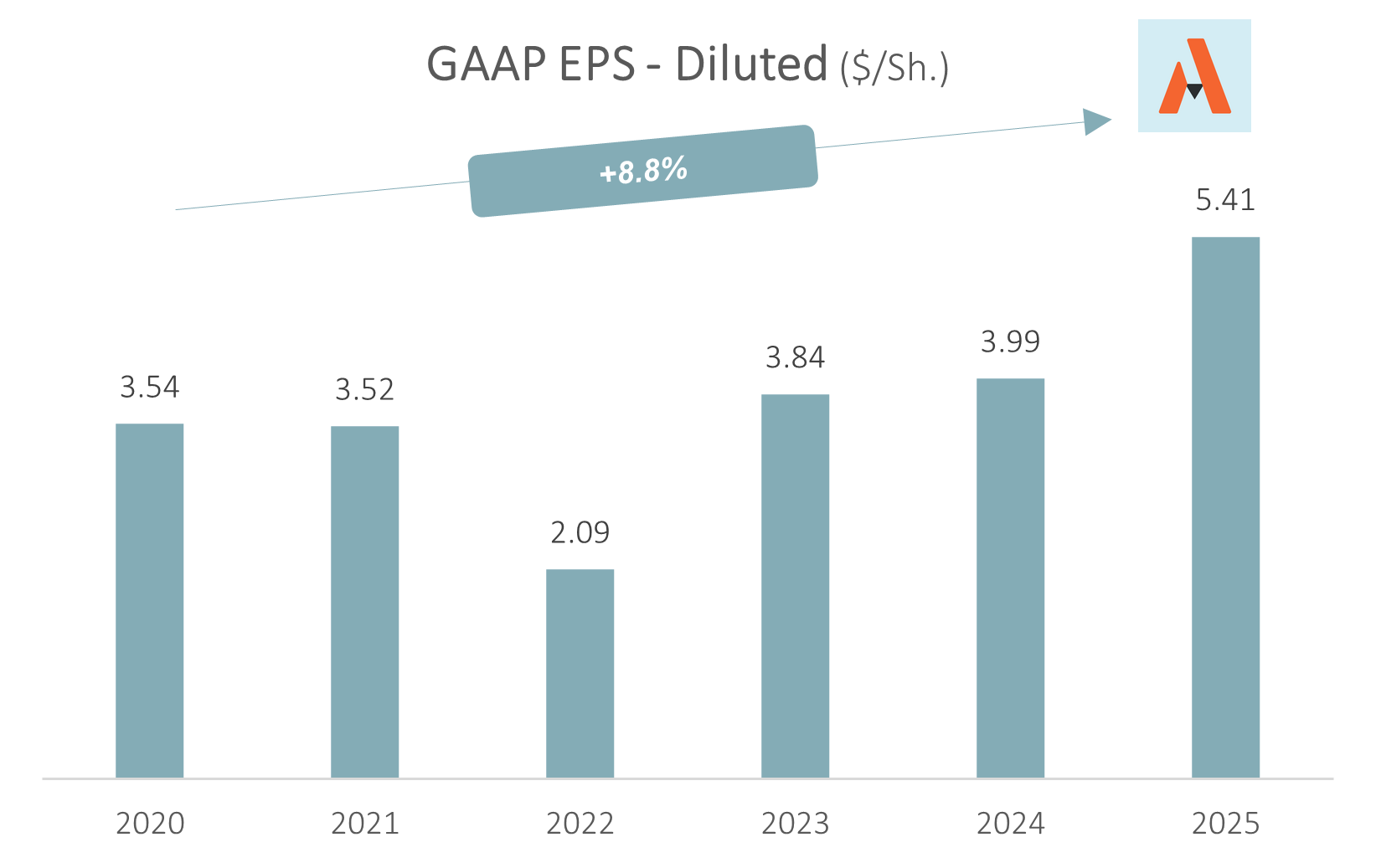

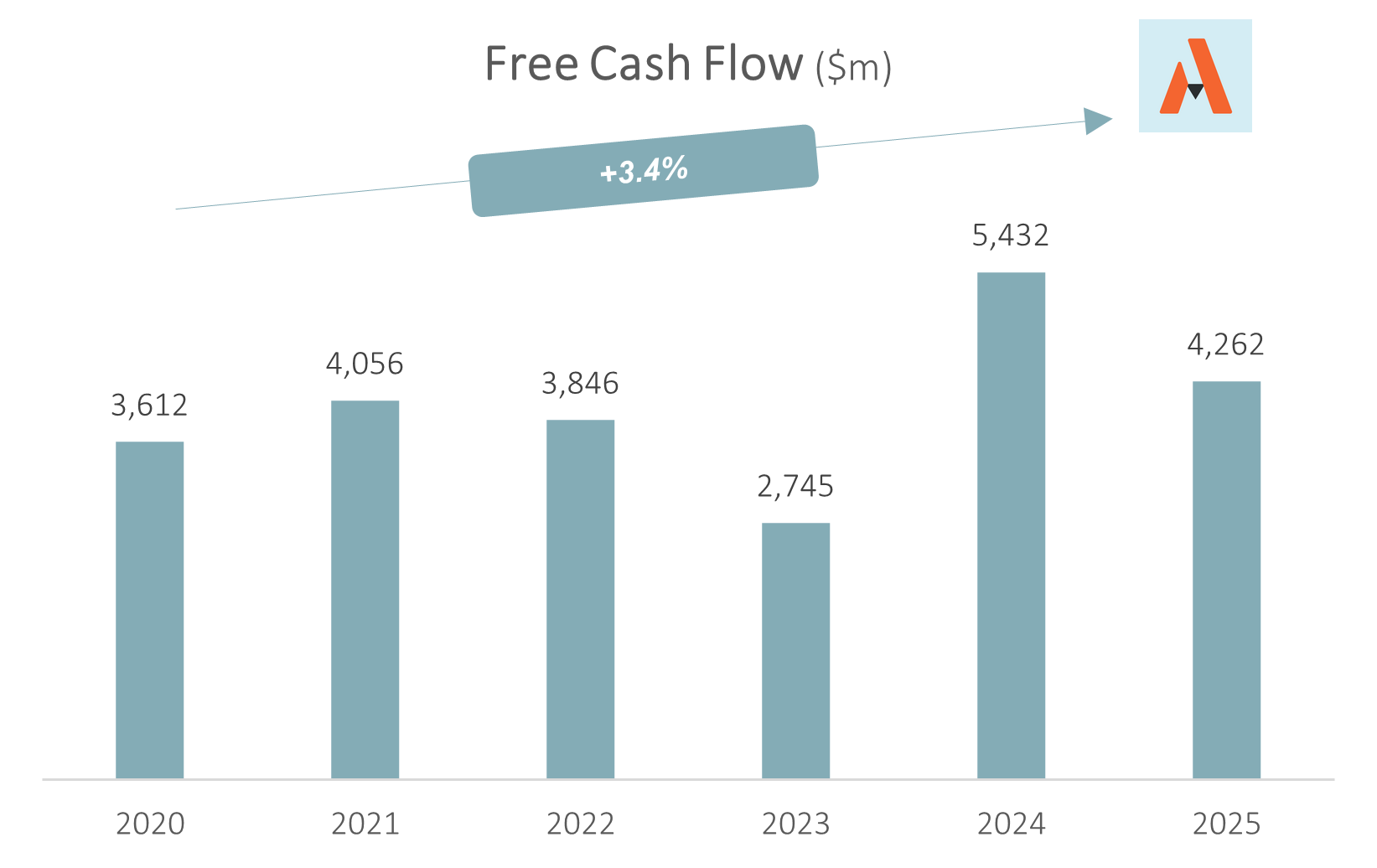

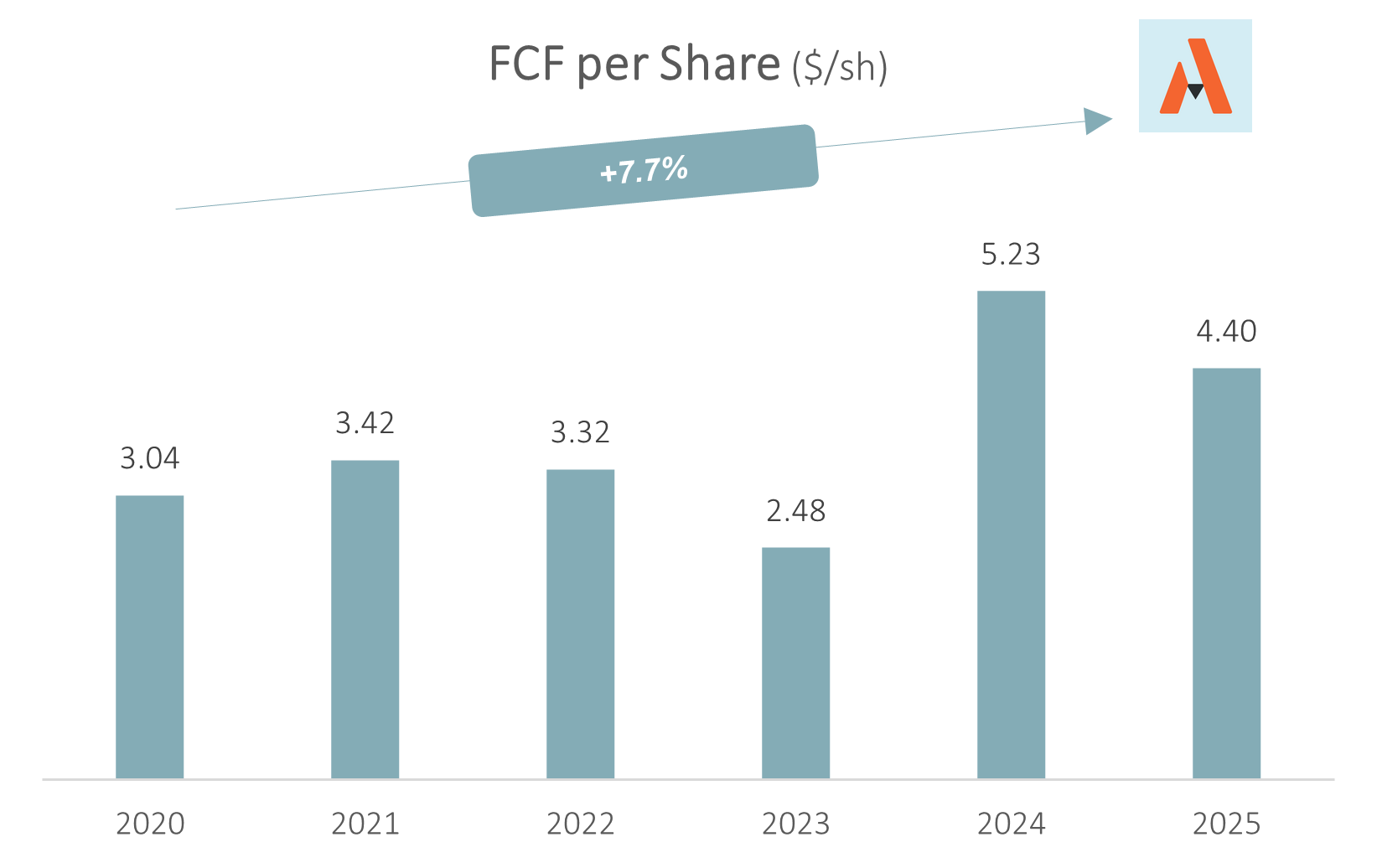

Growth in EPS and FCF Has Been Solid

When analyzing the company, I started excluding their non-GAAP adjustments for a simple reason: every year the company reports extraordinary expenses, restructuring, etc. One year is extraordinary, five years is ordinary.

However, even if we don’t consider these adjustments, EPS has increased over the last years, and now the company trades at 8x EPS.

In terms of FCF, it has remained strong at above $4bn. Please note that this FCF includes SBC as a cash expense.

FCF per share stood at $4.4 during 2025, implying a FCF yield of 11% under current share price. But, under current guidance, a lower FCF must be expected for the year ahead; therefore, we can’t consider the current multiples as valid.

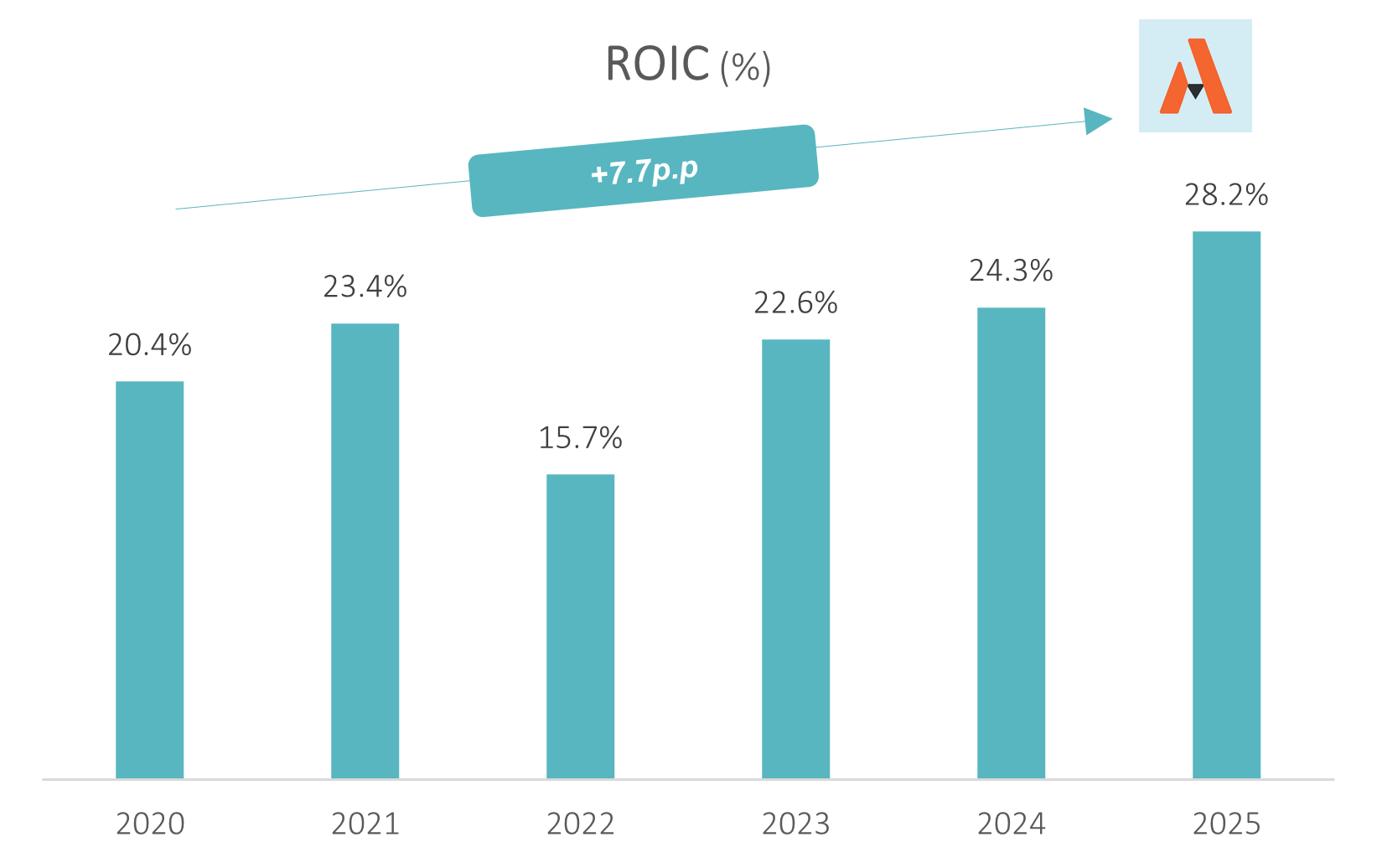

In The Meantime, PayPal Generates 20%+ ROIC

Profitability metrics remained solid over the past years.

ROIC stands above 25%

ROCE stands at 25%

Overall, the profitability metrics are very solid.

Conclusion: What I Will Do

PayPal is facing strong competition from other players and has huge challenges ahead. Same as all the companies I own, PayPal is no different. However, there are reasons to consider that PayPal competitive positioning will weaken in the coming years.

Many players are going to steal market share and for sure PayPal will face huge challenges ahead.

The results and the management of the situation have been poorly managed by the company. One bad quarter and the CEO is out.

I’m wondering what is the strategy proposed by the Board. So far no plan has been presented, but I will expect the new CEO to present a new strategic plan in during 2026.

So, what should I do? Sell? Buy more? Do nothing?

The company faces huge competition and we are certainly not going to see strong growth. Company should conform with modest growth between 0% and 5% per year.

In the meantime, the company plans to repurchase 13% of the shares during the year.

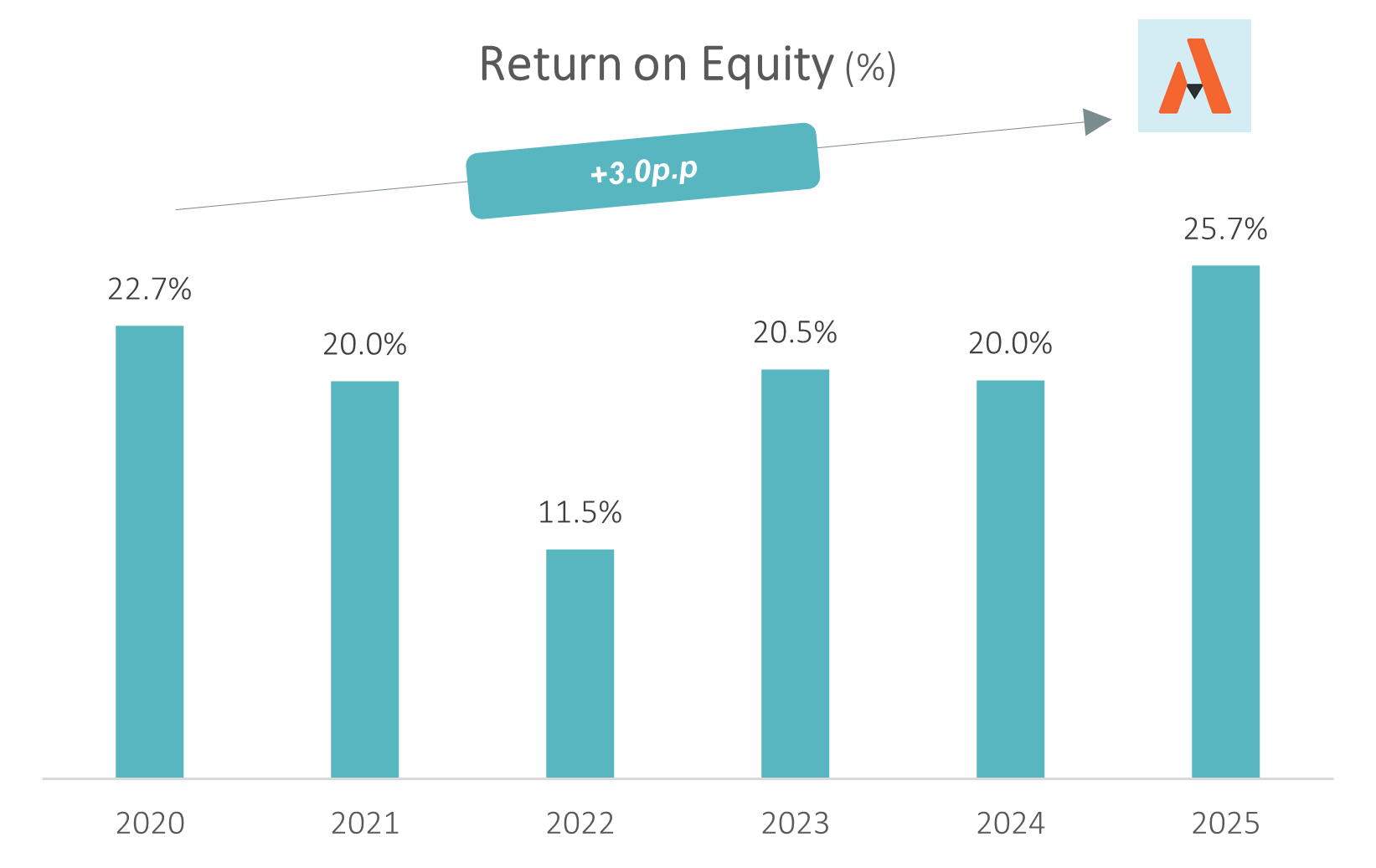

Cash generation and ROIC remains strong, but it can evaporate in a few years.

So far, I’ve lost around 40% in my investment.

It’s clearly my biggest mistake.

To recover, I need +67% increase from current levels. I don’t expect this will happen with PayPal.

However, I think the company will recover from current levels to more reasonable valuation levels.

If management is capable to stabilize the situation, stock should regain at least $60 per share to trade at reasonable levels. On the hand, if they don’t do it, stock will certainly keep falling.

While I continue to look for investment opportunities, I will remain invested in PayPal. Selling at 40% loss, to acquire a new stock is not efficient from tax purposes. If I believe the stock can at least partly recover, I prefer to wait.

I will continue to closely monitor the situation. If results don’t show any signal of improvement, I will sell the stock for sure.

As a conclusion, PayPal could be categorized as a big mistake. However, when we look at valuation and current fundamentals, the stock seems pretty undervalued. However, the market is addressing PayPal 2 years from now.

Today it seems that the future is very dark, let’s see in a couple of quarters.

This is not investment recommendation

Thanks for reading

Asymmetric Ventures

Disclaimer:

PayPal looks very cheap but I would never invest in it because of how they treated me when I was living in Myanmar (2011 to 2015). Very poor customer service.